Question

In: Accounting

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

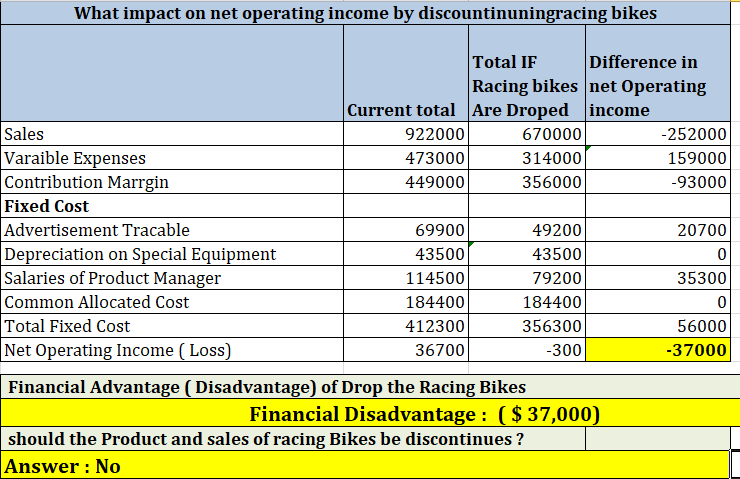

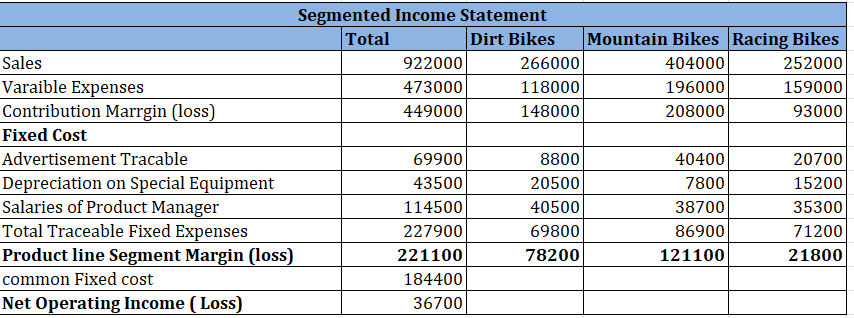

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a racing bike. Data on sales and expenses for the past quarter follow: Total Dirt Bikes Mountain Bikes Racing Bikes Sales $ 922,000 $ 266,000 $ 404,000 $ 252,000 Variable manufacturing and selling expenses 473,000 118,000 196,000 159,000 Contribution margin 449,000 148,000 208,000 93,000 Fixed expenses: Advertising, traceable 69,900 8,800 40,400 20,700 Depreciation of special equipment 43,500 20,500 7,800 15,200 Salaries of product-line managers 114,500 40,500 38,700 35,300 Allocated common fixed expenses* 184,400 53,200 80,800 50,400 Total fixed expenses 412,300 123,000 167,700 121,600 Net operating income (loss) $ 36,700 $ 25,000 $ 40,300 $ (28,600) *Allocated on the basis of sales dollars. Management is concerned about the continued losses shown by the racing bikes and wants a recommendation as to whether or not the line should be discontinued. The special equipment used to produce racing bikes has no resale value and does not wear out. Required: 1. What is the financial advantage (disadvantage) per quarter of discontinuing the racing bikes? 2. Should the production and sale of racing bikes be discontinued? 3. Prepare a properly formatted segmented income statement that would be more useful to management in assessing the long-run profitability of the various product lines.

Solutions

ekkarill92 answered 4 months ago

ekkarill92 answered 4 months agoRelated Solutions

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

The Regal Cycle Company manufactures three types of bicycles—a dirt bike, a mountain bike, and a...

- What are the key environmental and biological controls over decomposition rate in ecosystems?

- describe why independent oversight is important to taxpayers.

- Graph a Monopoly. Compare the price, quantity, and ATC of a monopoly with a perfectly competitive...

- Problem 18-12 Various shareholders' equity topics; comprehensive [LO18-1, 18-4, 18-5, 18-6, 18-7, 18-8] Part A In...

- Hello There, This is discussion Question For Advanced Database Systems Question: (a) Please define what a...

- Physicians at a clinic gave what they thought were drugs to 860860 patients. Although the doctors...

- On January 1, 2018, bonds with a face value of $ 79,000 were sold. The bonds...