Question

In: Economics

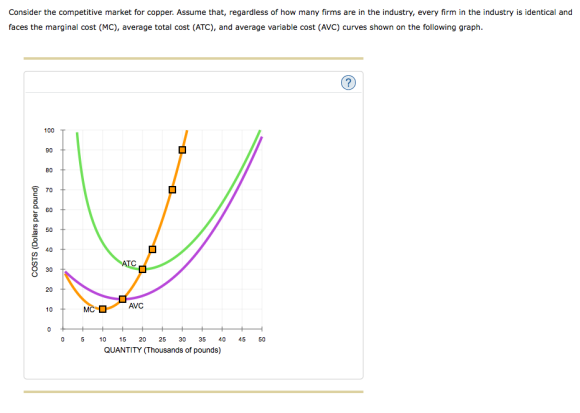

Consider the competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical

Consider the competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph.

Solutions

Expert Solution

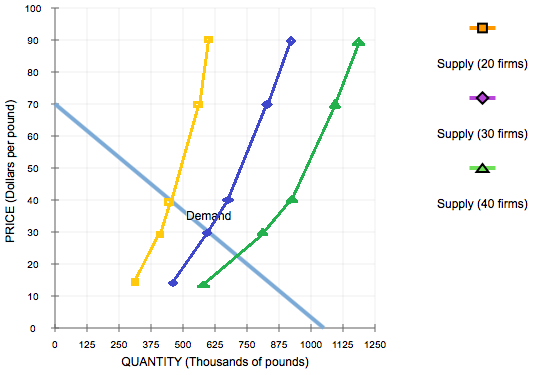

| P | QS-1 FIRM | QS-20 FIRMS | 30 FIRMS | 40 FIRMS |

| 10 | 0 | 0 | 0 | 0 |

| 15 | 15000 | 300000 | 450000 | 600000 |

| 30 | 20000 | 400000 | 600000 | 800000 |

| 40 | 22500 | 450000 | 675000 | 900000 |

| 70 | 27500 | 550000 | 825000 | 1100000 |

| 90 | 30000 | 600000 | 900000 | 1200000 |

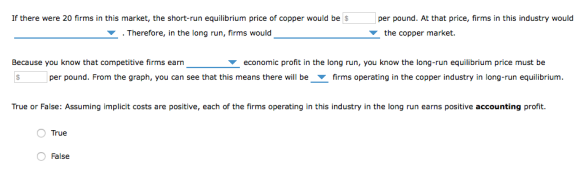

Blanks:-

1) 40

2) earn positive economic profits

3) enter the market

4) zero

5) 30

6) 30

The statement is True

Rahul Sunny answered 4 years ago

Rahul Sunny answered 4 years agoRelated Solutions

Consider the competitive market for titanium. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical

Consider the competitive market for titanium. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph.

Consider the competitive market for copper. Assume that, regardless of how many firms are in the...

Consider the competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph.

Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC)

Consider the perfectly competitive market for steel. Assume

that, regardless of how many firms are in the industry, every firm

in the industry is identical and faces the marginal cost

(MC), average total cost (ATC), and average

variable cost (AVC) curves shown on the following

graph. The following diagram shows the market demand for steel. Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 10 firms in the market. (Hint: You can disregard the...

7. Short-run supply and long-run equilibrium Consider the competitive market for copper. Assume that, regardless of...

7. Short-run supply and long-run

equilibrium

Consider the competitive market for copper. Assume that,

regardless of how many firms are in the industry, every firm in the

industry is identical and faces the marginal cost (MC), average

total cost (ATC), and average variable cost (AVC) curves shown on

the following graph.

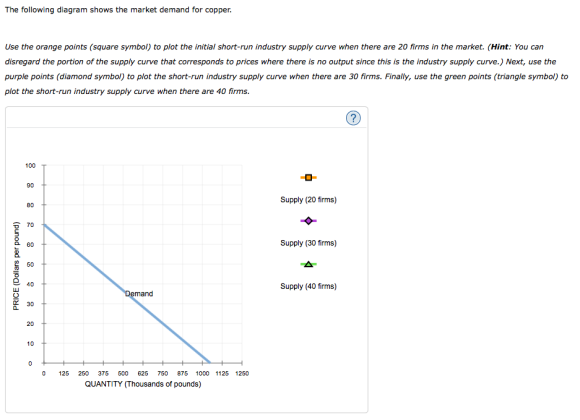

The following diagram shows the market demand for copper.

Use the orange points (square symbol) to plot the initial

short-run industry supply curve when there are 10 firms in...

Consider a market with two identical firms, Firm A and Firm B. The market demand is...

Consider a market with two identical firms, Firm A and Firm B.

The market demand is ? = 20−1/2?, where ? = ?a +?b . The cost conditions are

??a = ??b = 16.

a) Assume this market has a Stackelberg leader, Firm A. Solve

for the quantity, price and profit for each firm. Explain your

calculations.

b) How does this compare to the Cournot-Nash equilibrium

quantity, price and profit? Explain your calculations.

c) Present the Stackelberg and Cournot equilibrium...

Assume the following market is a pure competitive and all firms are identical with the same...

Assume the following market is a pure competitive and all firms

are identical with the same costs functions: TC=100 +80*q+q^2

MC=80+2q The market demand is P=150-Q_d The equilibrium price in

short run is $100. Note that Q is the market quantity and q is the

quantity produced by a single firm. Calculate the output that

minimizes average total cost (ATC). (2 points) What is the

breakeven price for this firm in long run? How many firms will be

in the...

Assume a competitive market for computer hard drives. All firms in the market are identical each...

Assume a competitive market for computer hard drives. All firms

in the market are identical each with cost function given by C(q) =

32 + 2q2 where q is measured in thousands of units per year. In

this market, each firm will make zero profits when it produces

_________ units.

Suppose there is a perfectly competitive industry where all the firms are identical with identical cost...

Suppose there is a perfectly competitive industry where all the

firms are identical with identical cost curves.

Furthermore, suppose that a representative firm’s total cost is

given by the equation TC = 120 + q2 + 2q where q is the

quantity of output produced by the firm.

You also know that the market demand for this product is given

by the equation P = 1200 – 2Q where Q is the market quantity. In

addition you are told that...

Suppose there is a perfectly competitive industry where all the firms are identical with identical cost...

Suppose there is a perfectly competitive industry where all the

firms are identical with identical cost curves.

Furthermore, suppose that a representative firm’s total revenue

is given by the equation TR = q.p; where q is the quantity of

output produced by the firm and p the market price (=P).

The market demand for this product is given by the equation P =

5000 – 9Q where Q is the market quantity.

In addition you are told that the market...

Suppose there is a perfectly competitive industry where all the firms are identical with identical cost...

Suppose there is a perfectly competitive industry where all the

firms are identical with identical cost curves.

Furthermore, suppose that a representative firm’s total revenue

is given by the equation TR = q.p; where q is the quantity of

output produced by the firm and p the market price (=P).

The market demand for this product is given by the equation P =

5000 – 9Q where Q is the market quantity.

In addition you are told that the market...

ADVERTISEMENT

ADVERTISEMENT

Latest Questions

- describe why independent oversight is important to taxpayers.

- Graph a Monopoly. Compare the price, quantity, and ATC of a monopoly with a perfectly competitive...

- Problem 18-12 Various shareholders' equity topics; comprehensive [LO18-1, 18-4, 18-5, 18-6, 18-7, 18-8] Part A In...

- Hello There, This is discussion Question For Advanced Database Systems Question: (a) Please define what a...

- Physicians at a clinic gave what they thought were drugs to 860860 patients. Although the doctors...

- On January 1, 2018, bonds with a face value of $ 79,000 were sold. The bonds...

- How do I make this sort in true alphabetical order instead of ascii(ABCabc) order? I am...

ADVERTISEMENT