Question

In: Accounting

a) Your friend wants you to explain why it is generally better for taxpayers to “maximize...

a) Your friend wants you to explain why it is generally better for taxpayers to “maximize their after-tax incomes” rather than simply “minimize their current year tax liabilities.” Create a simple example to illustrate how minimizing the current year’s tax liability does not always result in maximizing after-tax income, and walk your friend through each step of your calculation.

b) What are the four basic variables that can change the structure of a transaction and impact the related tax consequences? Provide your friend with a general description of each variable, and using your own numbers, create a short, simple example to show how each can be used effectively to reduce taxes from the perspective of legal tax planning. Despite the potential tax benefits from pursuing effective tax planning strategies, why must a taxpayer be careful not to ignore the importance of nontax factors?

c) Your prior responses have your friend wondering about the primary difference between tax avoidance and tax evasion. Define and provide an example of each, and compare/contrast the typical consequences a taxpayer can expect from the Internal Revenue Service when s/he engages in either of the behaviors. In your response, identify the legal doctrines that the IRS typically uses to challenge a tax planning strategy.

d) Finally, your friend needs you to explain what is meant by an “implicit tax.” Define an implicit tax, and illustrate the concept by showing your friend how a taxpayer’s marginal tax rate will determine whether s/he should invest $10,000 in a fully taxable corporate bond generating pretax interest of 8%, or a municipal bond generating pretax interest of 6%. At what marginal tax rate will an investor be indifferent between the two options?

Solutions

Expert Solution

A

5 ways to maximise you income tax return

Taxes are unavoidable but you can surely minimize its impact by filing the Income Tax return every year. Whether you have invested your money or made large payments against loans, travel or insurance it's time to look back at the year to maximise your deductions and thereby lower your tax burden.

1. Contribution made towards Public Provident Fund (PPF)

Investments in these small saving instruments start from as low as Rs 500 up to Rs 1.5 lakh with a rate of interest at 8 per cent per annum.

While the lock-in period is 15 years, withdrawal is possible under certain conditions.

The investment, the gains as well as the withdrawals are completely tax-free.

2. Employer's Provident Fund (EPF)

The employer's contribution to your EPF is tax-free, and your contribution is tax-deductible under Section 80C of the Income Tax Act.

The total PF amount deducted annually can be claimed by you as deduction while computing your total taxable income.

So the money you invest in your EPF, the interest earned and the lump sum withdrawal after the specified period are exempt from income tax.

3. Home loan

If you have a home loan to repay you can claim a deduction against the principal repayment up to Rs 1.50 lakh under section 80C.

You are also eligible for a deduction up to Rs 2 lakh for the interest on home loan paid under Section 24 in case of a self occupied house. While for the second house you can claim the entire amount of interest paid as deduction.

4. House Rent Allowance

If you are staying in a rented accommodation, you can claim a tax deduction against the rent paid if HRA is a part of your salary.

Between the rent allowance provided by the employer, The actual rent that you pay minus 10% of your basic salary and 50% of your basic salary (if you are living in a metro city) 40% of your basic salary (if you reside in a non-metro city) the least amount will be allowed as tax exemption on your HRA.

5. Health and Life Insurance

Investments made towards health insurance can be claimed up to Rs 25,000 under section 80D of the Income Tax Act against the premium paid for yourself, your spouse and children.

Payment of life insurance qualifies for a deduction of up to Rs 1.5 lakh on premium paid for LIC as well as all other private insurance companies.

Minimizing Tax Liability

If you want to save money on your tax bill

next year, consider using one or more of these tax-saving

strategies that reduce your income, lower your tax bracket, and

minimize your tax bill.

If you want to save money on your tax bill

next year, consider using one or more of these tax-saving

strategies that reduce your income, lower your tax bracket, and

minimize your tax bill.

1. Max out your 401(k) or Contribute to an IRA

You've heard it before, but it's worth repeating because it's one of the easiest and most cost-effective ways of saving money for your retirement. Many employers offer plans where you can elect to defer a portion of your salary and contribute it to a tax-deferred retirement account. For most companies, these are referred to as 401(k) plans. For many other employers, such as universities, a similar plan called a 403(b) is available. Check with your employer about the availability of such a plan and contribute as much as possible to defer income and accumulate retirement assets.

If you have income from wages or self-employment income, you can build tax-sheltered investments by contributing to a traditional (pre-tax contributions) or a Roth IRA (after-tax contributions). You may also be able to contribute to a spousal IRA even when your spouse has little or no earned income.

2. Take Advantage of Employer Benefit Plans

Medical and dental expenses are generally only deductibles to the extent they exceed 7.5 percent of your adjusted gross income (AGI) in 2018 (rising to 10% in 2019). For many individuals, particularly those with high income, this could eliminate the possibility for a deduction.

However, you can effectively get a deduction for these items if your employer offers a Flexible Spending Account or FSA (sometimes called a cafeteria plan). These plans permit you to redirect a portion of your salary to pay these types of expenses with pre-tax dollars. Another such arrangement is a Health Savings Account (HSA). Ask your employer if they provide either of these plans.

Learn More about Tax Preparation for Small Businesses

3. Bunch your Itemized Deductions

Certain itemized deductions, such as medical or employment-related expenses, are only deductible if they exceed a certain amount. It may be advantageous to delay payments in one year and prepay them in the next year to bunch the expenses in one year. This way you stand a better chance of getting a deduction.

4. Use the Gift-Tax Exclusion to Shift Income

In 2018, you can give away $15,000 ($30,000 if joined by a spouse) per donee, per year without paying federal gift tax. And, you can give $15,000 to as many donees as you like. The income on these transfers will then be taxed at the donee's tax rate, which is in many cases lower.

Note: Special rules apply to children under age 18. Also, if you directly pay the medical or educational expenses of the donee, such gifts will not be subject to gift tax.

For gift tax purposes, contributions to Qualified Tuition Programs (Section 529) are treated as completed gifts even though the account owner has the right to withdraw them. As such, they qualify for the up-to-$15,000 annual gift tax exclusion in 2018. One contributing more than $15,000 may elect to treat the gift as made in equal installments over the year of the gift and the following four years so that up to $60,000 can be given tax-free in the first year.

5. Consider Tax-Exempt Municipal Bonds

Interest on state or local municipal bonds is generally exempt from federal income tax and from tax by the issuing state or locality. For that reason, interest paid on such bonds is somewhat less than that paid on commercial bonds of comparable quality. However, for individuals in higher brackets, the interest from municipal bonds will often be greater than from higher paying commercial bonds after reduction for taxes. Gain on sale of municipal bonds is taxable, and loss is deductible. Tax-exempt interest is sometimes an element in the computation of other tax items. Interest on loans to buy or carry tax-exempts is non-deductible.

B.

I. The subjects of every state ought to contribute towards the support of the government, as nearly as possible, in proportion to their respective abilities; that is, in proportion to the revenue which they respectively enjoy under the protection of the state.…

II. The tax which each individual is bound to pay ought to be certain, and not arbitrary. The time of payment, the manner of payment, the quantity to be paid, ought all to be clear and plain to the contributor, and to every other person.…

III. Every tax ought to be levied at the time, or in the manner, in which it is most likely to be convenient for the contributor to pay it.…

IV. Every tax ought to be so contrived as both to take out and keep out of the pockets of the people as little as possible over and above what it brings into the public treasury of the state.…

Although they need to be reinterpreted from time to time, these principles retain remarkable relevance. From the first can be derived some leading views about what is fair in the distribution of tax burdens among taxpayers. These are: (1) the belief that taxes should be based on the individual’s ability to pay, known as the ability-to-pay principle, and (2) the benefit principle, the idea that there should be some equivalence between what the individual pays and the benefits he subsequently receives from governmental activities. The fourth of Smith’s canons can be interpreted to underlie the emphasis many economists place on a tax system that does not interfere with market decision making, as well as the more obvious need to avoid complexity and corruption.

Distribution of tax burdens

Various principles, political pressures, and goals can direct a government’s tax policy. What follows is a discussion of some of the leading principles that can shape decisions about taxation.

Horizontal equity

The principle of horizontal equity assumes that persons in the same or similar positions (so far as tax purposes are concerned) will be subject to the same tax liability. In practice this equality principle is often disregarded, both intentionally and unintentionally. Intentional violations are usually motivated more by politics than by sound economic policy (e.g., the tax advantages granted to farmers, home owners, or members of the middle class in general; the exclusion of interest on government securities). Debate over tax reform has often centred on whether deviations from “equal treatment of equals” are justified.

C.

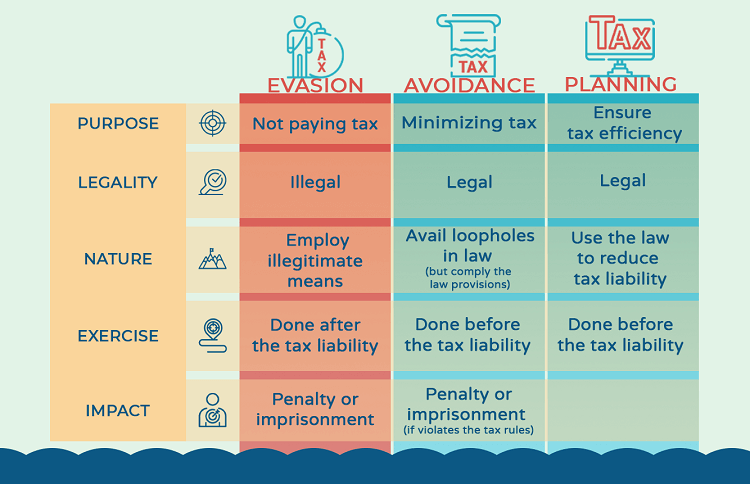

Differences between tax evasion, tax avoidance and tax planning

Businesses in search of saving tax often come up with those couples of terms. Each term has been clarified quite obviously in our above-mentioned sections. Below are key differences between tax evasion, tax avoidance and tax planning to help you get better understanding:

- Purpose: All serve for tax saving, but tax avoidance aims at minimizing tax, while tax evasion is deemed a form of not paying tax. Tax planning, on the other hand, helps businesses to ensure tax efficiency.

- Legality: Both tax planning and tax avoidance are legal. As considered as frauds, tax evasion is an illegal method to reduce tax.

- Nature: Tax avoidance is performed by availing loopholes in the law, but complying with law provisions. By contrast, tax evasion is performed by employing illegitimate means for nonpayment of tax. Tax planning uses existing law provisions to relieve the burden of tax liability.

- How it is exercised: Tax avoidance is characterized as tax planning, but it is done before tax liability takes place. This method generally emerges in short-term benefits. Like tax avoidance, tax planning also should be done before tax liability arises, but it associates with the future and often serves for either long-term or short-term benefits of every assessee. Oppositely, tax evasion is typically done after the tax liability has arisen.

- Consequences: Tax avoidance is subject to penalty or imprisonment if it violates the tax regulations. Tax planning is totally legal, meanwhile tax evasion must be subject to penalty and other kinds of punishment.

D.

implicit tax

Definition

A reduction in the return on a tax-favored investment. In theory, investors are willing to accept a lower return on an investment if it is subject to lower taxes. The term "implicit tax" is also used to describe an indirect cost that results from a government policy. For example, environmental regulations might impose an implicit tax on businesses that have to spend money to comply with them.

please give the Good Feedback

ekkarill92 answered 3 years ago

ekkarill92 answered 3 years agoRelated Solutions

Distinguish between needs and wants, and explain why it may be better to act as if...

Your friend tells you that she wants to start saving for retirement by investing in the...

Your friend Bob wants to starts an Italian restaurant and you decide to to invest in...

Your friend picks a random card and wants you to guess if it’s a face card....

Your friend wants to borrow $2,500 and pay you back the $2,500 in a year from...

Discuss why deductions FOR AGI are generally considered more beneficial to taxpayers than deductions FROM AGI....

What is a friend function? Do we have to use friend functions? Explain why or why...

How would you explain the concept of synergism to a friend unfamiliar with the topic? Why...

Your friend is talking to you about one of their investments. Yesterday, your friend received a...

why taxpayers must have insurance? please explain as much as possible

- prepare a tecnical report that discuss about "A custom Union (CU) constitute a partial movement towards...

- in your own opinion, It has been said that a smartphone is a computer in your...

- Use the internet to read more about journaling file systems such as NTFS, extfs2, and extfs3....

- Consider the quick sort algorithm. The quick sort algorithm is a divide and conquer approach which...

- Tesla 1. How to make these weaknesses into strengths? Burn through cash, high prices, bottlenecking/product delays,...

- Assignment # 12: Email Presentation Learning Objectives and Outcomes Design a PowerPoint presentation appropriate for middle...

- Identify which of the perspectives you believe is the BEST for accurately explaining human behavior and...