Question

In: Finance

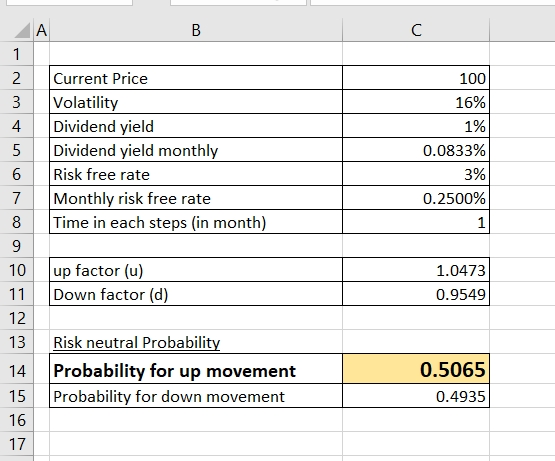

A binomial tree with one-month time steps is used to value an index option. The interest...

A binomial tree with one-month time steps is used to value an index option. The interest rate is 3% per annum and the dividend yield is 1% per annum. The volatility of the index is 16%. What is the probability of an up movement?

|

0.4704 |

||

|

0.5065 |

||

|

0.5592 |

||

|

0.5833 |

Solutions

Expert Solution

Correct answer: 0.5065

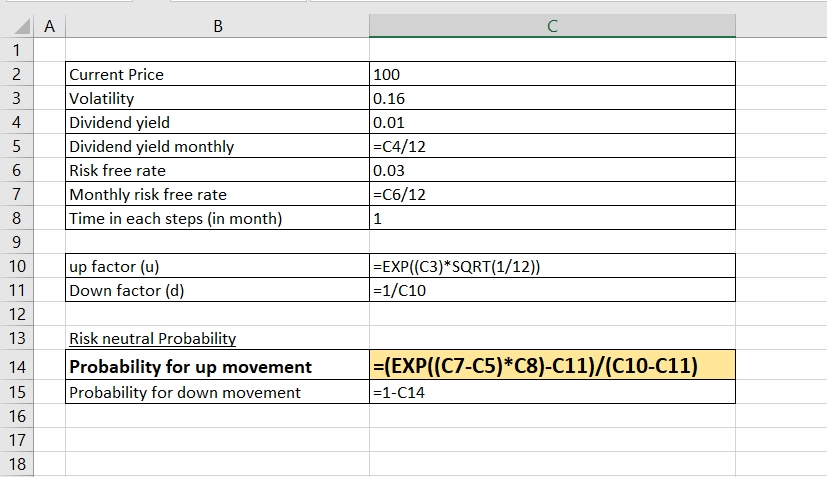

Please refer to below spreadsheet for calculation and answer. Cell reference also provided.

Cell reference -

Please note:

There are three parameters of Option Binomial Pricing Model

· up factor (u)

· down factor (d)

· probability (P)

up factor and down factor used to calculate rise in price and fall in price of underlying assets in one period. Probability is measure probability of rise in price and (1-P) is probability of price fall.

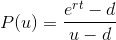

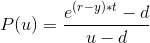

Cox-Rox-Rubinstein has suggested following formula to calculate these factors,

If dividend yield given:

where,

u = Price up factor

d = Price down factor

P = Probability

t= time in a period

=

volatility

=

volatility

y = dividend yield for time in one step

jeff jeffy answered 8 months ago

jeff jeffy answered 8 months agoRelated Solutions

You want to use the binomial tree analysis to value a 6-month call option with a...

A 2-step binomial tree is used to value an American put option with strike 104, given...

Calculate u, d and p when a binomial tree is constructed to value an option on...

(1) Please use binomial option pricing model to derive the value of a one-year put option....

1. Please use binomial option pricing model to derive the value of a one-year put option....

]Using either a Black Scholes or Binomial Tree option calculator on the internet, what is the...

Use a 2 step binomial tree to value a new exotic derivative. Draw the tree and...

Use a 2 step binomial tree to value a new exotic derivative. Draw the tree and...

Use a one step binomial option pricing model to value a 1 year at the money...

Use the binomial option pricing model to find the value of a call option on £10,000...

- a sulfide of iron, containing 36.5% S by mass, is heated in O2(g), and the products...

- Python previous function: wrtie a function that takes one argument. The function returns True if the...

- A professional couple wishes to purchase a new home costing $750,000, make a 20 percent down...

- Padre holds 100 percent of the outstanding shares of Sonora. On January 1, 2016, Padre transferred...

- Question: Use backtracking algorithm design to write Java code to solve the subset problem: given a...

- Patsy Ltd. produces ice-cream and would like to accurately forecast sales so that it can meet...

- Power Music owns five music stores, where it sells music, instruments, and supplies. In addition, it...