Question

In: Finance

A graph, plotting a the relationship between a bond’s modified duration and its tenor for a...

-

A graph, plotting a the relationship between a bond’s modified duration and its tenor for a (10) zero, (10) discount bond, (10) premium bond and (10) perpetuity

-

In (10 per) writing, and by (5 per) showing numerical analysis, explain what drives the shape of the four curves you plotted in part 1

Solutions

Expert Solution

-

Duration is a measure of a bond's interest rate sensitivity. It provides an estimate how much a bond’s price is likely to rise or fall if interest rates change

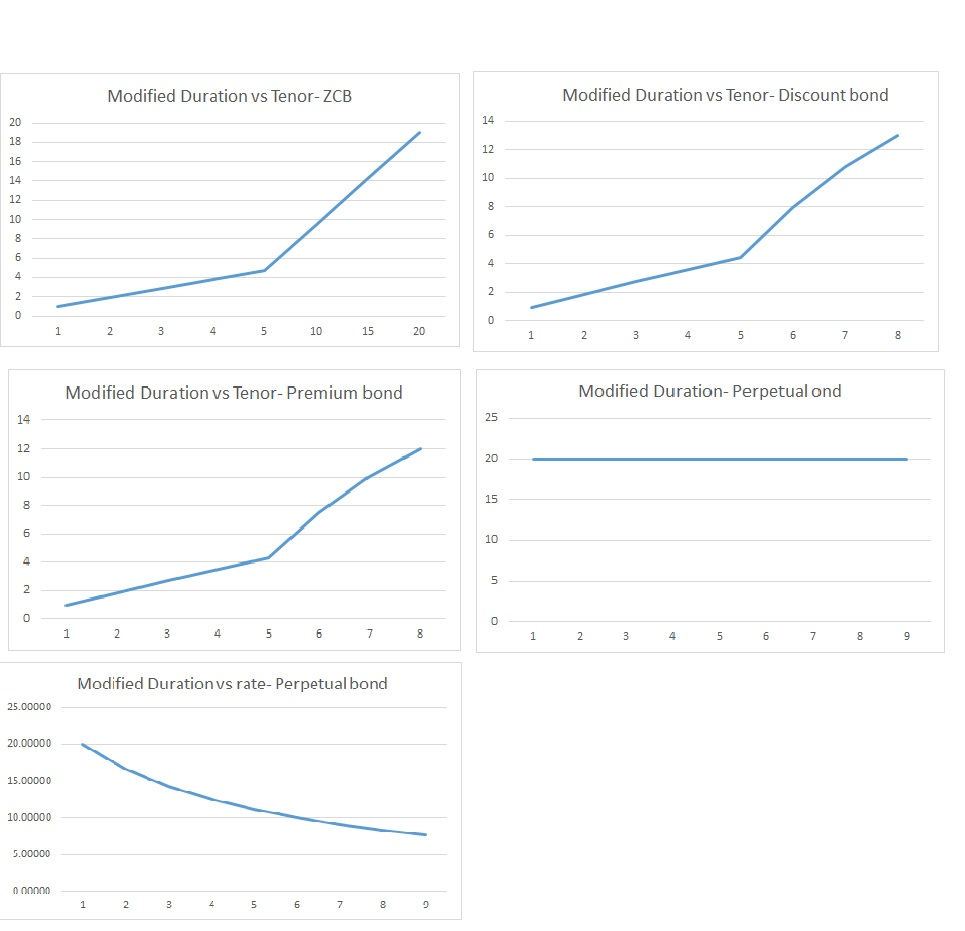

ZCB settlment date maturity date Years to maturity coupon yield frequency (annual) Macaulay Duration Modified Duration Slope of the curve= y/x= duration/ tenor 2/7/2019 2/7/2020 1 0% 5% 1 1.0000 0.9524 0.9524 2/7/2019 2/6/2021 2 0% 5% 1 1.9972 1.9048 0.9524 2/7/2019 2/6/2022 3 0% 5% 1 2.9972 2.8571 0.9524 2/7/2019 2/6/2023 4 0% 5% 1 3.9972 3.8095 0.9524 2/7/2019 2/6/2024 5 0% 5% 1 4.9972 4.7619 0.9524 2/7/2019 2/4/2029 10 0% 5% 1 9.9917 9.5238 0.9524 2/7/2019 2/3/2034 15 0% 5% 1 14.9889 14.2857 0.9524 2/7/2019 2/2/2039 20 0% 5% 1 19.9861 19.0476 0.9524 discount bond settlment date maturity date Years to maturity coupon yield frequency (annual) Macaulay Duration Modified Duration Slope of the curve= y/x= duration/ tenor 2/7/2019 2/7/2020 1 4% 5% 1 1.0000 0.9524 0.9524 2/7/2019 2/6/2021 2 4% 5% 1 1.9584 1.8678 0.9339 2/7/2019 2/6/2022 3 4% 5% 1 2.8816 2.747 0.9157 2/7/2019 2/6/2023 4 4% 5% 1 3.7677 3.5909 0.8977 2/7/2019 2/6/2024 5 4% 5% 1 4.6175 4.4003 0.8801 2/7/2019 2/4/2029 10 4% 5% 1 8.3513 7.9615 0.7962 2/7/2019 2/3/2034 15 4% 5% 1 11.3278 10.799 0.7199 2/7/2019 2/2/2039 20 4% 5% 1 13.6668 13.0292 0.6515 premium bond settlment date maturity date Years to maturity coupon yield frequency (annual) Macaulay Duration Modified Duration Slope of the curve= y/x= duration/ tenor 2/7/2019 2/7/2020 1 6% 5% 1 1.0000 0.9524 0.9524 2/7/2019 2/6/2021 2 6% 5% 1 1.9411 1.8513 0.9257 2/7/2019 2/6/2022 3 6% 5% 1 2.8330 2.7007 0.9002 2/7/2019 2/6/2023 4 6% 5% 1 3.6765 3.504 0.8760 2/7/2019 2/6/2024 5 6% 5% 1 4.4750 4.2645 0.8529 2/7/2019 2/4/2029 10 6% 5% 1 7.8838 7.5163 0.7516 2/7/2019 2/3/2034 15 6% 5% 1 10.5301 10.0392 0.6693 2/7/2019 2/2/2039 20 6% 5% 1 12.6080 12.0208 0.6010 perpetuity bond settlment date maturity date Years to maturity coupon yield frequency (annual) Macaulay Duration Modified Duration 2/7/2019 - 1 5% 5% 1 21.0000 20 6.00% 20 7.00% 20 8.00% 20 9.00% 20 10.00% 20 11.00% 20 12.00% 20 13.00% 20 settlment date maturity date Years to maturity coupon yield frequency (annual) Macaulay Duration Modified Duration 2/7/2019 - 1 5% 5% 1 21.0000 20 6.00% 20 7.00% 20 8.00% 20 9.00% 20 10.00% 20 11.00% 20 12.00% 20 13.00% 20 Explanation- for zero coupon bond, the relationship between the tenor and modified duration is linear with slope of the curve being almost equal to one and modified duration being slightly lower than the tenor. This is because, the changes in interest rate do not impact the price of a zcb as there are no coupon payments.

Explanation- for discount bond, the relationship between the tenor and modified duration is linear with slope of the curve being less than one. The slope of the curve goes decreasing at an increasing pace as the tenor increases. This is because the impact of difference between yield and coupon rate gets magnified as the tenor increases.

Explanation- for premium bond, the relationship between the tenor and modified duration is linear with slope of the curve being less than one. The slope of the curve goes decreasing at an increasing pace as the tenor increases, at a rate greater than that for a discount bond. This is because the impact of difference between yield and coupon rate gets magnified as the tenor increases, more than that for a discount bond.

Explanation- for perpetual bond, there is not relationship between the tenor and duration of the bond as the tenor is technically infinite. Hence, the curve is a straight horizontal line. A more appropriate relationship is between the duration and the yield of the bond. the relationship between the 2 is inverse i.e. modified duration= 1/rate Note-

pay attention to the horizontal scale. The tenor is not changing at

a linear scale after 5 years. This is done to emphasis on a rate of

change of duration with tenor

Note-

pay attention to the horizontal scale. The tenor is not changing at

a linear scale after 5 years. This is done to emphasis on a rate of

change of duration with tenor

jeff jeffy answered 3 weeks ago

jeff jeffy answered 3 weeks agoRelated Solutions

1. A graph, plotting the relationship between a bond’s modified duration and its tenor for a...

6. a) What is duration? What is modified duration?

What is the difference between absorption and emission? Transmission and reflection? When plotting a graph of...

what is the difference between absorption and emission? transmission and reflection? when plotting a graph of...

Describe the differences between Macaulay, modified and effective duration. Explain the difference between positive and negative...

The relationship between marginal social cost and marginal social benefit by plotting the necessary graphics

Which of the following is true about duration and modified duration? I. The Macaulay duration calculates...

When is duration appropriate for estimating the bond’s sensitivity to changes in interest rates.

Compute the Macaulay duration and modified duration of a 6%, 25-year bond selling at a yield...

-Whot should have an understanding of duration, modified duration and convexity. - Who should be able...

- Write a Python program to implement a form of a Roman numeral calculator. We are using...

- The neutralization of H3PO4 with KOH is exothermic. 55.0 mL of 0.213 M H3PO4 is mixed...

- Jeremy earned $102,100 in salary and $8,100 in interest income during the year. Jeremy’s employer withheld...

- Some bacteria only have capsules while actively infecting a host but not when grown in a...

- College physics 1) A 600 g model rocket is on a cart that is rolling to...

- I- + NO3- ? I2 + NO Note: I2 is elemental Indicate the numeric coefficient in...

- STOICHIOMETERY QUESTION :-When aluminum metal is added to sulphuric acid, hydrogen gas and aluminum sulphate is...