Question

In: Economics

A society has 2 goods, A and B, for two people, Larry and Javier. The price...

A society has 2 goods, A and B, for two people, Larry and Javier. The price of A and B are PA = $4 and PB = $10. Larry’s utility function is UL(A, B) = 40X0.25B0.5 and income is YL = $600. Javier’s utility function is UJ(A, B) = A0.5B0.5 and income is YJ = $2,400. Marginal utilities for Larry and Xavier are:

Larry: MUA = 10A-0.75B0.5 and MUB = 20A0.25B-0.5

Xavier: MUA = 0.5A-0.5B0.50 and MUB = 0.5A0.5B-0.5

- Find the utility maximizing consumption choices of A and B for Larry and Javier. Explain your work.

- Currently in this economy, there are 300 units of good A supplied and 200 units of good B supplied. Given the consumption demands for A and B above, is this economy in a competitive equilibrium? If so, explain why. If not, explain how prices and outputs will adjust to move toward an equilibrium.

- Draw the situation described in parts a and b in an Edgeworth Box.

Solutions

Expert Solution

a. Consumer 1's problem:

At equilibrium, marginal rate of substitution is equal to the price ratio:

Substituting the value of y into consumer 1's budget line:

Consumer 2's problem:

At equilibrium, MRS is equal to price ratio:

Substituting the value of y into consumer 2's budget line:

b. The market for a good is in equilibrium when its demand and supply are equal. If the market demand is greater or less than the market supply, the market for that good is not in equilibrium.

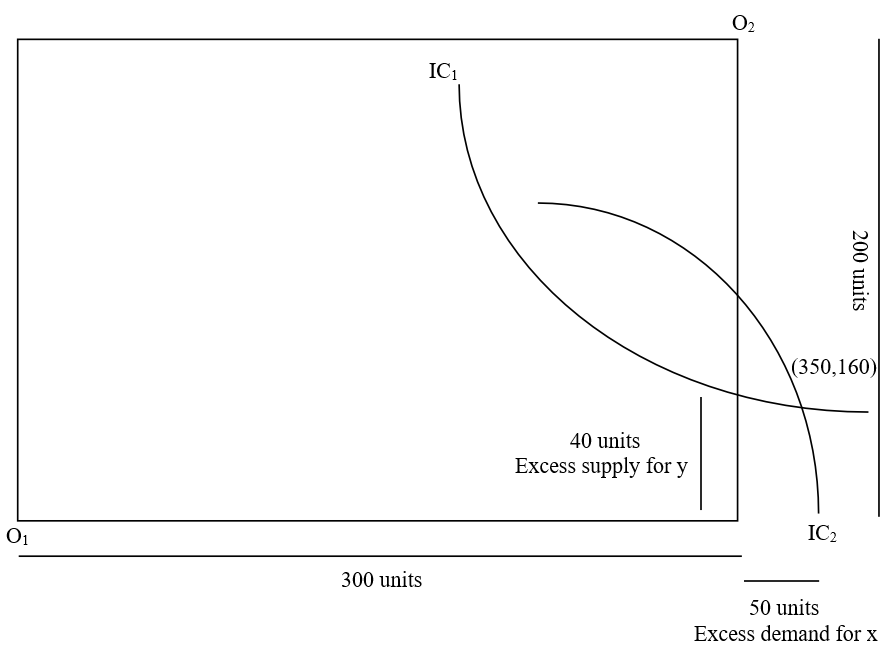

Total quantity available in the market of x is 300, total quantity demanded in the market of x is 350. Therefore, the market for x is not in equilibrium. Total quantity available of y is 200, total quantity demanded in the market of y is 160. Therefore, the market for y is not in equilibrium.

Therefore, this economy is not in a competitive equilibrium as markets for x and y are not in equilibrium. The market for x has excess demand and the market for y has excess supply.

Since there exists an excess demand for x in the economy, the price of x will increase till the point demand for x and supply of x are both equal to 300. Similarly, there is excess supply of y in the economy. Therefore, price of y will decrease till the point where demand for y and supply of y are both equal to 200 in the market. Hence, at equilibrium:

c. The following image shows an Edgeworth Box describing the situation in the previous parts:

Rahul Sunny answered 3 months ago

Rahul Sunny answered 3 months agoRelated Solutions

11. Consider an exchange economy consisting of two people, A and B, endowed with two goods,...

1. Assume a society in which consumers partake of only two goods, bread (B) and wine...

Suppose you have a world with two goods, A and B. Suppose the price of good...

If goods A and B are complements, an increase in the price of A will result...

1. (Public Goods Game) Suppose that there are two people, Agent 1 and Agent 2 in...

(a) Let U(A,B) = (A)^1/3 (B)^2/3 , where A and B are two distinct consumption goods....

2. In the oligopoly market, only two companies A and B produce goods of the same...

A simple economy has two goods, food (F) and soda (S) and two people, Jesse and Presly.

The profit motive is: A.ineffective at producing consumer goods B. inherently beneficial to society if left...

A consumer has an income of $120 to buy two goods (X, Y). the price of...

- The half-life of mercury-197 is 64.1 hours. If a patient undergoing a kidney scan is given...

- Double bonds react with Br2 to form a dibromide. Isobutylene undergoes cationic polymerization under conditions where...

- 1. Which sex chromosomes are limited to only one sex? A. X and Z B. X...

- prepare a tecnical report that discuss about "A custom Union (CU) constitute a partial movement towards...

- in your own opinion, It has been said that a smartphone is a computer in your...

- Use the internet to read more about journaling file systems such as NTFS, extfs2, and extfs3....

- Consider the quick sort algorithm. The quick sort algorithm is a divide and conquer approach which...