Question

In: Finance

Steve Sullivan was recently promoted to loan officer at the first national bank. He has authority...

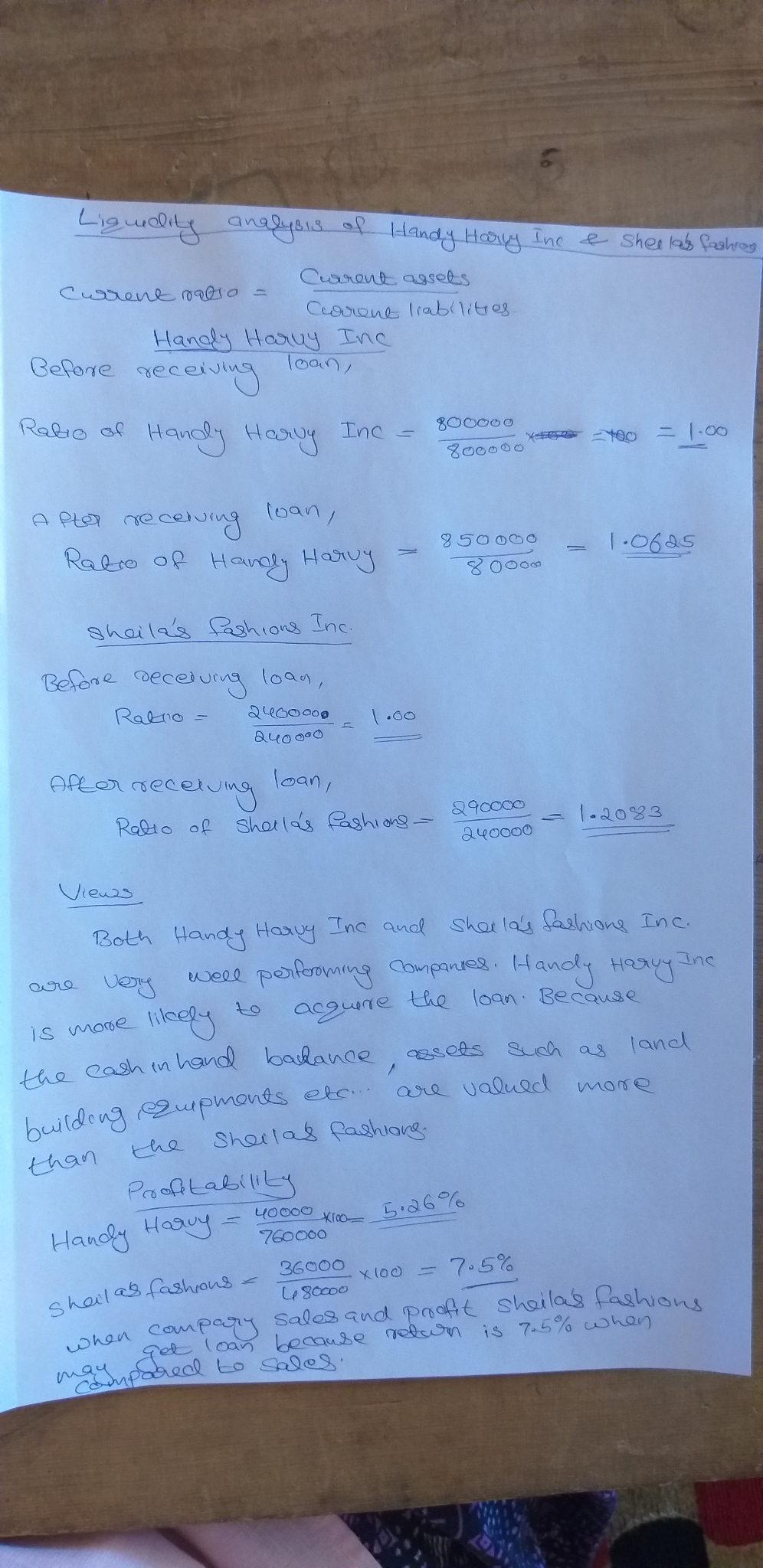

Steve Sullivan was recently promoted to loan officer at the first national bank. He has authority to issue loans up to $50,000 without approval from a higher bank official. this week two small companies, Handy Harvey, Inc. and Sheila’s fashion, Inc, have each submitted a proposal for a six-month $50,000 loan. In order to prepare a financial analysis of the two companies Steve has obtained the information summarized below.

Handy Harvey, Inc. is a local lumber and home improvement company. Because sales have increased so much during the past two years, Handy Harvey has had to raise additional working capital , especially as represented by receivables and inventory. The $50,000 loan is needed to assure the company of enough working capital for next year. Handy Harvey began the year with total assets of $740,000 and stockholders equity of $260,000 and during the past year the company had a net income of $40,000 on sales of $760,000. The company’s current unclassified balance sheet appears as follows:

|

Assets |

$ |

Liability and stockholder’s equity |

$ |

|

|

Cash |

30,000 |

Account payable |

200,000 |

|

|

Account receivable (net) |

150,000 |

Note payable |

100,000 |

|

|

Inventory |

250,000 |

Mortage payable |

200,000 |

|

|

Land |

50,000 |

Common stock |

250,000 |

|

|

Buildings (net) |

250,000 |

Retained earnings |

50,000 |

|

|

Equipment (net) |

70,000 |

Totatal liability and stockholder equity |

800,000 |

|

|

Total assets |

800,000 |

Sheila’s Fashions, Inc. has for three years been a successful clothing store for young professional women. The leased store is located in the downtown financial district. Sheila’s loan proposal ask for $50,000 to pay for stocking a new line professional suilts for working women during the coming season. At the beginning of the year, the company had total assets of $200,000 and total stockholders’ equity of $114,000. Over the past year, the company earned a income of $36,000 on sales of $480,000. The firm’s unclassified balance sheet the current date appears as follows

|

Assets |

$ |

Liability and stockholder’s equity |

$ |

|

|

Cash |

10,000 |

Account payable |

80,000 |

|

|

Account receivable (net) |

50,000 |

Accrued liabilities |

10,000 |

|

|

Inventory |

135,000 |

Common stock |

50,000 |

|

|

Prepaid expenses |

5,000 |

Retained earnings |

100,000 |

|

|

Equipment (net) |

40,000 |

|||

|

Totatal liability and stockholder equity |

240,000 |

|||

|

Total assets |

240,000 |

Required

- Prepare a financial analysis of both companies’ liquidity and after receiving the proposed loan. Also, compute profitability ratios before and after as appropriate. Write a brief summary of the effect if the proposed loan on each company’s financial position.

- To which company do you suppose Steve would be most willing to make a $50,000 loan? What are the positive and negative factors related to each company’s ability to pay back the loan in the next year? What other information of a financial or non-financial nature would be helpful before making a financial decision?

Solutions

jeff jeffy answered 3 weeks ago

jeff jeffy answered 3 weeks agoRelated Solutions

You are a loan officer for National Bank. You have a loan application submitted by a...

You are a loan officer for The National Bank. Trish Jones, president of Jones Corporation, has...

Lynch was the loan officer at First Bank. Patterson applied to borrow $25,000. Bank policy required...

Joseph Berio is a loan officer with the First Bank of Tennessee. Red Brick, Inc., a...

The First National Bank has a mortgage loan office with conversion cost of $73,950 per month.

1-18 (Objectives 1-1 ) James Burrow is the loan officer for the National Bank of Dallas....

You are a loan officer for First Benevolent Bank. You have an uneasy feeling as you...

1. Valley View Manufacturing Inc. sought a $500,000 loan from First National Bank. First National insisted...

After reviewing the financial statements, the loan officer at the bank asked your brother whether he...

eBook Problem 9-19 Joseph Berio is a loan officer with the First Bank of Tennessee. Red...

- Problem 18-12 Various shareholders' equity topics; comprehensive [LO18-1, 18-4, 18-5, 18-6, 18-7, 18-8] Part A In...

- Hello There, This is discussion Question For Advanced Database Systems Question: (a) Please define what a...

- Physicians at a clinic gave what they thought were drugs to 860860 patients. Although the doctors...

- On January 1, 2018, bonds with a face value of $ 79,000 were sold. The bonds...

- How do I make this sort in true alphabetical order instead of ascii(ABCabc) order? I am...

- As a healthcare provider in physical therapy, athletic training, or as an exercise scientist and personal...

- in the market for makeup artists, what happens after the invention of high-definition tv allowing viewers...