Question

In: Math

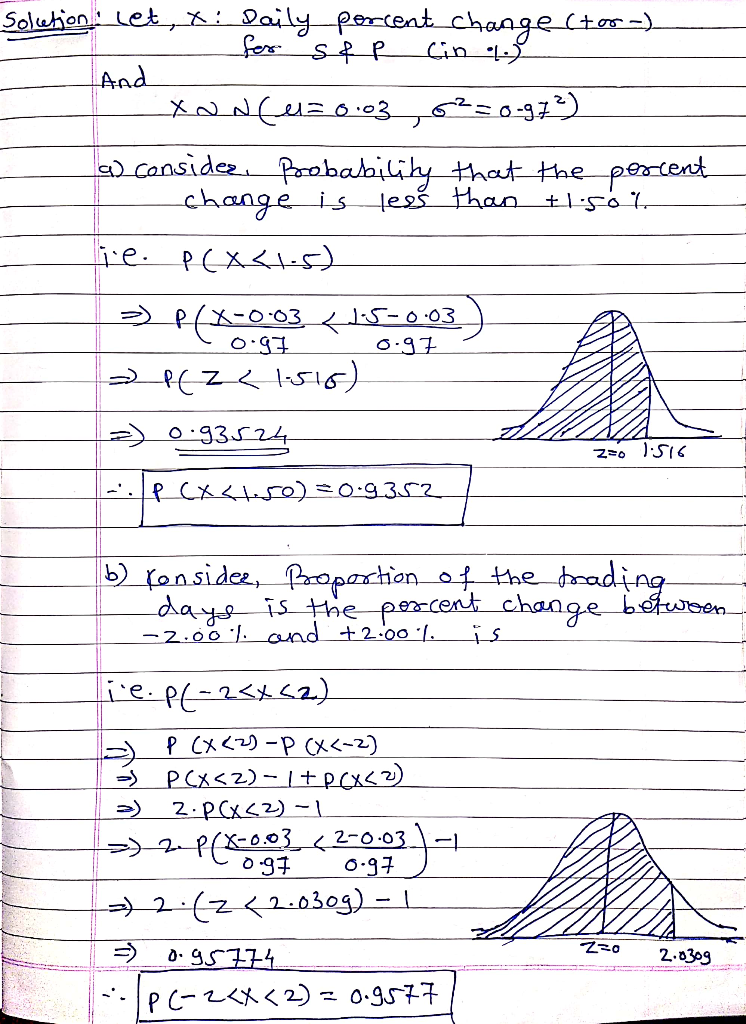

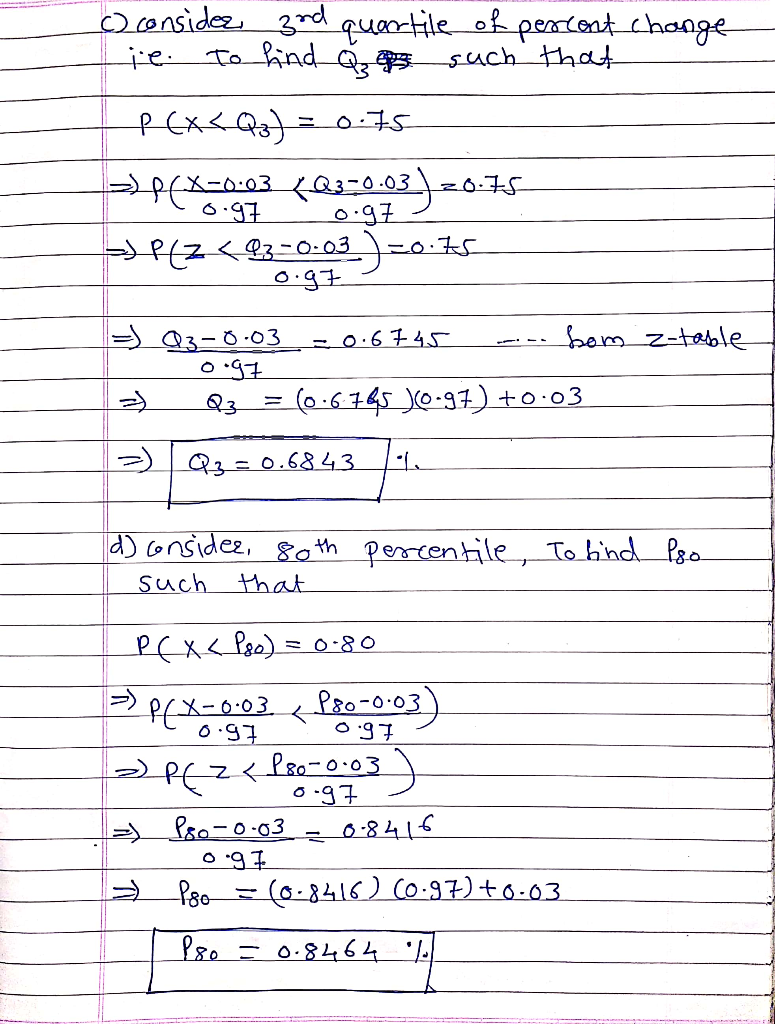

Suppose that over a year the daily percent change (+ or -) for the S&P 500...

Suppose that over a year the daily percent change (+ or -) for

the S&P 500 adjusted closing value is approximately normally

distributed with a mean of +0.03% and a standard deviation of

0.97%. Use this model to answer the following questions. Show all

calculations. Show the standardization calculations.

a) For a randomly selected trading day, what the is probability

that the percent change is less than +1.50%?

b) For what proportion of the trading days is the percent change between -2.00% and +2.00%?

c) What is the 3rd quartile of the percent change?

d) The 80th percentile?

Solutions

Expert Solution

a) 0.9352

b) 0.9577

c) Q3= 0.6843%

d) P80 = 0.8464 %

milcah answered 5 months ago

milcah answered 5 months agoRelated Solutions

Below are the closing values and daily return on the S&P 500 for the last ten...

Below are the closing values and daily return on the S&P 500

for the last ten days. What are the daily and annualized

standard deviations? You may use excel for this problem.

Enter your answers as percent rounded to two decimal places.

Date

Closing value

Return

9/25/2019

2984.87

0.0062

9/26/2019

2977.62

-0.0024

9/27/2019

2961.79

-0.0053

9/30/2019

2976.74

0.0050

10/1/2019

2940.25

-0.0123

10/2/2019

2887.61

-0.0179

10/3/2019

2910.63

0.0080

10/4/2019

2952.01

0.0142

10/7/2019

2938.79

-0.0045

10/8/2019

2893.06

-0.0156

The following table shows the annual returns over a six year period for the S&P 500...

The following table shows the annual

returns over a six year period for the S&P 500 market index and

MCH, Inc. Assume that the historical information represents a

population. Use this data to calculate the correlation between both

sets of security returns. Discuss your findings.

Year

S&P

500

MCH,

Inc.

2013

0.15

0.37

2014

0.13

0.09

2015

0.14

-0.11

2016

-0.09

0.08

2017

0.12

0.11

2018

0.09

0.04

Please show me each step. Thank you

The following table shows the annual returns over a six year period for the S&P 500...

The following table shows the annual

returns over a six year period for the S&P 500 market index and

MCH, Inc. Assume that the historical information represents a

population. Use this data to calculate the correlation between both

sets of security returns. Discuss your findings.

Year

S&P

500

MCH,

Inc.

2013

0.15

0.37

2014

0.13

0.09

2015

0.14

-0.11

2016

-0.09

0.08

2017

0.12

0.11

2018

0.09

0.04

Suppose the value of the S&P 500 Stock Index is currently $3,350. a. If the one-year...

Suppose the value of the S&P 500 Stock Index is currently

$3,350.

a. If the one-year T-bill rate is 4.6% and the

expected dividend yield on the S&P 500 is 4.2%, what should the

one-year maturity futures price be? (Do not round

intermediate calculations. Round your answer to 2 decimal

places.)

b. What would the one-year maturity futures price

be, if the T-bill rate is less than the dividend yield, for

example, 3.2%? (Do not round intermediate calculations.

Round your...

The S&P 500 and Nohr Corp had the following returns over the past five years Year ...

The S&P 500 and Nohr Corp had the following returns over the

past five years

Year S&P

500

Nohr

.12

.23

.01

-.05

.18

.20

.09

.12

.10

.20

a. What was the mean AND standard

deviation of returns (population version)

for Nohr for the 5 years?

b. What was the beta of Nohr relative to the S&P 500?

c. What was the geometric mean return for Nohr

for the 5 years?

Suppose you invest $15,000 in an S&P 500 Index fund (S&P fund) and $10,000 in a...

Suppose you invest $15,000 in an S&P 500 Index fund (S&P

fund) and $10,000 in a total bond market fund (Bond fund). The

expected returns of the S&P and Bond funds are 8% and 4%,

respectively. The standard deviations of the S&P and Bond funds

are 18% and 7% respectively. The correlation between the two funds

is 0.40. The risk-free rate is 2%. What is the expected return on

your portfolio? What is the standard deviation on your portfolio?

What...

The Daily S&P 500® Bull 3x ETF seeks daily investment results, before fees and expenses, of...

The Daily S&P 500® Bull 3x ETF seeks daily investment

results, before fees and expenses, of 300% of the performance of

the S&P 500® Index and Daily S&P 500® Bear 3x ETF seeks

daily investment results, before fees and expenses, of 300% of the

inverse (or opposite) of the performance of the S&P 500® Index.

For the purposes of this question, disregard the effects of

expenses and fees. Let the returns on S&P 500® Index on three

consecutive days be,...

Suppose the value of the S&P 500 Stock Index is currently $2,050. If the one-year T-bill...

Suppose the value of the S&P 500 Stock Index is currently

$2,050. If the one-year T-bill rate is 5.5% and the expected

dividend yield on the S&P 500 is 5.0%.

a. What should the one-year maturity futures

price be? (Do not round intermediate

calculations.)

Futures price

$

b. What would the one-year maturity futures

price be, if the T-bill rate is less than the dividend yield, for

example, 4.0%? (Do not round intermediate

calculations.)

Futures price

Suppose that the S&P 500, with a beta of 1.0, has an expected return of 12%...

Suppose that the S&P 500, with a beta of 1.0, has an expected return of 12% and T-bills provide a risk-free return of 3%.

a.

What would be the expected return and beta of portfolios constructed from these two assets with weights in the S&P 500 of (i) 0; (ii) .25; (iii) .50; (iv) .75; (v) 1.0? (Leave no cells blank - be certain to enter "0" wherever required. Do not round intermediate calculations. Round your answers to 2 decimal...

Suppose that the S&P 500, with a beta of 1.0, has an expected return of 11%...

Suppose that the S&P 500, with a beta of 1.0, has an

expected return of 11% and T-bills provide a risk-free return of

6%.

a. What would be the expected return and beta

of portfolios constructed from these two assets with weights in the

S&P 500 of (i) 0; (ii) 0.25; (iii) 0.50; (iv) 0.75; (v) 1.0?

(Leave no cells blank - be certain to enter "0" wherever

required. Do not round intermediate calculations. Enter the value

of Expected return...

ADVERTISEMENT

ADVERTISEMENT

Latest Questions

- The output of the function is a dictionary whose keys represent the bins and whose values...

- The shape of a graph of a binomial distribution depends on the value of both n...

- In 2012, cost per Medicare beneficiary did what?

- 3. A. What techniques can a firm use to optimize demand deposit holdings? B. How do...

- The half-life of mercury-197 is 64.1 hours. If a patient undergoing a kidney scan is given...

- Double bonds react with Br2 to form a dibromide. Isobutylene undergoes cationic polymerization under conditions where...

- 1. Which sex chromosomes are limited to only one sex? A. X and Z B. X...

ADVERTISEMENT