Question

In: Economics

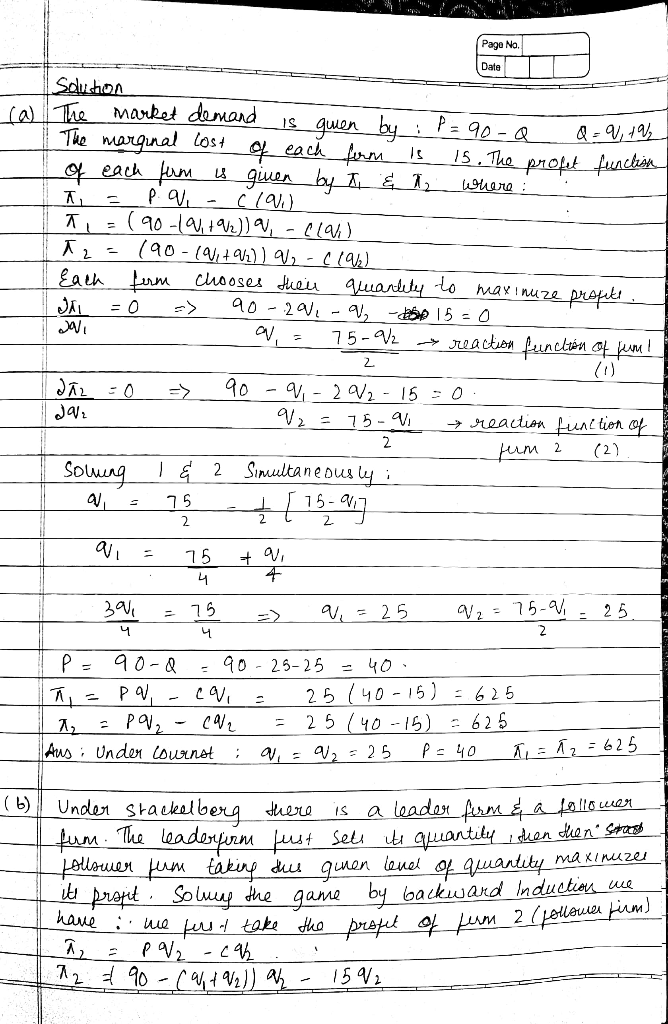

4. Two firms face a market demand of p = 90 – Q, each firm with...

4. Two firms face a market demand of p = 90 – Q, each firm with a constant marginal cost of $15 per unit.

a. What are the Cournot equilibrium q1, q2, price and profits for each firm?

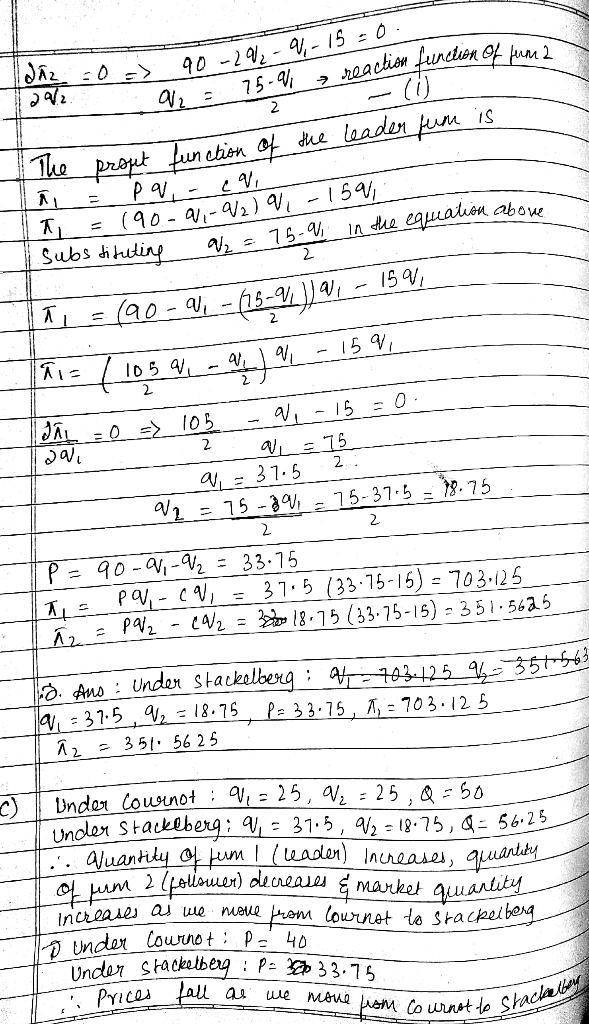

b. What are the Stackelberg equilibrium q1, q2, price and profits for each firm, assuming firm 1 moves first?

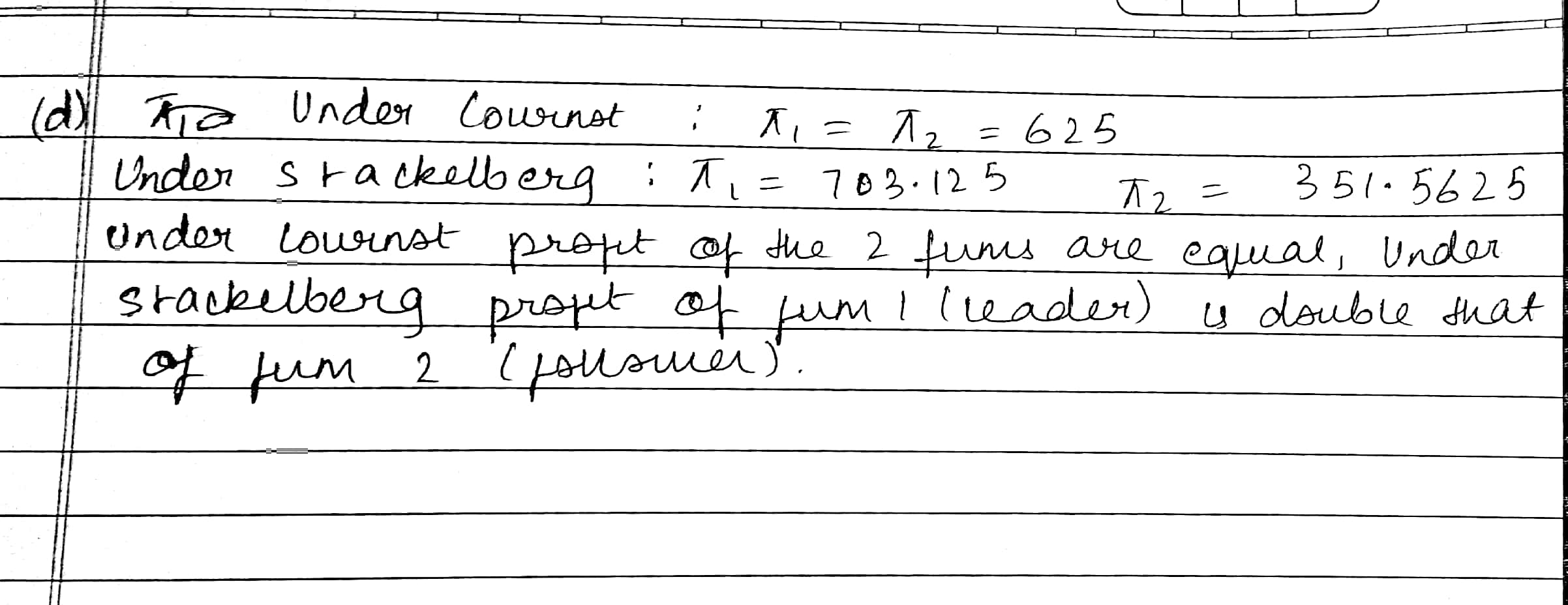

c. Compare the quantities, price and profits between the two models.

Solutions

Rahul Sunny answered 2 hours ago

Rahul Sunny answered 2 hours agoRelated Solutions

Cournot duopolists face a market demand curve given by P = 90 -Q where Q is...

Cournot duopolists face a market demand curve given by P = 90 -Q

where Q is total market demand. Each firm can produce output at a

constant marginal cost of 30 per unit. There are no fixed costs.

Determine the (1) equilibrium price, (2) quantity, and (3) economic

profits for the total market,(4) the consumer surplus, and (5) dead

weight loss.Show Work

Cournot duopolists face a market demand curve given by P = 90 - Q where Q...

Cournot duopolists face a market demand curve given by P = 90 -

Q where Q is total market demand. Each firm can produce output at a

constant marginal cost of 30 per unit. There are no fixed costs.

Determine the (1) equilibrium price, (2) quantity, and (3) economic

profits for the total market, (4) the consumer surplus, and (5)

dead weight loss.

Cournot duopolists face a market demand curve given by P = 90 - Q where Q...

Cournot duopolists face a market demand curve given by P = 90 -

Q where Q is total market demand. Each firm can produce output at a

constant marginal cost of 30 per unit. There are no fixed cost.

(Just need B through C answer please)

a. Find the equilibrium price, quantity and economic profit for

the total market, consumer surplus and Dead weight loss

b. If the duopolists in question above behave, instead,

according to the Bertrand model, what...

25.) Duopolists face a market demand curve given by P = 90 - Q where Q...

25.) Duopolists face a market demand curve given by P = 90 - Q

where Q is total market demand. Each firm can produce output at a

constant marginal cost of 30 per unit. There are no fixed costs. If

the duopolists behave, according to the Bertrand model, determine

the (1) equilibrium price, (2) quantity, and (3) economic profits

for the total market and (4) the consumer surplus, and (5) dead

weight loss.

Two firms compete in a market with inverse demand P(Q) = a − Q, where the...

Two firms compete in a market with inverse demand P(Q) = a − Q,

where the aggregate quantity is Q = q1 + q2. The profit of firm i ∈

{1, 2} is πi(q1, q2) = P(Q)qi − cqi , where c is the constant

marginal cost, with a > c > 0. The timing of the game is: (1)

firm 1 chooses its quantity q1 ≥ 0; (2) firm 2 observes q1 and then

chooses its quantity q2 ≥...

The market demand is Q=120-P, there are two firms on the market that engage in Stackelber...

The market demand is Q=120-P, there are two firms on the market

that engage in Stackelber competition. Both firms have MC=0 and

FC=0. How much more profit does Stackelber leader made compared to

Cournot?

The market demand curve is given by p = 100 - Q Two firms, A and...

The market demand curve is given by

p = 100 - Q

Two firms, A and B, are competing in the Cournot fashion. Both

firms have the constant marginal cost of 70. Suppose firm A

receives a new innovation which reduces its marginal cost to c.

Find the cutoff value of c which makes this innovation

"drastic".

Consider an oligopolist market with demand: Q = 18 – P. There are two firms A...

Consider an oligopolist market with demand: Q = 18 – P. There

are two firms A and B. The cost function of each firm is given by

C(q) = 8 + 6q. The firms compete by simultaneously choosing

quantities.

a. Write down firm A’s profit function and derive firm A’s

reaction function.

b. Plot the reaction functions of both firms in a diagram.

c. What is the optimal quantity produced by firm A and firm

B?

d. Now suppose firm...

Consider a market with two firms, facing the demand function: p = 120 – Q. Firms...

Consider a market with two firms, facing the demand function: p

= 120 – Q. Firms are producing their output at constant

MC=AC=20.

If the firms are playing this game repetitively for infinite

number of times, find the discount factor that will enable

cooperation given the firms are playing grim trigger strategy.

Q1.Two firms produce in a market with demand P=100-Q. The marginal cost for firm 1 is...

Q1.Two firms produce in a market with demand P=100-Q. The

marginal cost for firm 1 is constant and equals 10. The marginal

cost of firm 2 is also constant and it equals 25. Firm 1 sets

output first. After observing firm 1's output, firm 2 sets its

output. (Please pay attention. Read the brackets correctly.)

1a. For firm 2, the best response is R₂(q₁)=(A-q₁)/2. The value

for A is?

1b. Solve for the Stackelberg equilibrium. The quantity sold by

firm...

ADVERTISEMENT

ADVERTISEMENT

Latest Questions

- 5. Using terms a layperson would understand, state the differences between Congenital and Genetic disorders...

- 4. Two firms face a market demand of p = 90 – Q, each firm with...

- For this lab you will write a Java program that plays a simple Guess The Word...

- what effect did Sutton's discovery that chromosomes come in pairs have on his life?

- Sulfur and fluorine react to form sulfur hexafluoride: S(s)+3F2(g)→SF6(g) Part A If 50.0 g S is...

- Explain how naproxen sodium and ibuprofen are structurally similar.

- For the t test , one uses ----------------instead of σ a. n b. s c. χ²...

ADVERTISEMENT