Question

In: Accounting

Pell Corporation's property, plant, and equipment and accumulated depreciation accounts had the following balances at December...

Pell Corporation's property, plant, and equipment and accumulated depreciation accounts had the following balances at December 31, 2015:

| Property, Plant, and Equipment |

Accumulated Depreciation |

|

|---|---|---|

| Land | $350,000 | $ — |

| Land Improvements | 180,000 | 45,000 |

| Building | 1,500,000 | 350,000 |

| Machinery and Equipment | 1,158,000 | 405,000 |

| Automobiles | 150,000 | 112,000 |

Depreciation method and useful lives:

- Land improvements: Straight-line; 15 years.

- Building: 150%-declining-balance; 20 years.

- Machinery and equipment: Straight-line; 10 years.

- Automobiles: 150%-declining-balance; 3 years.

- Depreciation is computed to the nearest month. No salvage values are recognized.

Transactions during 2016:

- On January 2, 2016, machinery and equipment were purchased at a total invoice cost of $260,000, which included a $5,500 charge for freight. Installation costs of $27,000 were incurred.

- On March 31, 2016, a machine purchased for $58,000 on January 3, 2012, was sold for $36,500.

- On May 1, 2016, expenditures of $50,000 were made to repave parking lots at Pell's plant location. The work was necessitated by damage caused by severe winter weather.

- On November 2, 2016, Pell acquired a tract of land with an existing building in exchange for 10,000 shares of Pell's $20 par common stock, which had a market price of $38 a share on this date. Pell paid legal fees and title insurance totaling $23,000. The last property tax bill indicated assessed values of $240,000 for land and $60,000 for building. Shortly after acquisition, the building was razed at a cost of $35,000 in anticipation of new building construction in 2017.

- On December 31, 2016, Pell purchased a new automobile for $15,250 cash and trade-in of an automobile purchased for $18,000 on January 1, 2015. The new automobile has a cash value of $19,000.

Required:

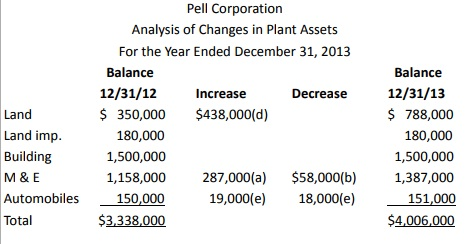

1. Prepare a schedule analyzing the changes in each of the plant assets during 2016. Disregard the related accumulated depreciation accounts.

| PELL CORPORATION | ||||

| Analysis of Changes in Plant Assets | ||||

| For the Year Ended December 31, 2016 | ||||

| Balance 12/31/15 | Increase | Decrease | Balance 12/31/16 | |

| Land | $ | $ | $ | |

| Land improvements | ||||

| Building | ||||

| Machinery and equipment | ||||

| Automobiles | ||||

| Totals | $ | $ | $ | $ |

Feedback

2. For each asset classification, prepare a schedule showing depreciation expense for the year ended December 31, 2016.

| PELL CORPORATION | |||

| Depreciation Expense | |||

| For the Year Ended December 31, 2016 | |||

| Land improvements: | |||

| Total depreciation on land improvements | $ | ||

| Building: | |||

| Total depreciation on building | |||

| Machinery and equipment: | |||

| Cost of machinery and equipment, Balance, 12/31/15 | $ | ||

| Deduct machine sold 3/31/16 | $ | ||

| Depreciation after applying straight-line rate | |||

| Cost of asset purchased 1/2/16 | $ | ||

| Depreciation | |||

| Cost of machine sold 3/31/16 | $ | ||

| Depreciation from 1/1/16 to 3/31/16 | |||

| Total depreciation on machinery and equipment | |||

| Automobiles: | |||

| Total depreciation on automobiles | |||

| Total depreciation expense for 2016 | $ | ||

Feedback

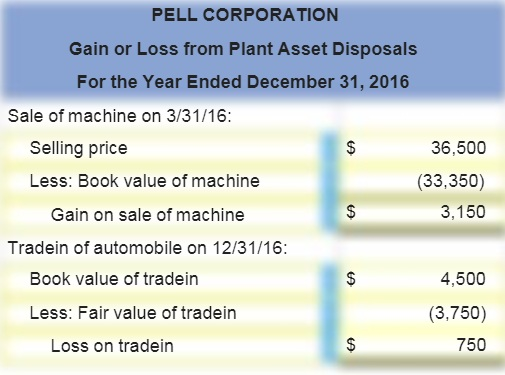

3. Prepare a schedule showing the gain or loss from each asset disposal that Pell would recognize in its income statement for the year ended December 31, 2016.

| PELL CORPORATION | |

| Gain or Loss from Plant Asset Disposals That Would Be Recognized in Income Statement | |

| For the Year Ended December 31, 2016 | |

| Gain or (loss) | |

| Sale of machine 3/31/16: | |

| Selling price | $ |

| Carrying amount of machine sold | |

| Gain on sale | $ |

| Trade-in of automobile 12/31/16: | |

| Carrying amount of trade-in | $ |

| Trade-in allowed | |

| Loss on trade-in | |

| Net gain from asset disposals | $ |

Solutions

Expert Solution

I HOPE ITS HELPFUL TO YOU IF YOU HAVE ANY DOUBTS PLS COMMENTS BELOW..I WILL BE THERE TO HELP YOU...ALL THE BEST...!!

AS FOR GIVEN DATA...

1.

a) 1/2 Machinery and equipment (260,000 + 27,000) 287,000

Cash 287,000

b) 3/1 Cash 36,500

Accumulated depreciation 24,650

Machinery and equipment 58 000 ,

Gain on sale 3,150

c) 5/1 Repairs expense 50,000

Cash 50,000

d) 11/1 Land (380,000+23,000+35,000) 438,000

Cash 438,000

e) 12/31 Automobile‐new (15,250+3,750) 19,000

Accumulated depreciation 13,500

Loss on exchange (4,500‐3,750) 750

Automobile‐old 18,000

Cash 15,250

2.

PELL CORPORATION

Depreciation Expense

For the Year Ended December 31, 2016

Land improvements:

Cost $ 180,000

Straight-line rate (1 ÷ 15 years) x 6 2/3% $ 12,000

Building:

Book value 12/31/15 ($1,500,000 – 350,000) $1,150,000

150% declining balance rate:

(1 ÷ 20 years = 5% x 1.5) x 7.5% $ 86,250

Machinery and Equipment:

Balance, 12/31/15 $1,158,000

Deduct machine sold (58,000) $1,100,000

Straight-line rate (1 ÷ 10 years) x 10% 110,000

Purchased 1/2/16 287,000

Depreciation x 10% 28,700

Machine sold 3/31/16 58,000

Depreciation for three months x 2.5% 1,450

Total depreciation on machinery and equipment $140,150

Automobiles:

Book value on 12/31/15 ($150,000 – 112,000) $38,000

150% declining balance rate:

(1 ÷ 3 years = 33.333% x 1.5) x 50% $ 19,000

Total depreciation expense for 2016 $257,400

3.

I HOPE YOU UNDERSTAND...

PLS RATE THUMBS UP....ITS HELPS ME ALOT...

THANK YOU...!!

ekkarill92 answered 1 month ago

ekkarill92 answered 1 month agoRelated Solutions

The plant asset and accumulated depreciation accounts of Pell Corporation had the following balances at December...

The plant asset and accumulated depreciation accounts of Pell Corporation had the following balances at December...

The plant asset and accumulated depreciation accounts of Pell Corporation had the following balances at December...

The plant asset and accumulated depreciation accounts of Pell Corporation had the following balances at December...

The plant asset and accumulated depreciation accounts of Pell Corporation had the following balances at December...

The plant asset and accumulated depreciation accounts of Pell Corporation had the following balances at December...

The plant asset and accumulated depreciation accounts of Pell Corporation had the following balances at December...

The plant asset and accumulated depreciation accounts of Pell Corporation had the following balances at December...

he plant asset and accumulated depreciation accounts of Pell Corporation had the following balances at December...

At December 31, 2017, Cord Company's plant asset and accumulated depreciation and amortization accounts had balances...

- Problem 18-12 Various shareholders' equity topics; comprehensive [LO18-1, 18-4, 18-5, 18-6, 18-7, 18-8] Part A In...

- Hello There, This is discussion Question For Advanced Database Systems Question: (a) Please define what a...

- Physicians at a clinic gave what they thought were drugs to 860860 patients. Although the doctors...

- On January 1, 2018, bonds with a face value of $ 79,000 were sold. The bonds...

- How do I make this sort in true alphabetical order instead of ascii(ABCabc) order? I am...

- As a healthcare provider in physical therapy, athletic training, or as an exercise scientist and personal...

- in the market for makeup artists, what happens after the invention of high-definition tv allowing viewers...