Question

In: Accounting

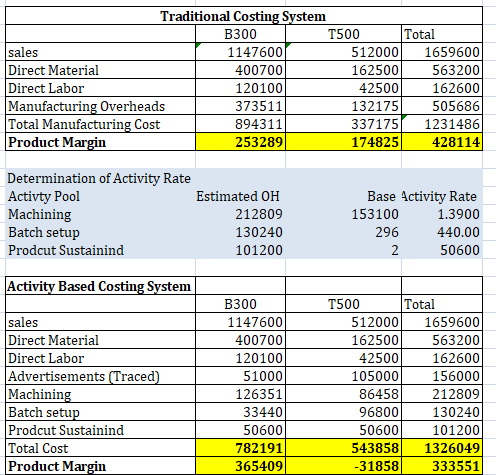

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption costing income statement for the most recent period is shown: Hi-Tek Manufacturing Inc .

| Income Statement Sales | $ 1,659,600 |

| Cost of goods sold | $1,230,949 |

| Gross margin | 428,651 |

| Selling and administrative expenses | 570,000 |

| Net operating loss | $ (141,349 ) |

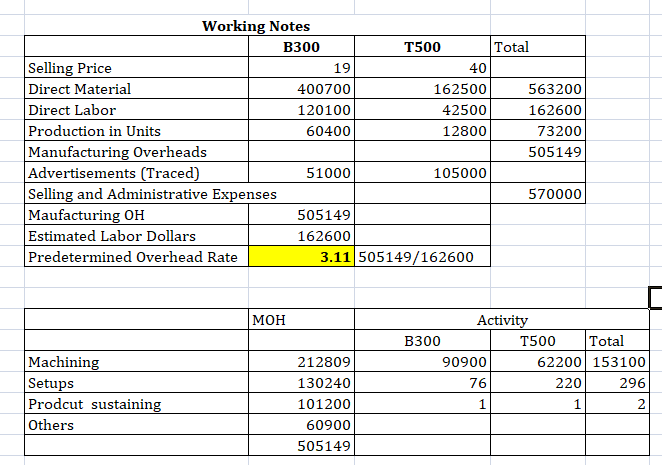

Hi-Tek produced and sold 60,400 units of B300 at a price of $19 per unit and 12,800 units of T500 at a price of $40 per unit. The company’s traditional cost system allocates manufacturing overhead to products using a plantwide overhead rate and direct labor dollars as the allocation base. Additional information relating to the company’s two product lines is shown below:

| B300 | T500 | Total | |

| Direct Materials | $ 400,700.00 | $ 162,500.00 | $ 563,200.00 |

| Direct Labor | $ 120,100.00 | $ 42,500.00 | $ 162,600.00 |

| Manufacturing Overhead | $ 505,149.00 | ||

| Cost of goods sold | $ 1,230,949.00 |

The company has created an activity-based costing system to evaluate the profitability of its products. Hi-Tek’s ABC implementation team concluded that $51,000 and $105,000 of the company’s advertising expenses could be directly traced to B300 and T500, respectively. The remainder of the selling and administrative expenses was organization-sustaining in nature. The ABC team also distributed the company’s manufacturing overhead to four activities as shown below:

| Activity | ||||

| Activity Cost Pool (and Activity Measure) | Manufacturing Overhead | B300 | T500 | Total |

| Machining (machine-hours) | $ 212,809 | $ 90,900.00 | $ 62,200.00 | $ 153,100.00 |

| Setups (setup hours) | $ 130,240 | 76 | 220 | 296 |

| Product-sustaining (number of products) | $ 101,200 | 1 | 1 | 2 |

| Other (organization-sustaining costs) | $ 60,900 | NA | NA | NA |

| Total manufacturing overhead cost | $ 505,149 | |||

Required:

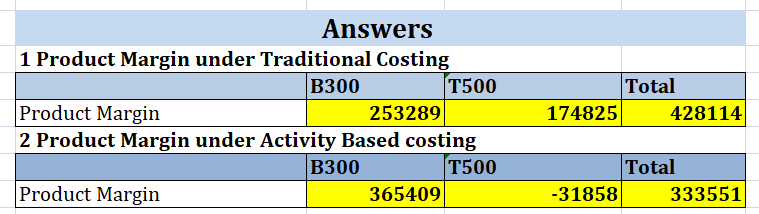

1. Compute the product margins for the B300 and T500 under the company’s traditional costing system.

2. Compute the product margins for B300 and T500 under the activity-based costing system.

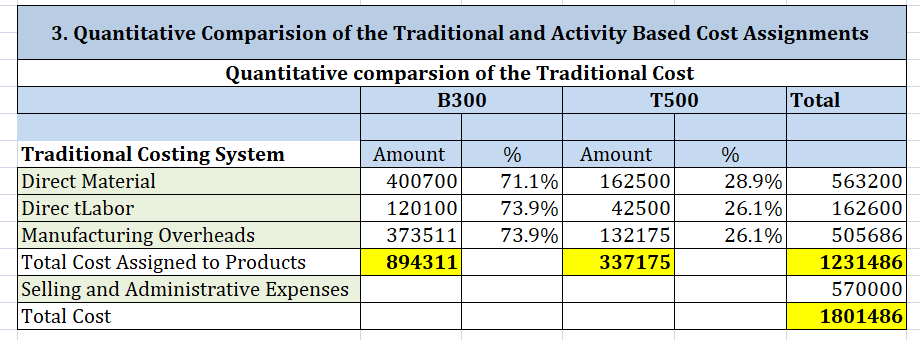

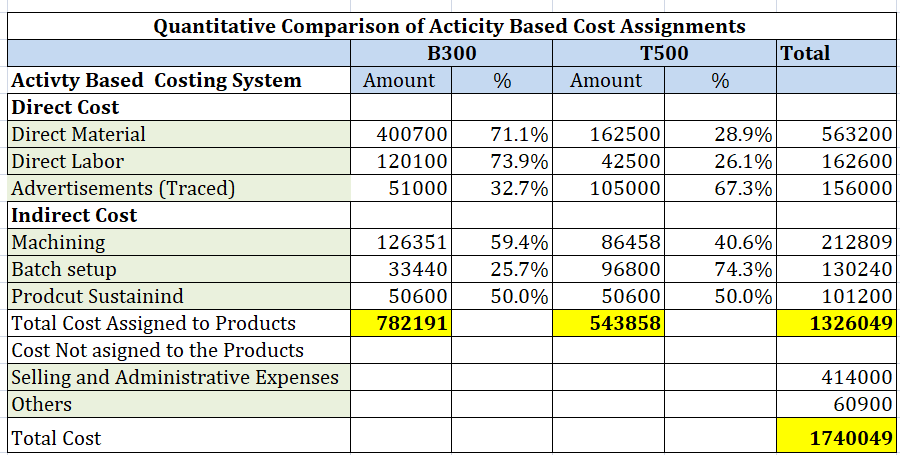

3. Prepare a quantitative comparison of the traditional and activity-based cost assignments.

Solutions

ekkarill92 answered 2 months ago

ekkarill92 answered 2 months agoRelated Solutions

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

Hi-Tek Manufacturing, Inc., makes two types of industrial component parts—the B300 and the T500. An absorption...

- On January 1, 2018, bonds with a face value of $ 79,000 were sold. The bonds...

- How do I make this sort in true alphabetical order instead of ascii(ABCabc) order? I am...

- As a healthcare provider in physical therapy, athletic training, or as an exercise scientist and personal...

- in the market for makeup artists, what happens after the invention of high-definition tv allowing viewers...

- 10. What are the three monetary policy tools of the Fed? Briefly describe how each tool...

- In what ways would the role of a manager working in a nonstandard international assignment arrangement...

- Write a Bash script called move that could replace the UNIX command mv. 'move' tries to...