Question

In: Finance

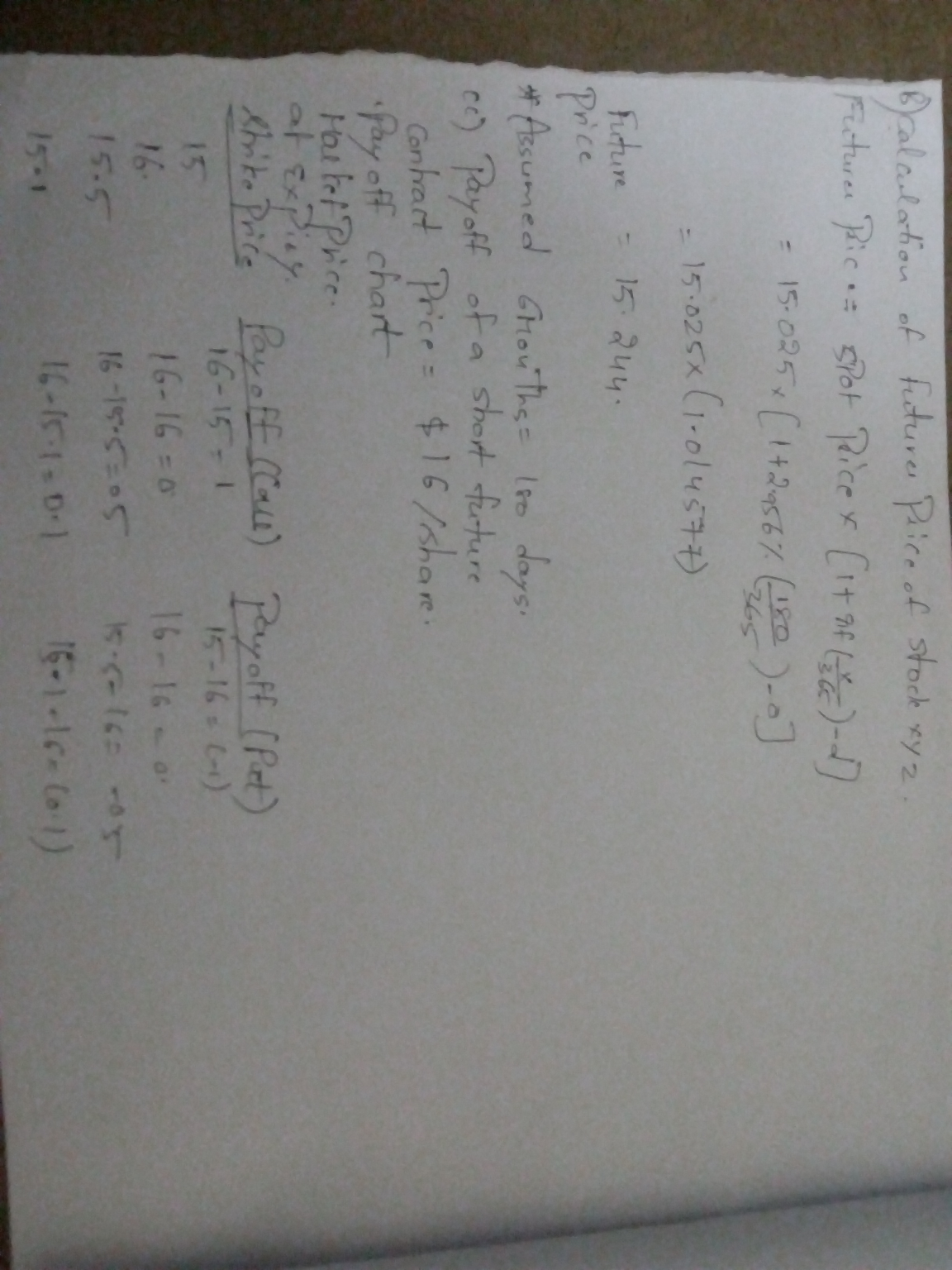

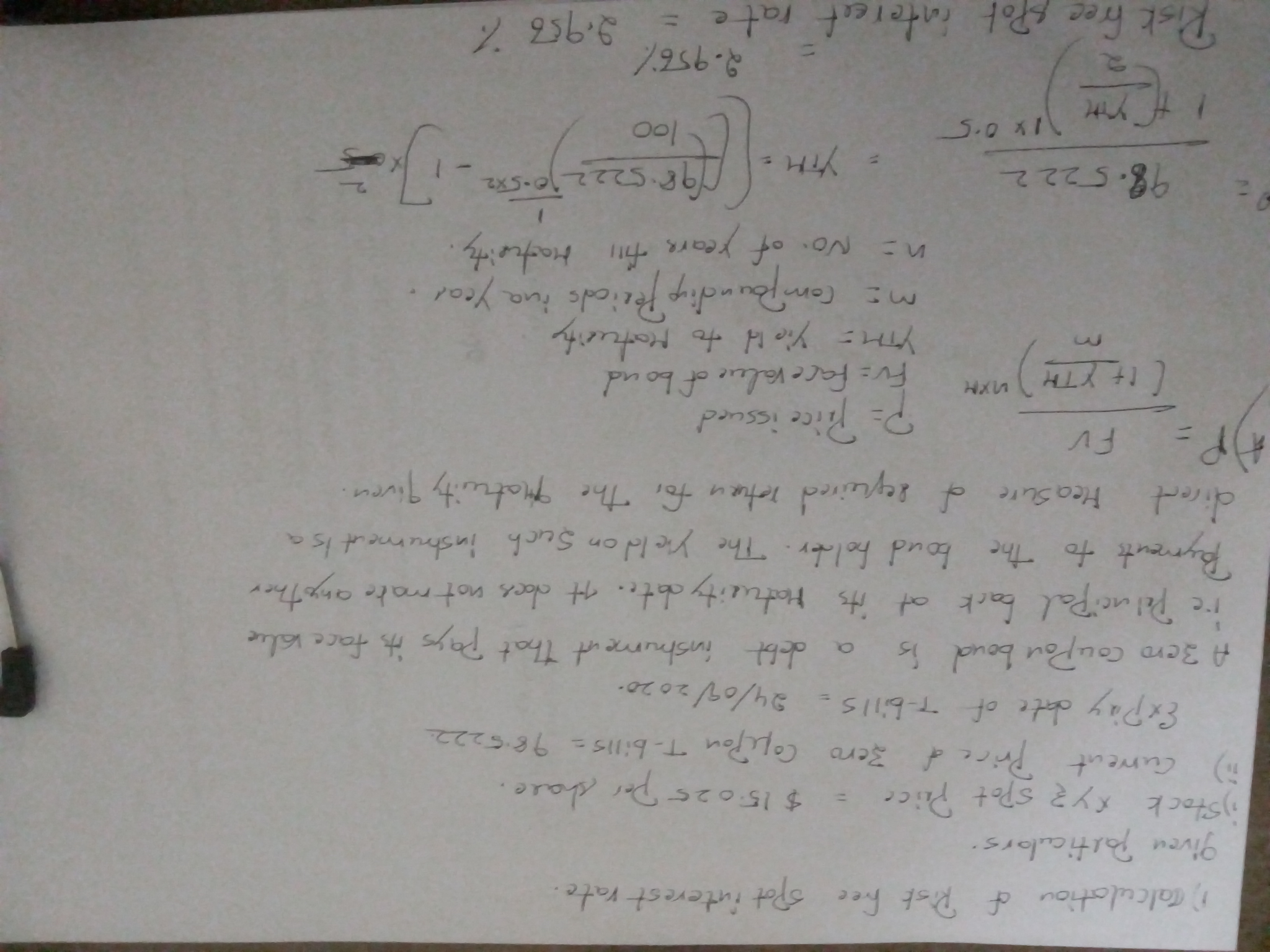

Consider the stock XYZ, which pays no dividends. It is currently trading at $15.025 per share....

- Consider the stock XYZ, which pays no dividends. It is currently trading at $15.025 per share. The following questions refer to options and futures on this stock that expire on 9/24/2020. You may assume that this is exactly 6 months or .5 years from now in calculations.

a. Zero-coupon T-bills expiring on 9/24/2020 are currently selling

for 98.5222. What is the risk-free spot interest rate?

b. What is the futures price of XYZ?

c. You want to mimic the payoff of a short

future with a contract price of $16/share. How can you do this

using only puts and calls? You may assume any strike is

available.

Solutions

jeff jeffy answered 3 weeks ago

jeff jeffy answered 3 weeks agoRelated Solutions

Moutainbrook Company stock is is currently trading at $44 per share. The stock pays no dividends....

Moutainbrook Company stock is is currently trading at $44 per

share. The stock pays no dividends. The standard deviation of the

returns on the stock is 55%. The continuously compounded interest

rate is 6% per year. A three-year European call option on

Mountainbrook stock has a strike price of $50 per share. Using the

Black-Scholes-Merton model, find the premium per share to four

decimal places.

Suppose Amazon stock is trading for $ 535 per share, and Amazon pays no dividends. a....

Suppose Amazon stock is trading for $ 535 per share, and Amazon

pays no dividends.

a. What is the maximum possible price of a call option on

Amazon?

b. What is the maximum possible price of a put option on Amazon

with a strike price of $ 590?

c. What is the minimum possible value of a call option on Amazon

stock with a strike price of $ 500?

d. What is the minimum possible value of an American put...

A stock is currently trading at 36$/share, has annual volatility of 17% and pays no dividends....

A stock is currently trading at 36$/share, has annual volatility

of 17% and pays no dividends. The risk-free rate is 6% p.a.

continuously compounded and an option trader writes a three-month

call which is $4 out-of-the money. What should be the price of this

call? What should be the price of this call as a percentage of the

current stock price?

(a) Consider a stock that pays annual dividends. It just paid $4.50 dividends per share, and...

(a) Consider a stock that pays

annual dividends. It just paid $4.50 dividends per share, and the

next dividend will be paid in 1 year. The dividends are expected to

remain constant at $4.50 per share for the next 10 years, after

which the dividends are expected to decrease at a rate of 0.5% per

year. The annual cost-of-capital is 15.50%. Find the fair value of

the stock today.

(b) Consider the same stock as

described in part (a), except...

(a) Consider a stock that pays annual dividends. It just paid $4.50 dividends per share, and...

(a) Consider a stock that pays annual dividends. It just paid

$4.50 dividends per share, and the next dividend will be paid in 1

year. The dividends are expected to remain constant at $4.50 per

share for the next 10 years, after which the dividends are expected

to decrease at a rate of 0.5% per year. The annual cost-of-capital

is 15.50%. Find the fair value of the stock today.

(b) Consider the same stock as described in part (a), except...

(a) Consider a stock that pays annual dividends. It just paid $4.50 dividends per share, and...

(a) Consider a stock that pays

annual dividends. It just paid $4.50 dividends per share, and the

next dividend will be paid in 1 year. The dividends are expected to

remain constant at $4.50 per share for the next 10 years, after

which the dividends are expected to decrease at a rate of 0.5% per

year. The annual cost-of-capital is 15.50%. Find the fair value of

the stock today.

(b) Consider the same stock as

described in part (a), except...

XYZ company has 10,000 shares of stock currently trading at $10 per share. They have a...

XYZ company has 10,000 shares of stock currently trading at $10

per share. They have a beta of 1, expected market return of 10% and

a 3% risk free rate. XYZ also has 50 shares of debt outstanding

currently trading at $1000 per share. Their bonds have semiannual

bonds with a $1,000 par value, 5% coupon rate, and 10 years to

maturity. The firm's marginal tax rate is 22 percent. Calculate the

weighted average cost of capital (WACC). ENTER YOUR...

Consider a stock that pays no dividends and currently sells for S0. The forward on this...

Consider a stock that pays no dividends and currently sells for

S0. The forward on this stock for date-T delivery has the forward

price F0 that is greater than S0erT . Suppose that short selling

for this stock is NOT allowed in the market. For the forward, we

can either long or short. Here, we can make an arbitrage Is this

true or false?

ZAZ stock is currently trading at $163 per share. A dividend of $1.47 per share is...

ZAZ stock is currently trading at $163 per share. A dividend of

$1.47 per share is expected to be paid on the stock in two months.

A three month European put option with $165 strike on ZAZ is

trading at $1 in the options market.

1. Does an arbitrage opportunity exist regarding securities

markets for T-Bills, ZAZ stock and this put option? Explain

2. Completely specify a set of trades now that exploit the

arbitrage opportunity.

3. Compute the profit...

Consider an investor who owns stock XYZ. The stock is currently trading at $120. The investor...

Consider an investor who owns stock XYZ. The stock is currently

trading at $120. The investor worries that the outlooks for the

market and the stock are not favorable. The investor decides to

protect his potential losses by using derivatives.

Assume the investor decided to purchase a European call option

on stock ABC. Further assume that the current price of the stock is

$130. The investor paid $10 for the call with the strike price at

$155.

(A)If the stock...

ADVERTISEMENT

ADVERTISEMENT

Latest Questions

- A rural 6-lane divided highway with AADT = 30,000 veh/ day, with composition [(80% PC –...

- *VISUAL BASIC* Construct and instantiate an array of strings called afcSouth that contains the following information...

- LAG network inc. balance sheet and income statement are as follows: LAG network inc. income statement...

- Calculate the pH at the equivalence point in titrating 0.110 M solutions of each of the...

- why joints differ in their degree of mobility.

- How do customers typically respond to service failures? When a service failure occurs, what can firms...

- Some discarded solid chemical waste dissolves slowly in a large drain pipe in which the water...

ADVERTISEMENT