Question

In: Accounting

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

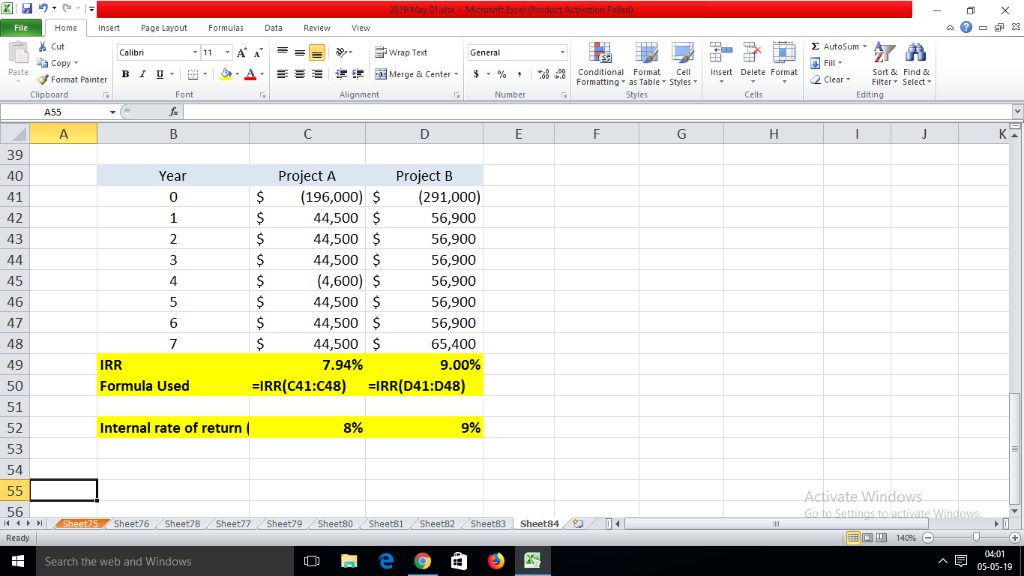

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would have an initial lower cost but would require a significant expenditure for rebuilding after 4 years. Option B would require no rebuilding expenditure, but its maintenance costs would be higher. Since the Option B machine is of initial higher quality, it is expected to have a salvage value at the end of its useful life. The following estimates were made of the cash flows. The company’s cost of capital is 5%. Option A Option B Initial cost $196,000 $291,000 Annual cash inflows $72,500 $82,500 Annual cash outflows $28,000 $25,600 Cost to rebuild (end of year 4) $49,100 $0 Salvage value $0 $8,500 Estimated useful life 7 years 7 years Click here to view PV table. Collapse question part (a) Compute the (1) net present value, (2) profitability index, and (3) internal rate of return for each option. (Hint: To solve for internal rate of return, experiment with alternative discount rates to arrive at a net present value of zero.) (If the net present value is negative, use either a negative sign preceding the number eg -45 or parentheses eg (45). Round answers for present value and IRR to 0 decimal places, e.g. 125 and round profitability index to 2 decimal places, e.g. 12.50. For calculation purposes, use 5 decimal places as displayed in the factor table provided.) Net Present Value Profitability Index Internal Rate of Return Option A $ % Option B $ %

Solutions

Expert Solution

| Project A | A | |||||

| Year | Annual cash inflows | Annual cash outflows | Cost of rebiuld | Net Cash flow | PV factor @ 5% | Present Value |

| 1 | $ 72,500 | $ (28,000) | $ 44,500 | 0.95238 | $ 42,381 | |

| 2 | $ 72,500 | $ (28,000) | $ 44,500 | 0.90703 | $ 40,363 | |

| 3 | $ 72,500 | $ (28,000) | $ 44,500 | 0.86384 | $ 38,441 | |

| 4 | $ 72,500 | $ (28,000) | $ (49,100) | $ (4,600) | 0.82270 | $ (3,784) |

| 5 | $ 72,500 | $ (28,000) | $ 44,500 | 0.78353 | $ 34,867 | |

| 6 | $ 72,500 | $ (28,000) | $ 44,500 | 0.74622 | $ 33,207 | |

| 7 | $ 72,500 | $ (28,000) | $ 44,500 | 0.71068 | $ 31,625 | |

| Present Value of Net Cash inflow | $ 217,100 | |||||

| Present Value of Net Cash inflow | $ 217,100 | |||||

| Less: Initial cost | $ 196,000 | |||||

| Net present value | $ 21,100 | |||||

| Present Value of Net Cash inflow | $ 217,100 | |||||

| Divided by: Initial cost | $ 196,000 | |||||

| Profitability index | 1.11 | |||||

| Project B | B | |||||

| Year | Annual cash inflows | Annual cash outflows | Salvage value | Net Cash flow | PV factor @ 5% | Present Value |

| 1 | $ 82,500 | $ (25,600) | $ 56,900 | 0.95238 | $ 54,190 | |

| 2 | $ 82,500 | $ (25,600) | $ 56,900 | 0.90703 | $ 51,610 | |

| 3 | $ 82,500 | $ (25,600) | $ 56,900 | 0.86384 | $ 49,152 | |

| 4 | $ 82,500 | $ (25,600) | $ 56,900 | 0.82270 | $ 46,812 | |

| 5 | $ 82,500 | $ (25,600) | $ 56,900 | 0.78353 | $ 44,583 | |

| 6 | $ 82,500 | $ (25,600) | $ 56,900 | 0.74622 | $ 42,460 | |

| 7 | $ 82,500 | $ (25,600) | $ 8,500 | $ 65,400 | 0.71068 | $ 46,478 |

| Present Value of Net Cash inflow | $ 335,285 | |||||

| Present Value of Net Cash inflow | $ 335,285 | |||||

| Less: Initial cost | $ 291,000 | |||||

| Net present value | $ 44,285 | |||||

| Present Value of Net Cash inflow | $ 335,285 | |||||

| Divided by: Initial cost | $ 291,000 | |||||

| Profitability index | 1.15 | |||||

ekkarill92 answered 4 months ago

ekkarill92 answered 4 months agoRelated Solutions

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

Brooks Clinic is considering investing in new heart-monitoring equipment. It has two options. Option A would...

- . 1. Provide an example of any two leading companies from the same industry, which are...

- Suppose Elon Musk is spectacularly successful, and electric vehicle technology follows the technology diffusion model we’ve...

- Starting from rest, a basketball rolls from the top to the bottom of a hill, reaching...

- Ray Company provided the following excerpts from its Production Department’s flexible budget performance report. (Round "rate...

- Give an examples of Altruism on a macro level, and micro level, and how the concept...

- QUESTION In process improvement efforts, quality costs or cost of quality is a means to quantify...

- Lightning is a great illustration from nature of the stunning application of statics and electric fields....