Question

In: Economics

3. Determine the effect upon equilibrium price and quantity sold if the following changes occur in...

3. Determine the effect upon equilibrium price and quantity sold if the following changes occur in a particular market:

a. Consumers’ income increases and the good is normal.

b. The price of a substitute good (in consumption) increases.

c. The price of a substitute good (in production) increases

d. The price of a complement good (in consumption) increases

e. The price of inputs used to produce the good increases.

f. Consumers expect that the price of the good will increase in the near future.

g. It is widely publicized that consumption of the good is hazardous to health.

h. Cost reducing technological change takes place in the industry.

For each of the pair of events indicated below, perform qualitative analysis to predict the direction of change in either the equilibrium price or equilibrium quantity. Explain why the change is indeterminate.

a. Both a and h conditions occur simultaneously.

b. Both d and e conditions occur simultaneously.

c. Both d and h conditions occur simultaneously.

d. Both f and c conditions occur simultaneously.

Solutions

Expert Solution

Ans) a) Normal good is a good whose consumption increase with increase in income. Demand will increase, demand curve will shift to the right. Both price and quantity will increase.

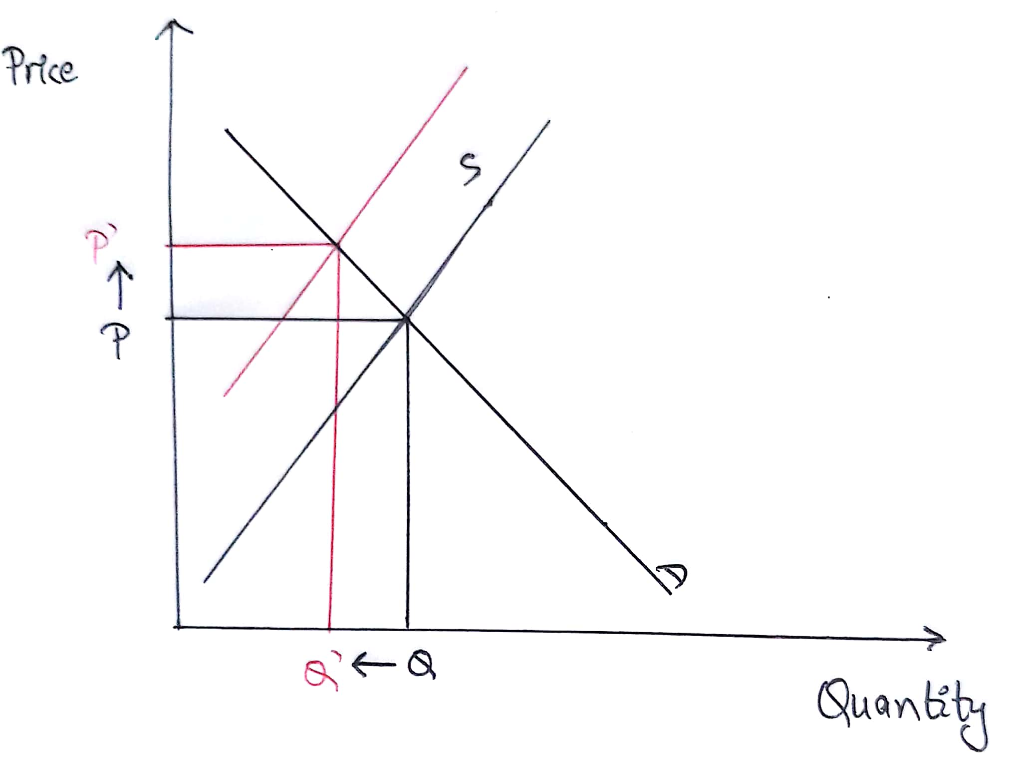

b) When the price of substitute good increases, demand for the product in question will increase as consumer prefer buying cheaper alternative. Demand curve will shift to the right. Both price and quantity will increase.

c) When the price of substitute good in production increases, supply of product in question decreases as producer find substitute good to be more profitable. Supply curve will shift to the left. Quantity will decrease, price will increase.

d) When price of complement good increases, demand for product in question decreases. Demand curve will shift to the left. Both price and quantity will decrease.

e) When price of input increases, supply decreases because producing good becomes costly. Supply curve will shift to the left. Price will increase and quantity will decrease.

f) When consumer expect the price of good to increase in future, they will start buying it more in present. Demand curve will shift to the right. Both price and quantity will increase.

g) When negative rumours are spread,product becomes less desirable. Demand will decrease, demand curve will shift to the left. Both price and quantity will decrease.

h) When cost reducing technology comes, producing goods becomes cheaper and supply increases. Supply curve will shift to the right. Price will decrease and quantity will increase.

--------------------------------------------------------------------------

Question 2)

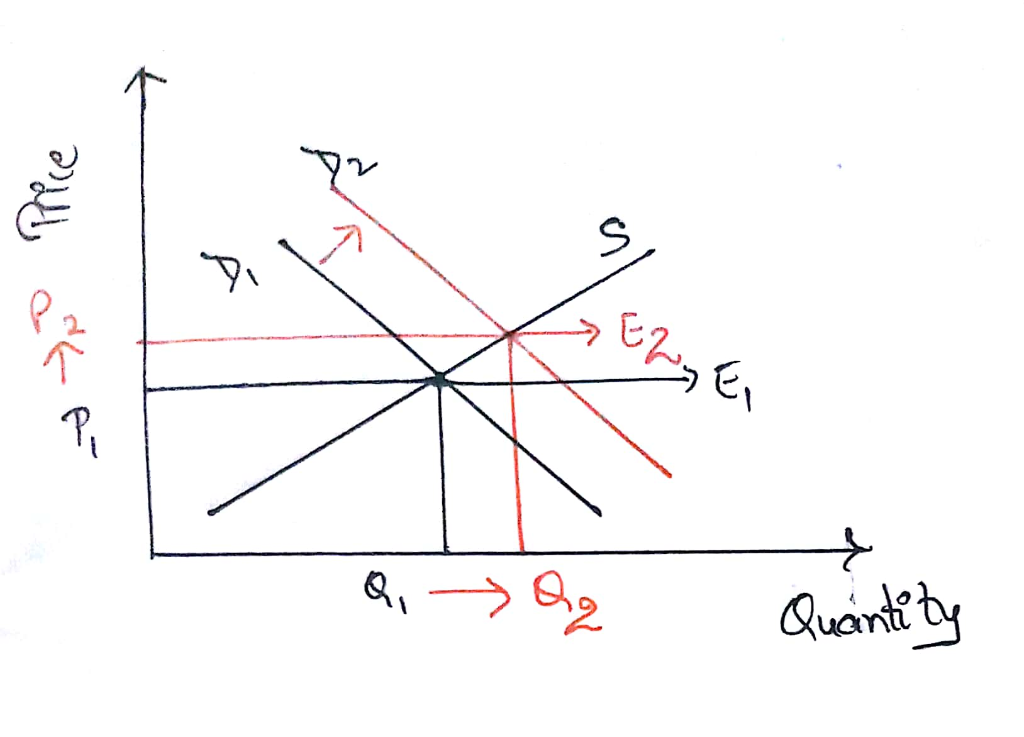

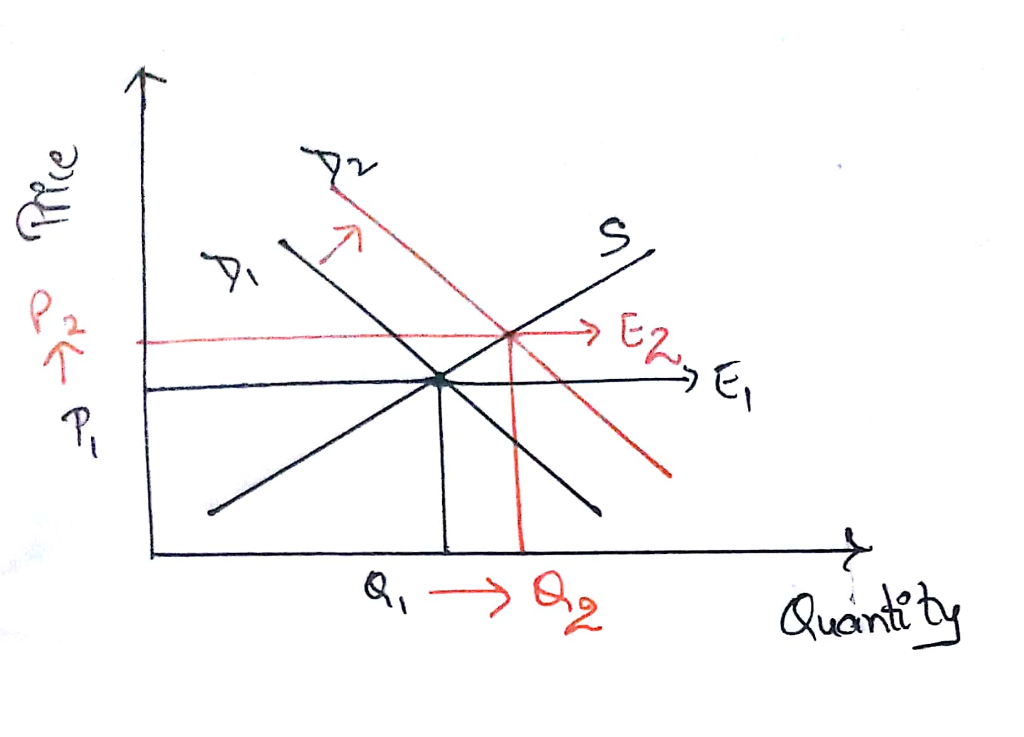

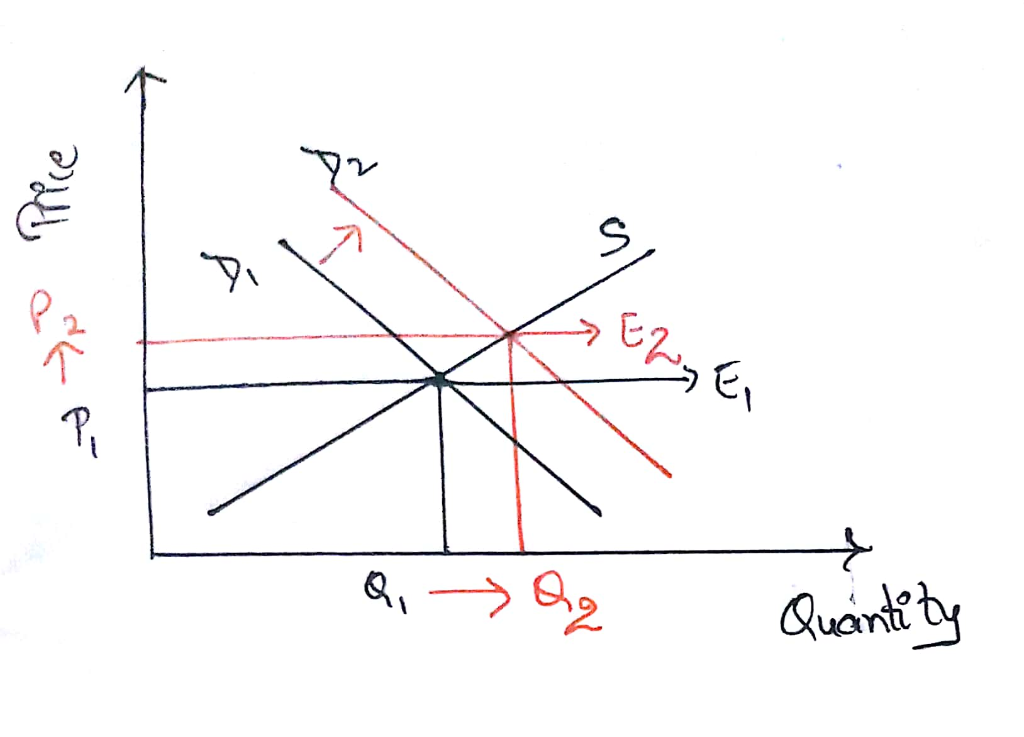

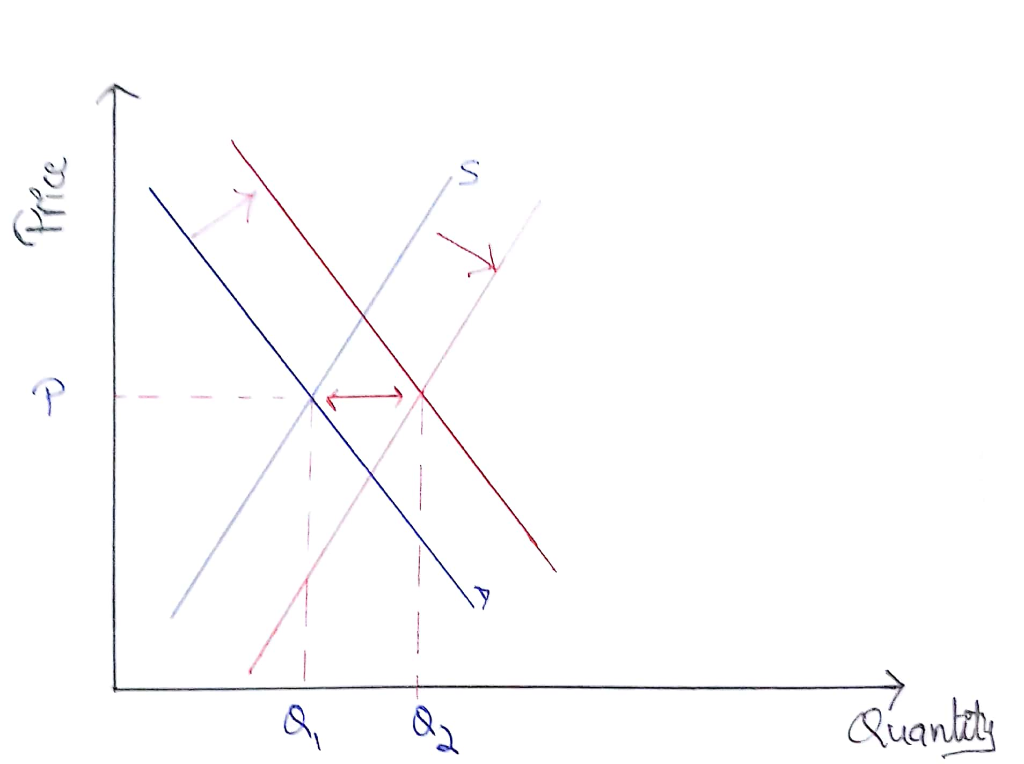

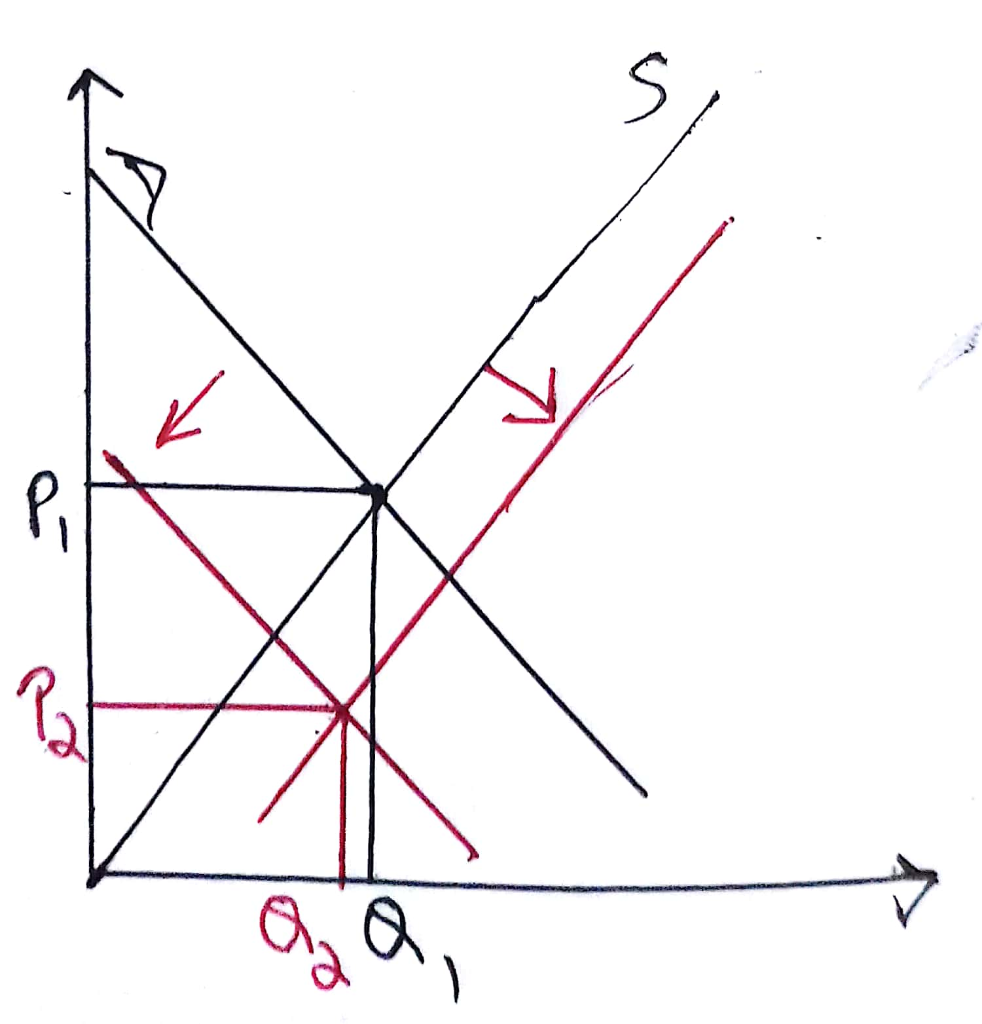

A) Increase in supply and increase in demand. Quantity increases and price is indeterminate because three cases are possible.

When increase in demand = increase in supply

When increase in demand >increasincn supply

Increase in demand < increase in supply

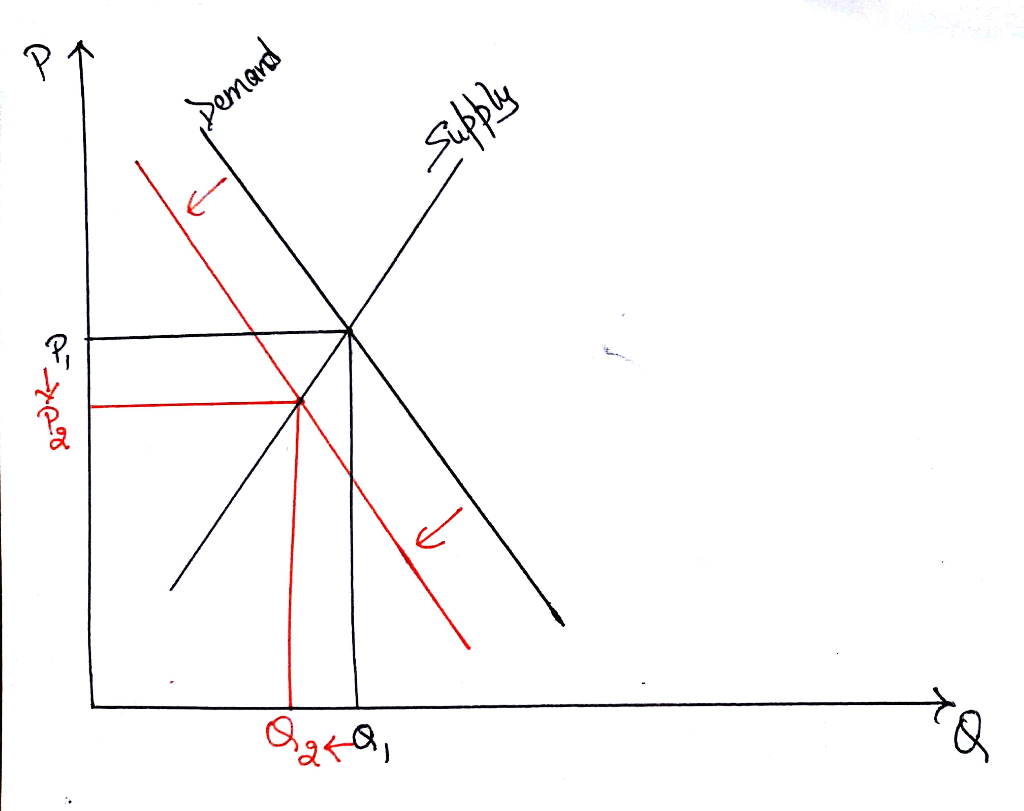

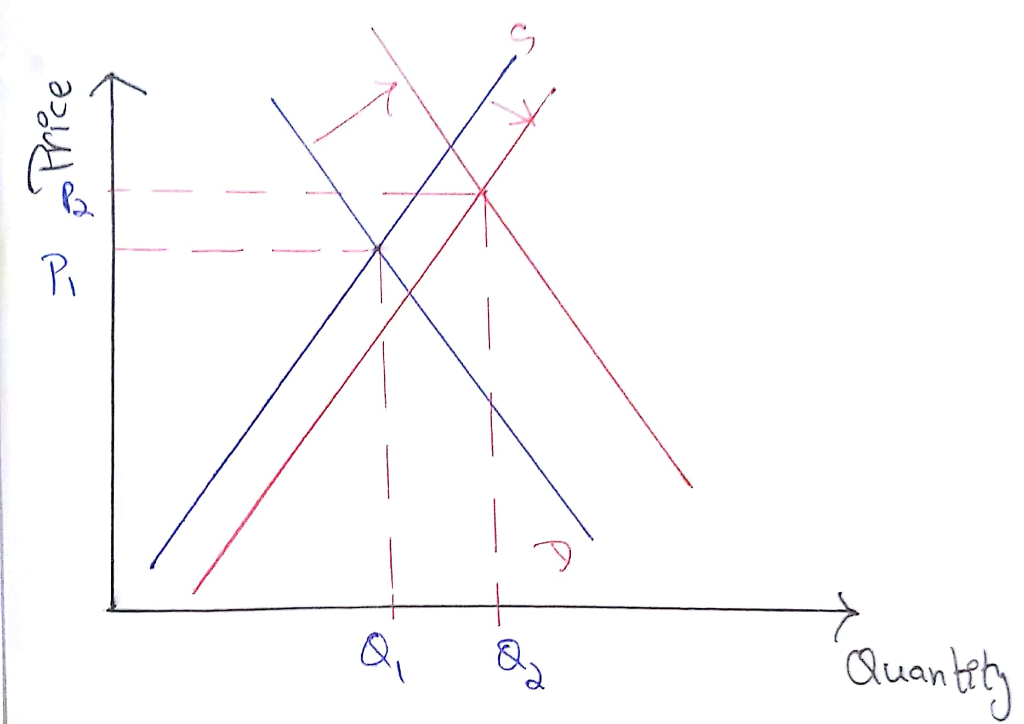

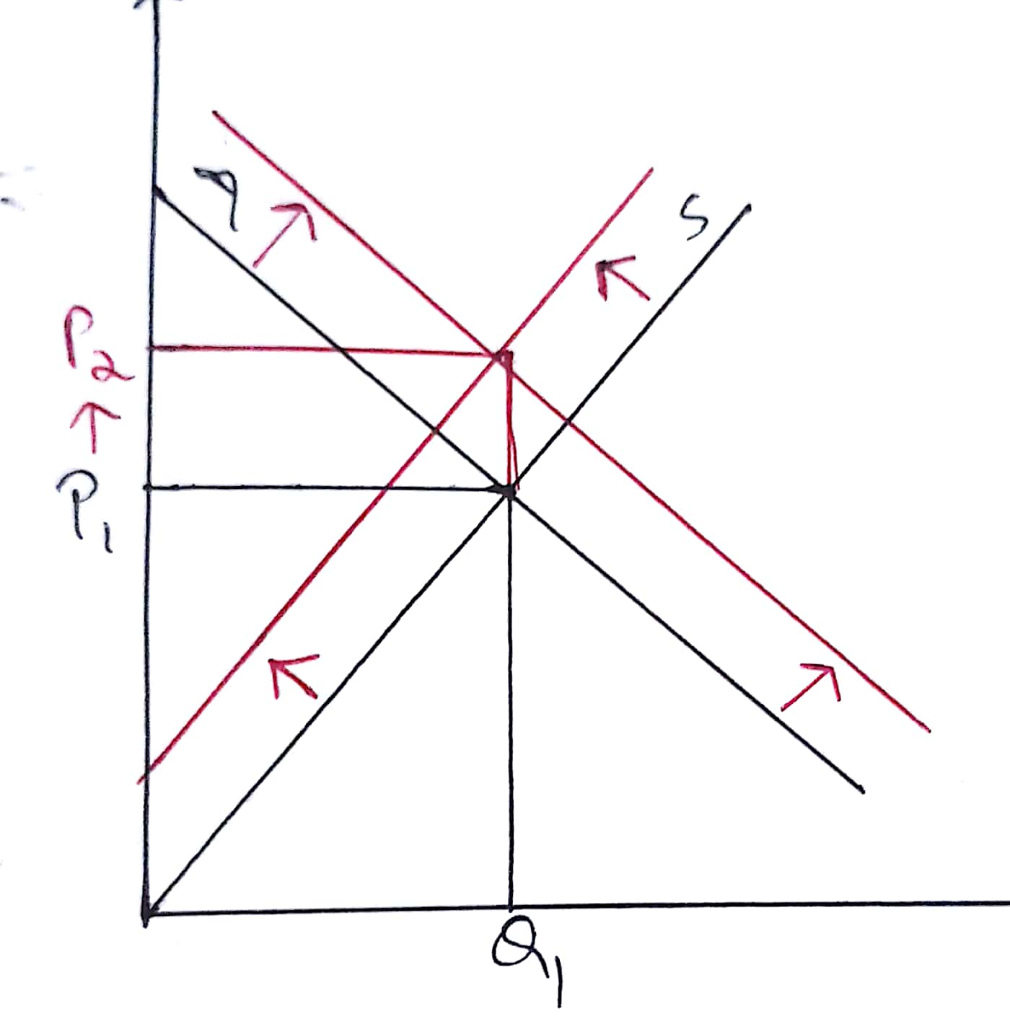

B) Decrease in demand and decrease in supply. Quantity decreases and price is indeterminate because three cases are possible÷

Decrease in demand = decrease in supply

Decrease in demand > decrease in supply

Decrease in demand < decrease in supply

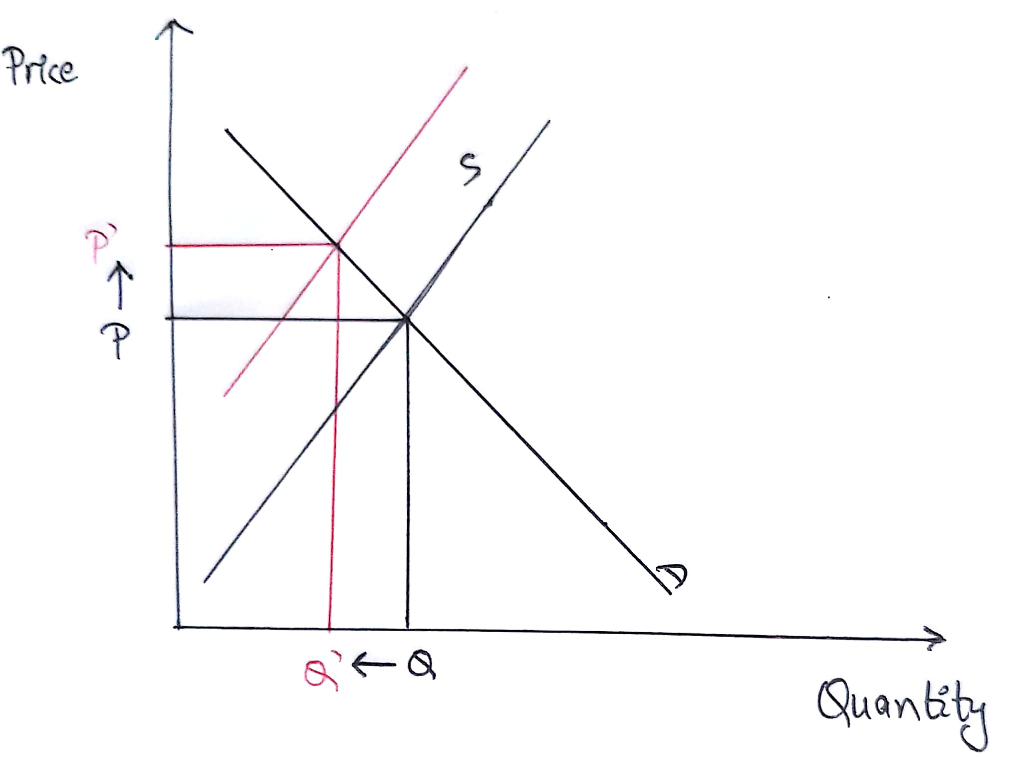

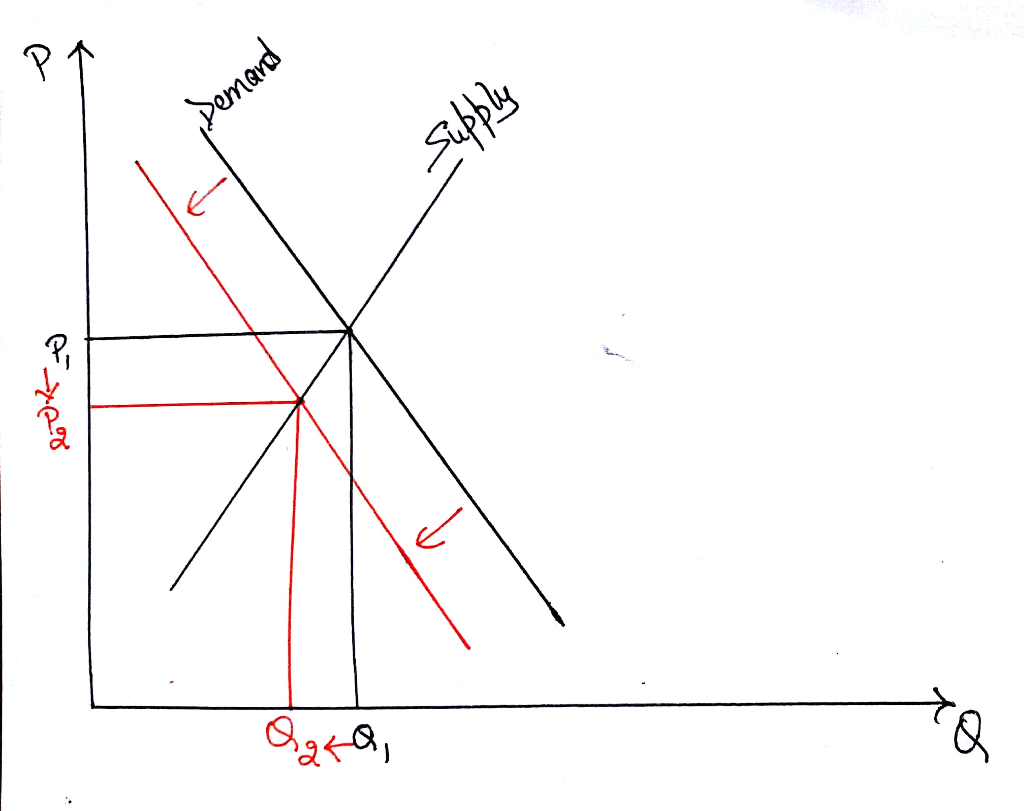

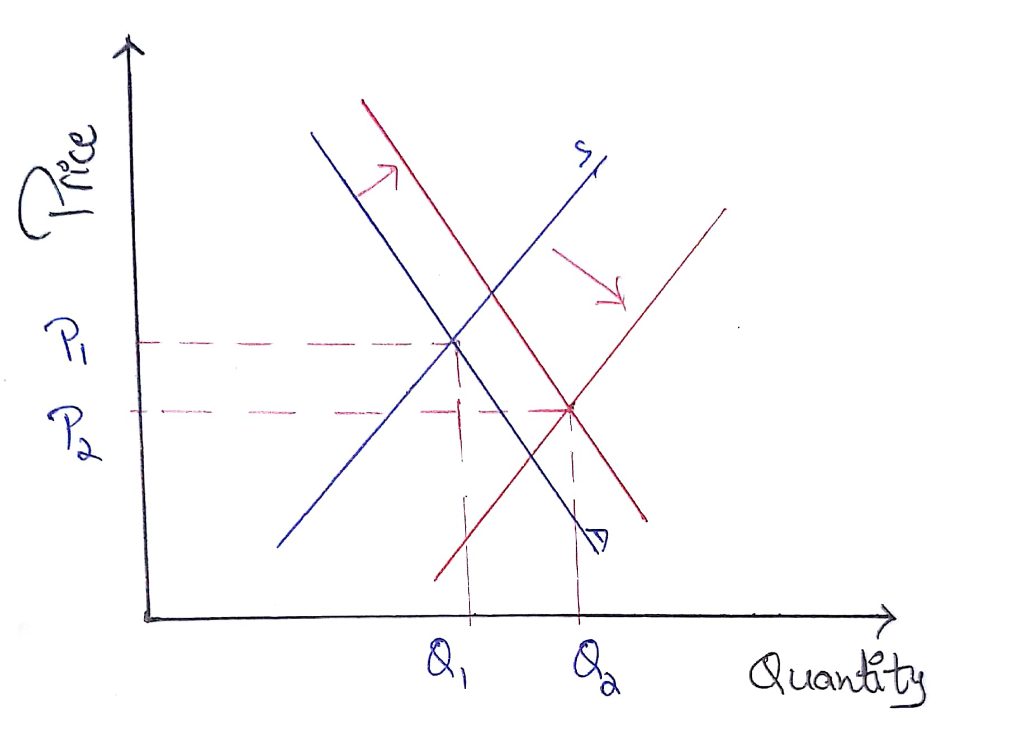

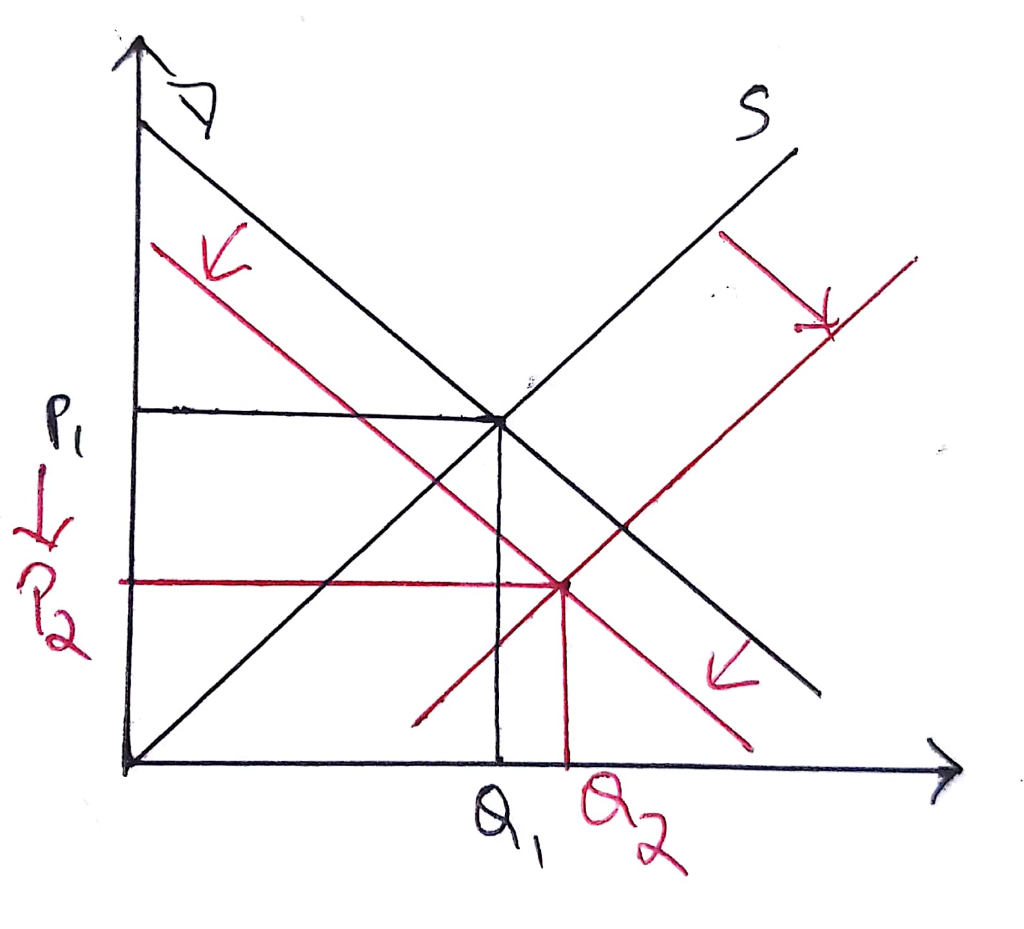

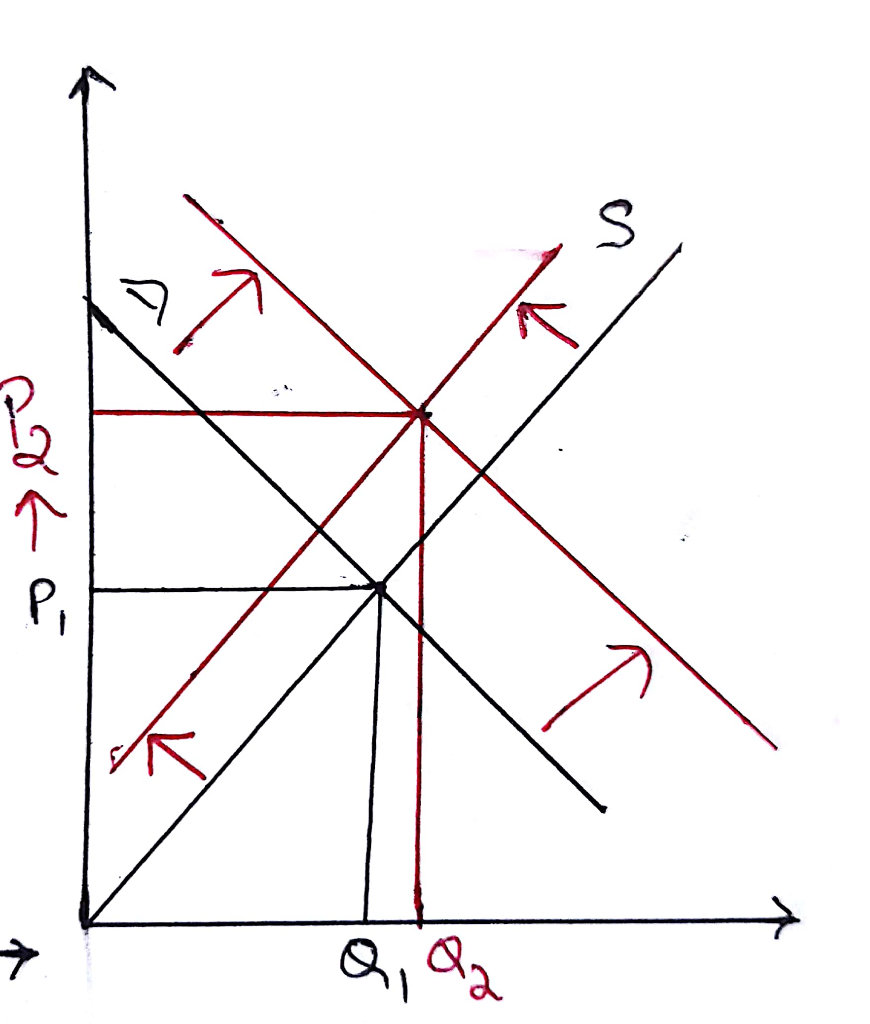

C) Increase in supply and decrease in demand. Price will fall and quantity is indeterminate. It is because three cases are possible ÷

Decrease in demand = increase in supply

Decrease in demand < increase in supply

Decrease in demand > increase in supply

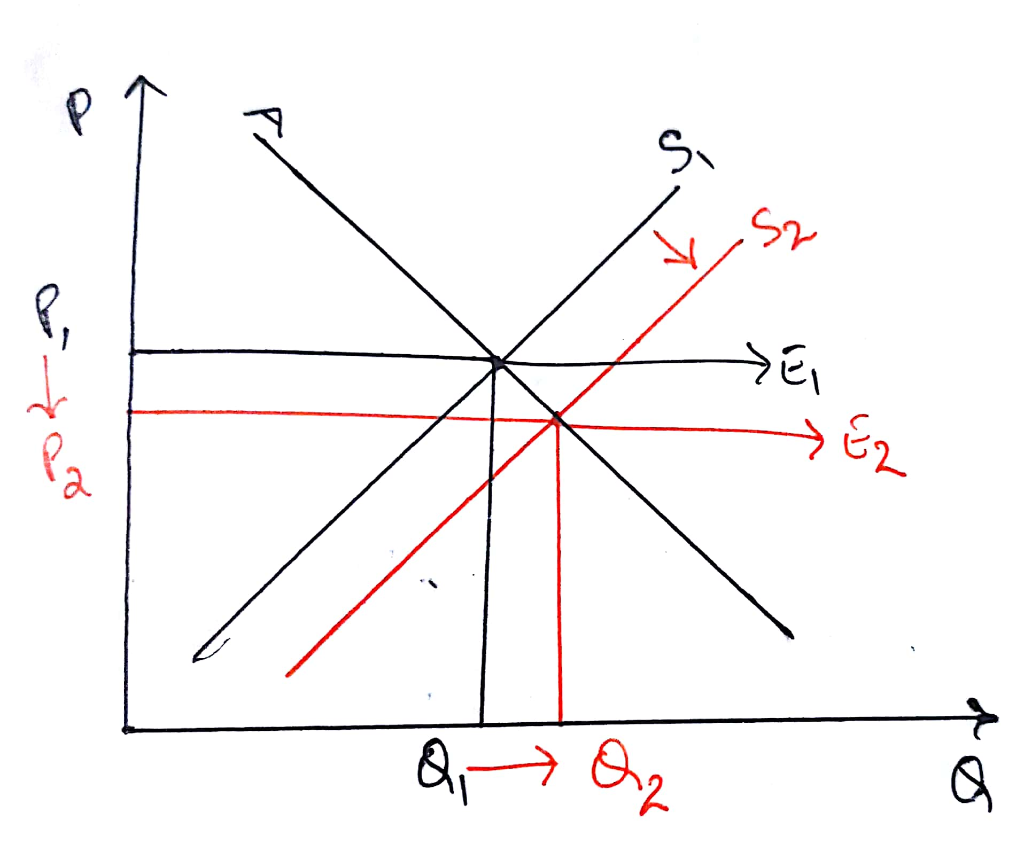

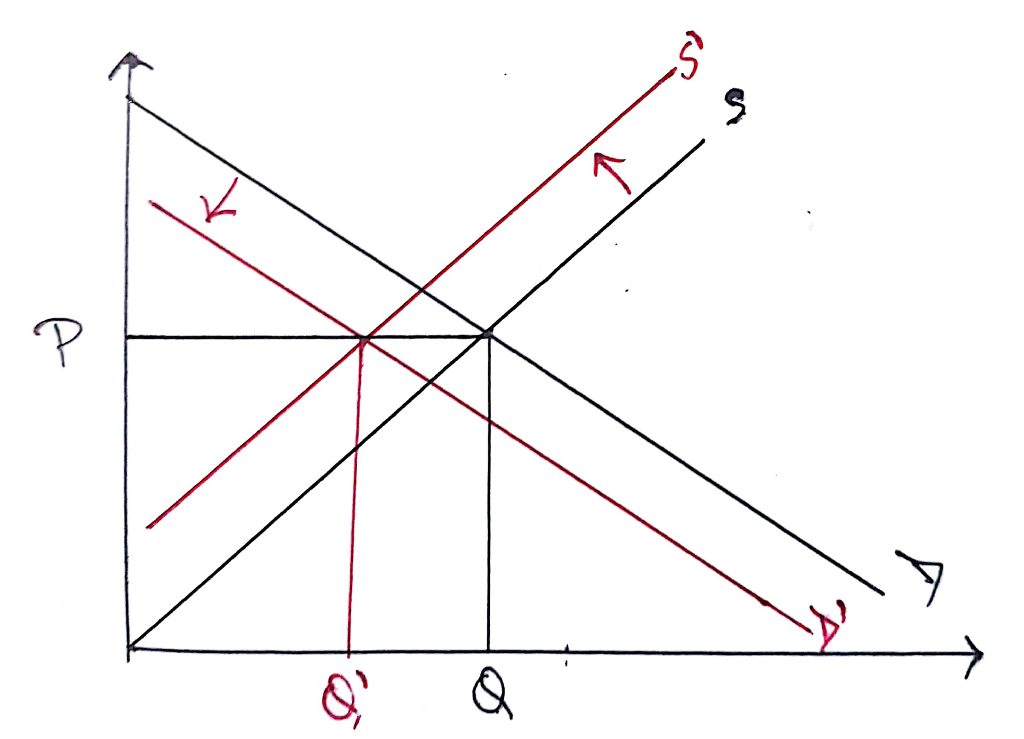

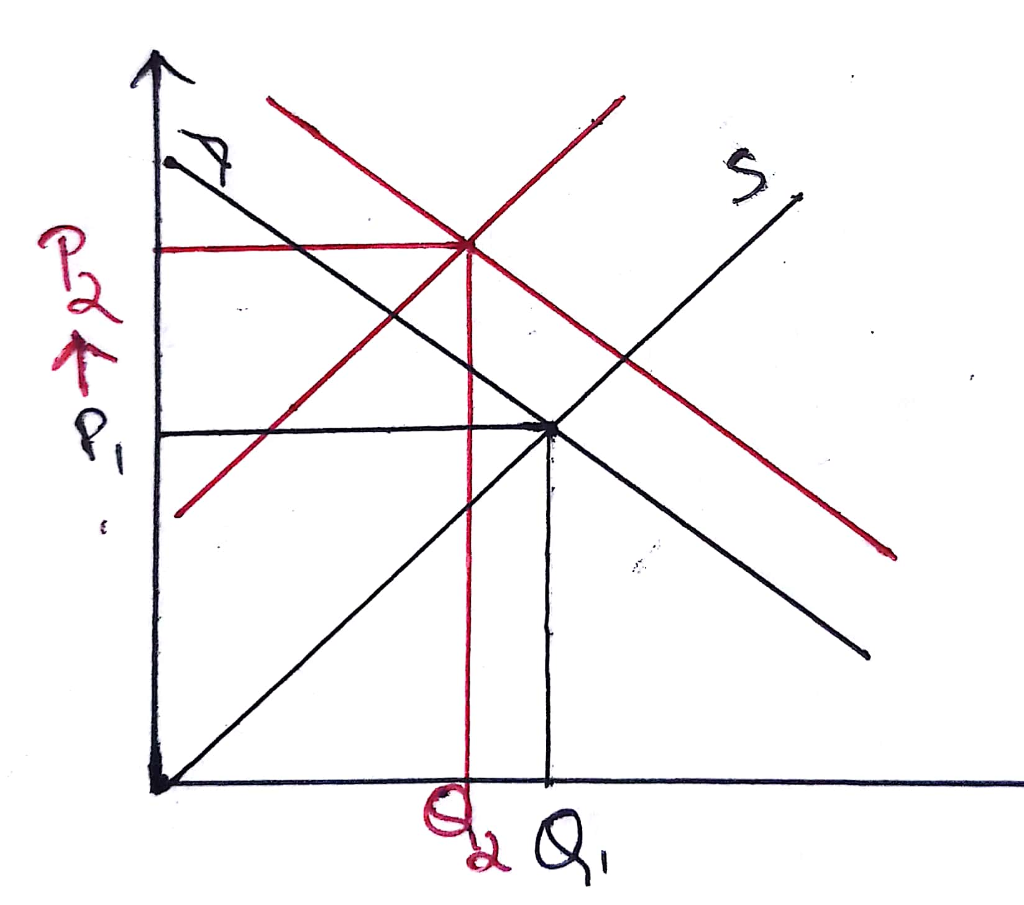

D) Increase in demand and decrease in supply. Price will increase and quantity is indeterminate. Because three cases are possible.

Increase in demand = decrease in supply

Increase in demand > decrease in supply

Increase in demand < decrease in supply

Rahul Sunny answered 2 weeks ago

Rahul Sunny answered 2 weeks agoRelated Solutions

The equilibrium price for a product is $58, and the quantity sold of the product is...

The equilibrium price for a product is $32, and the quantity sold of the product is...

Draw a graph to show the effect on the equilibrium price and quantity of hamburgers if...

Identify what determinant changes and explain how the equilibrium price and equilibrium quantity in a purely...

The equilibrium price in this market is _______ per shirt, and the equilibrium quantity is _______ shirts bought and sold per month.

Using the market model, show graphically the effect on the equilibrium price and quantity of good...

Explain Market equilibrium, equilibrium price, and equilibrium quantity

9. Find the equations for Demand and Supply, and determine the market equilibrium price and quantity....

Consider the following hypothetical market. The equilibrium price is $10 and the equilibrium quantity is 20...

. Given the changes stated, predict new market equilibrium price and quantity demanded. For each question...

- 16. When demand decreases in a competitive market, a. Supply rises. b. Actual price rises. c....

- Draw a picture that shows FA oxidation vs. FA synthesis Color-code each pathway Include: All steps...

- In IRAC Form Clifford Aymes was hired by Jonathan Bonelli of Sun Island Sales, Inc., to...

- 1.Describe the log-linear regression model and how it is used to measure the elasticity of the...

- I need to create an exception handler with the following code I have below public class...

- Why is Tukey's method more powerful than Bonferroni's method?

- Why did the course of World War I turn out to be so different from what...