Question

In: Economics

how do I solve problem # 10 in chapter 6 of the Essentials of Economics 10th...

how do I solve problem # 10 in chapter 6 of the Essentials of Economics 10th edition by Bradley R. Schiller? DO I need to make 2 graphs?

10. POLICY PERSPECTIVES Suppose that the monthly market demand schedule for Frisbees is

Price $8 $7 $6 $5 $4 $3 $2 $1

Quantity demanded 1,000

2,000 4,000 8,000

16,000 32,000 64,000

150,000

Suppose further that the marginal and average costs of Frisbee

production for every competitive firm are

Rate of output Marginal cost: 100 200 300 400 500 600

Marginal cost $2.00 $3.00 $4.00 $5.00 $6.00 $7.00

Average total cost $2.00 $2.50 $3.00 $3.50 $4.00 $4.50

Finally, assume that the equilibrium market price is $6 per

Frisbee. LO5

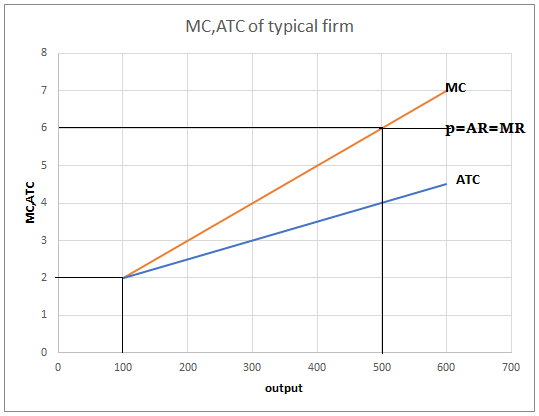

(a) Draw the cost curves of the typical firm.

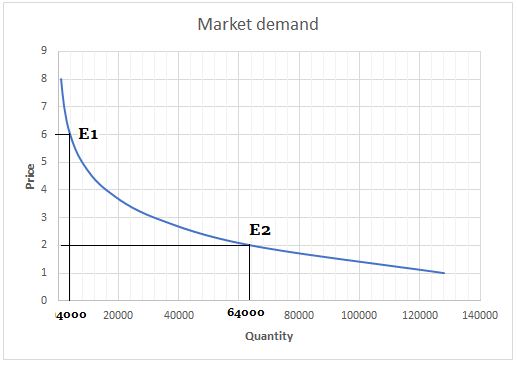

(b) Draw the market demand curve and identify market equilibrium.

(c) How many Frisbees are being sold in equilibrium?

(d) How many (identical) firms are initially producing Frisbees?

(e) How much profit is the typical firm making?

(f) In view of the profits being made, more firms will want to

get into Frisbee production. In the long run, these new firms will

shift the market supply curve to the right and push the price down

to minimum average total cost, thereby eliminating profits. At what

equilibrium price are all profits eliminated?

(g) How many firms will be producing Frisbees at this price?

Solutions

Expert Solution

(a)

The cost curves for the typical firm is given below+

b)

The market demand and price is given below

At market equilibrium P=6 and Q=4000 (point E1)

c)

At equilibrium there are 4000 freesbies being sold.

d)

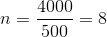

At equilibrium the price taker competitive firm produces the output for which P=MC. In this case P=MC=6. At this level a typical firm produces 500 units of output. The total market supply is 4000 units. Therefore, the number of firms producing freesbies (n) is

e)

At the output level of 500, the average total cost of production is ATC=4. Then per unit profit of a typical firm is P-ATC=$2. For 500 units the total profit is

f)

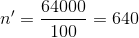

As new firm enters the market the price began to fall. The firm continue to enter as long as P>ATC. At long run P=ATC=MC. This occurs at P=ATC=2.

g)

A typical firm produces q=100 at this price, p=2. The total market demand is Q=64000. Then the number of firms is

Rahul Sunny answered 1 month ago

Rahul Sunny answered 1 month agoRelated Solutions

I am reviewing the International Economics textbook (10th edition), Chapter 14, Question 6. The question asks:...

Essentials of Business Communication (10th Edition) Chapter 3 How have market globalization and cultural diversity contributed...

Schiller, B. R. (2017). Essentials of economics (10th ed.). ECO 120 : Critical Reflection Differences between...

I would like the textbook solution to Auditing & Assurance Services 10th edition Chapter 21 problem...

how do I make a histogram. I am using the example from the book Essentials of...

I do not know how to solve this problem. A manufacture in Ontario has been fined...

Managerial economics - Chapter 3 - Problem 2

'an inside look' article page 118-119 chapter 4, essentials of economics 4th edition, Thinking critically question...

How can I solve this problem? Can you please show step by step how to solve...

I don't know how to solve this accounting problem. The problem is about Variance Analyses. Problem:...

- Hello There, This is discussion Question For Advanced Database Systems Question: (a) Please define what a...

- Physicians at a clinic gave what they thought were drugs to 860860 patients. Although the doctors...

- On January 1, 2018, bonds with a face value of $ 79,000 were sold. The bonds...

- How do I make this sort in true alphabetical order instead of ascii(ABCabc) order? I am...

- As a healthcare provider in physical therapy, athletic training, or as an exercise scientist and personal...

- in the market for makeup artists, what happens after the invention of high-definition tv allowing viewers...

- 10. What are the three monetary policy tools of the Fed? Briefly describe how each tool...