Question

In: Finance

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

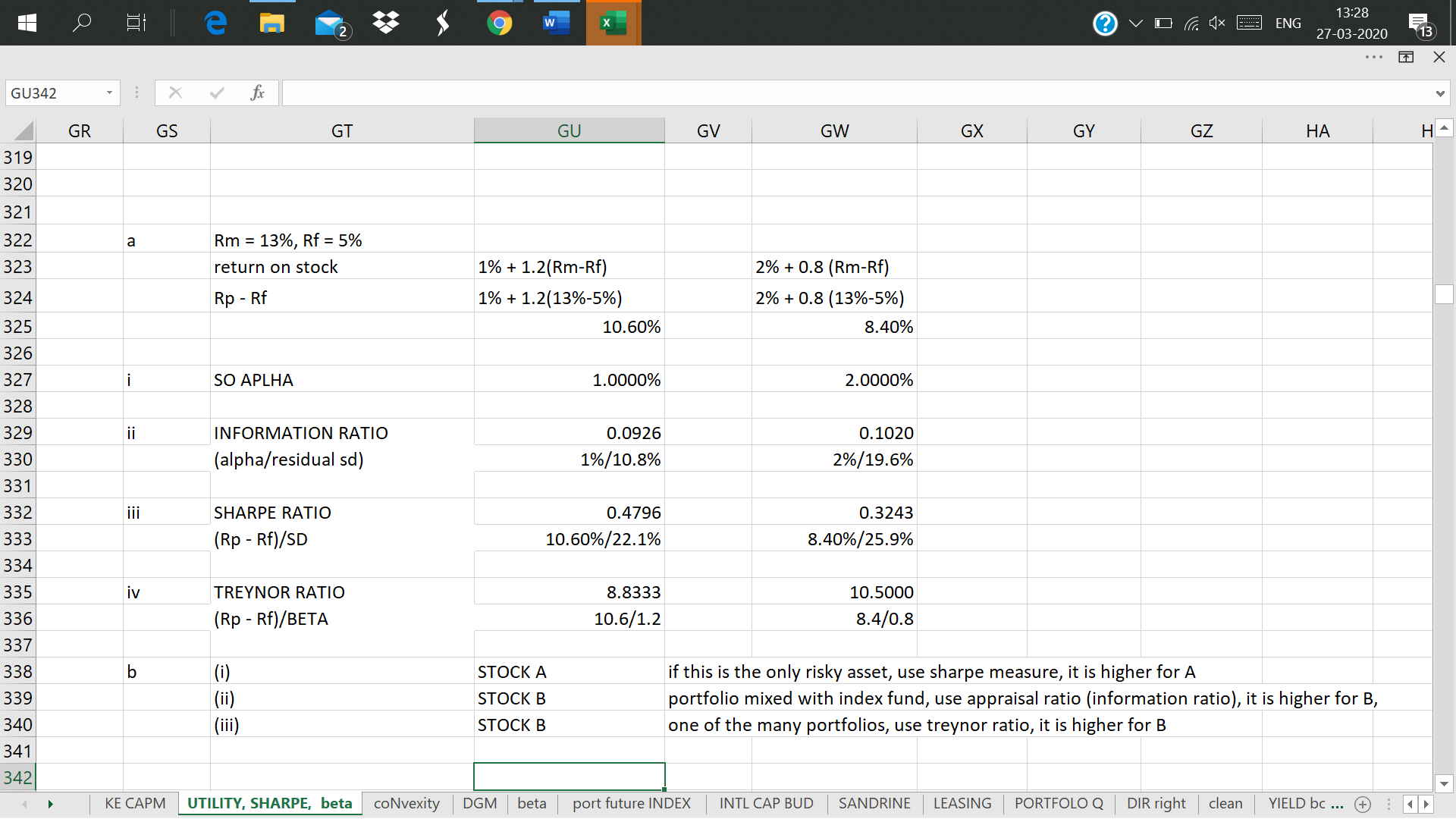

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 5%, and the market’s average return was 13%. Performance is measured using an index model regression on excess returns. Stock A Stock B Index model regression estimates 1% + 1.2(rM − rf) 2% + 0.8(rM − rf) R-square 0.605 0.451 Residual standard deviation, σ(e) 10.8% 19.6% Standard deviation of excess returns 22.1% 25.9% a. Calculate the following statistics for each stock: (Round your answers to 4 decimal places.) b. Which stock is the best choice under the following circumstances?

Solutions

Expert Solution

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP PLEASE

jeff jeffy answered 9 months ago

jeff jeffy answered 9 months agoRelated Solutions

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 8%, and the market’s average return was 14%. Performance

is measured using an index model regression on excess returns.

Stock A

Stock B

Index model regression estimates

1% + 1.2(rM − rf)

2% + 0.8(rM − rf)

R-square

0.665

0.481

Residual standard deviation, σ(e)

11.8%

20.6%

Standard deviation of excess returns

23.1%

27.9%

a. Calculate the following statistics for each...

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 7%, and the market’s average return was 14%. Performance

is measured using an index model regression on excess returns.

Stock

A

Stock

B

Index model

regression estimates

1% +

1.2(rM − rf)

2% +

0.8(rM − rf)

R-square

0.635

0.466

Residual

standard deviation, σ(e)

11.3%

20.1%

Standard

deviation of excess returns

22.6%

26.9%

a. Calculate the following statistics for each...

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 7%, and the market’s average return was 15%. Performance

is measured using an index model regression on excess returns.

Stock A

Stock B

Index model regression estimates

1% + 1.2(rM − rf)

2% + 0.8(rM − rf)

R-square

0.641

0.469

Residual standard deviation, σ(e)

11.4%

20.2%

Standard deviation of excess returns

22.7%

27.1%

a. Calculate the following statistics for each...

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 6%, and the market’s average return was 15%. Performance

is measured using an index model regression on excess returns.

Stock A

Stock B

Index model regression estimates

1% + 1.2(rM − rf)

2% + 0.8(rM − rf)

R-square

0.594

0.445

Residual standard deviation, σ(e)

10.6%

19.4%

Standard deviation of excess returns

21.9%

25.5%

a. Calculate the following statistics for each...

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 5%, and the market’s average return was 14%. Performance

is measured using an index model regression on excess returns.

Stock A

Stock B

Index model regression estimates

1% + 1.2(rM − rf)

2% + 0.8(rM − rf)

R-square

0.611

0.454

Residual standard deviation, σ(e)

10.9%

19.7%

Standard deviation of excess returns

22.2%

26.1%

a. Calculate the following statistics for each...

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 4%, and the market’s average return was 12%. Performance

is measured using an index model regression on excess returns.

Stock

A

Stock

B

Index model

regression estimates

1% +

1.2(rM − rf)

2% +

0.8(rM − rf)

R-square

0.689

0.493

Residual

standard deviation, σ(e)

12.2%

21%

Standard

deviation of excess returns

23.5%

28.7%

a. Calculate the following statistics for each...

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate...

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 8%, and the market’s average return was 12%. Performance

is measured using an index model regression on excess returns.

Stock A

Stock B

Index model regression estimates

1% + 1.2(rM − rf)

2% + 0.8(rM − rf)

R-square

0.653

0.475

Residual standard deviation, σ(e)

11.6%

20.4%

Standard deviation of excess returns

22.9%

27.5%

a. Calculate the following statistics for each...

Problem 24-9 Consider the two (excess return) index-model regression results for stocks A and B. The...

Problem 24-9

Consider the two (excess return) index-model regression results

for stocks A and B. The risk-free rate over the

period was 5%, and the market’s average return was 15%. Performance

is measured using an index model regression on excess returns.

Stock

A

Stock

B

Index model regression

estimates

1% +

1.2(rM ? rf)

2% +

0.8(rM ? rf)

R-square

0.617

0.457

Residual standard deviation,

?(e)

11%

19.8%

Standard deviation of excess

returns

22.3%

26.3%

a. Calculate the following statistics...

Consider the two (excess return) index model regression results for A and B: RA = –1.8%...

Consider the two (excess return) index model regression results

for A and B:

RA = –1.8% + 2RM

R-square = 0.640

Residual standard deviation = 12.6%

RB = 1.4% + 1RM

R-square = 0.590

Residual standard deviation = 11.4%

If rf were constant at 6% and the regression

had been run using total rather than excess returns, what would

have been the regression intercept for stock A?

(Negative value should be indicated by a minus sign. Round

your answer to...

Consider the two (excess return) index model regression results for stock A and B RA =...

Consider the two (excess return) index model regression results

for stock A and B RA = 0.01 + 1.2RM R2 of 0.576; Std deviation of

error term of 10.3% RB = -0.02 + 0.8RM R2 of 0.436; Std deviation

of error term of 9.1%

a) Which stock has more firm-specific risk? Explain [4

points]

b) Which has greater market risk? Explain [4 points]

c) For which stock does market movement explain a grater

fraction of return variability? Explain [4 points]...

ADVERTISEMENT

ADVERTISEMENT

Latest Questions

- Based on what you learned in this module, identify one person who you believe possesses primarily...

- An Auditor may decide to make use of a specialist in obtaining sufficient appropriate audit evidence...

- Dirac's Theorem states that "A simple graph with n vertices (n >= 3) is Hamiltonian if...

- Two 10-cm-diameter charged rings face each other, 15cm apart. The left ring is charged to -29nC...

- Under what conditions would it be possible for an excise tax to have no efficiency cost...

- explain the difference between activities and financial statements of service businesses and merchandising businesses.

- 2. Compare and compare the matrix multiplication algorithm and the Floyd-Warshall algorithm to find all pairs...

ADVERTISEMENT