Question

In: Accounting

Required: Make necessary journal entries including the necessary adjusting entries, post them to their respective general...

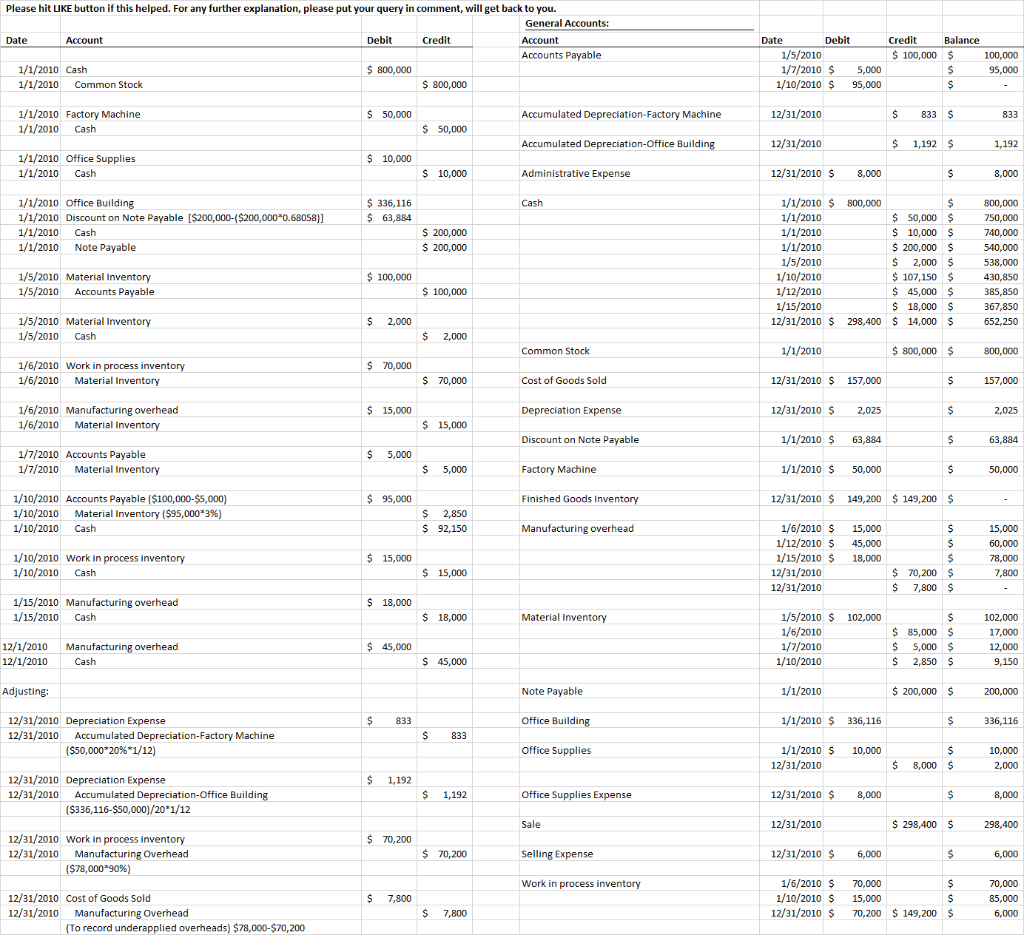

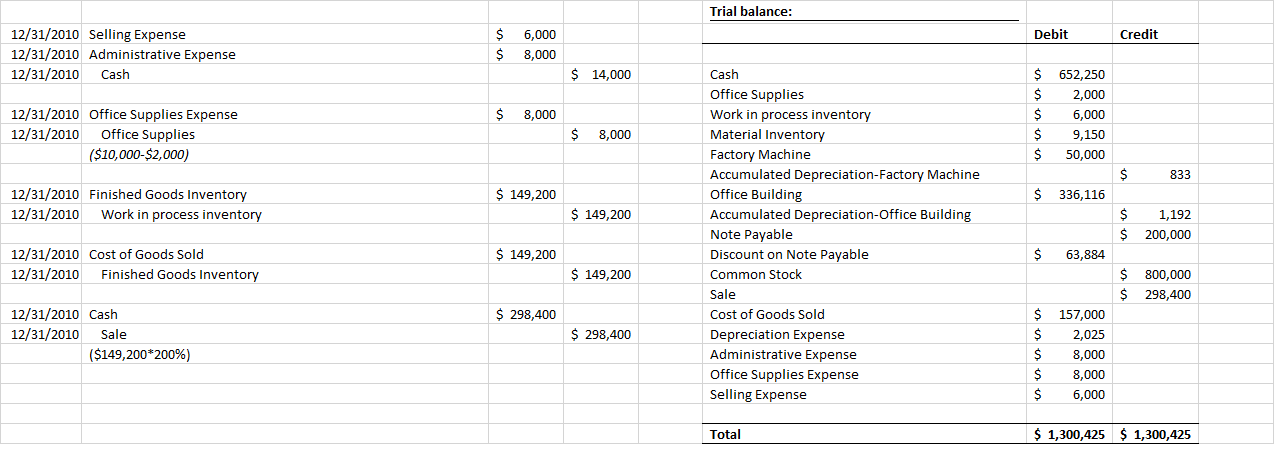

Required: Make necessary journal entries including the necessary adjusting entries, post them to their respective general ledger accounts and prepare only an adjusted trial balance. 1. Using the following information, complete the accounting cycle.

Jan 1, 2010 Sold Common Stock to raise capital in the amount of $800,000. Jan 1 Purchased Factory machinery for $50,000. The machinery has a life of 10 years, residual value of $10,000, and the company uses double declining balance method of depreciation. Jan 1 Purchased Office Supplies for $10,000 for cash Jan 1 Purchased Office Building for $400,000, making a down payment of $200,000 and giving a promissory note to be paid at once at the end of 5 years. The market interest rate at the time of the purchase is 8%. The office building has a life of 20 years, salvage value of $50,000, and the company uses straight line method of depreciation. Jan 5 Purchased Materials from William Martin for $100,000, term 3/10, EOM, FOB shipping point. The transportation incurred and paid is $2,000. Jan 6 Requisitioned for $70,000 direct materials which were put into production process. Jan 6 Requisitioned for $15,000 Indirect materials which were put into production process. Jan 7 Returned $5,000 of the materials to William Martin for defectiveness. Jan 10 Paid William Martin the amount due. Jan 10 Paid direct labor cost of $15,000. Jan 15 Paid indirect labor cost of $18,000. Jan 12 Paid other factory overhead of $45,000. Jan 31 Make necessary entries for depreciation adjustments for both machinery as well as office building. Additional Information: Applied 90% of the actual factory overhead to the production process. The over or under-applied overhead is considered immaterial and this information should be considered in determining how the over-or under-applied overhead would be disposed off. Jan 31 Paid selling expenses of $6,000 and administrative expenses of $8,000. Jan 31. The unused office supplies is $2,000 and the work in process at the end of the period is $6,000. Jan 31. Sold 60% of the goods available for sale at 200% of their cost for cash.

Solutions

ekkarill92 answered 4 months ago

ekkarill92 answered 4 months agoRelated Solutions

Record the adjusting entries in the general journal and post them to the ledger accounts and...

Record February transactions in the General Journal and post to the General Ledger. Record adjusting entries...

using the below transaction, you are required to post the journal entries to respective ledger accounts....

Why is it necessary to journalize and post adjusting entries?

Prepare General Journal Entries for the following transactions. Then post the journal entries to the General...

Part 1 – General Journal – Post the following journal entries to the general journal. ...

1. Prepare the necessary adjusting journal entries for items a through h. Assume that adjusting entries...

Required: 1. & 2. Prepare journal entries to record the transactions for April and post them...

a. Make the necessary journal entries for the following transactions:

Part 2 – General Journal (LO3-2) – Post the following journal entries to the general journal....

- Python previous function: wrtie a function that takes one argument. The function returns True if the...

- A professional couple wishes to purchase a new home costing $750,000, make a 20 percent down...

- Padre holds 100 percent of the outstanding shares of Sonora. On January 1, 2016, Padre transferred...

- Question: Use backtracking algorithm design to write Java code to solve the subset problem: given a...

- Patsy Ltd. produces ice-cream and would like to accurately forecast sales so that it can meet...

- Power Music owns five music stores, where it sells music, instruments, and supplies. In addition, it...

- 4) A client wants to finance the purchase of a house costing $50,000 over a period...