Question

In: Finance

On Monday morning, your buy one CME British Pound futures contract (i.e., you buy BP) containing...

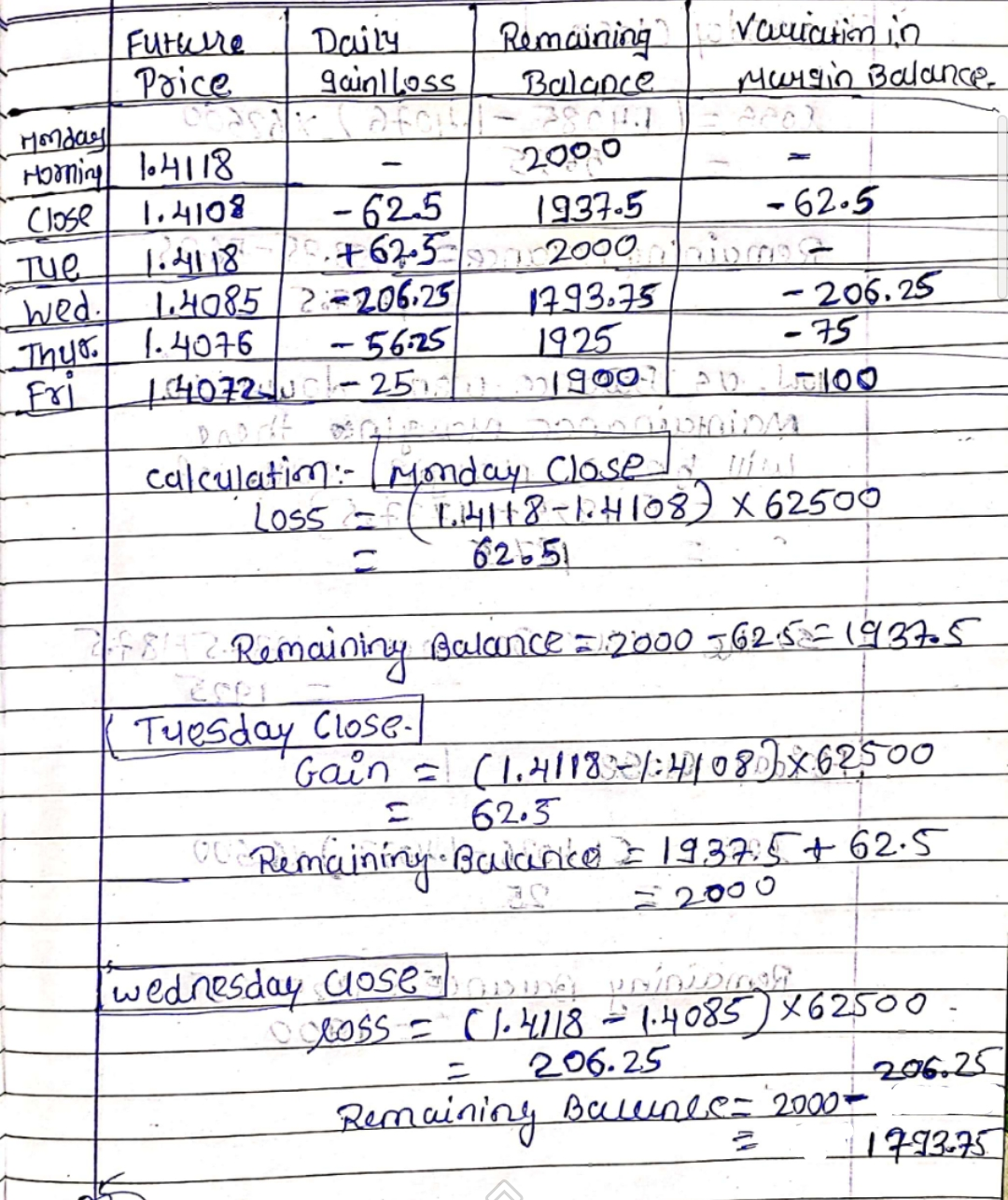

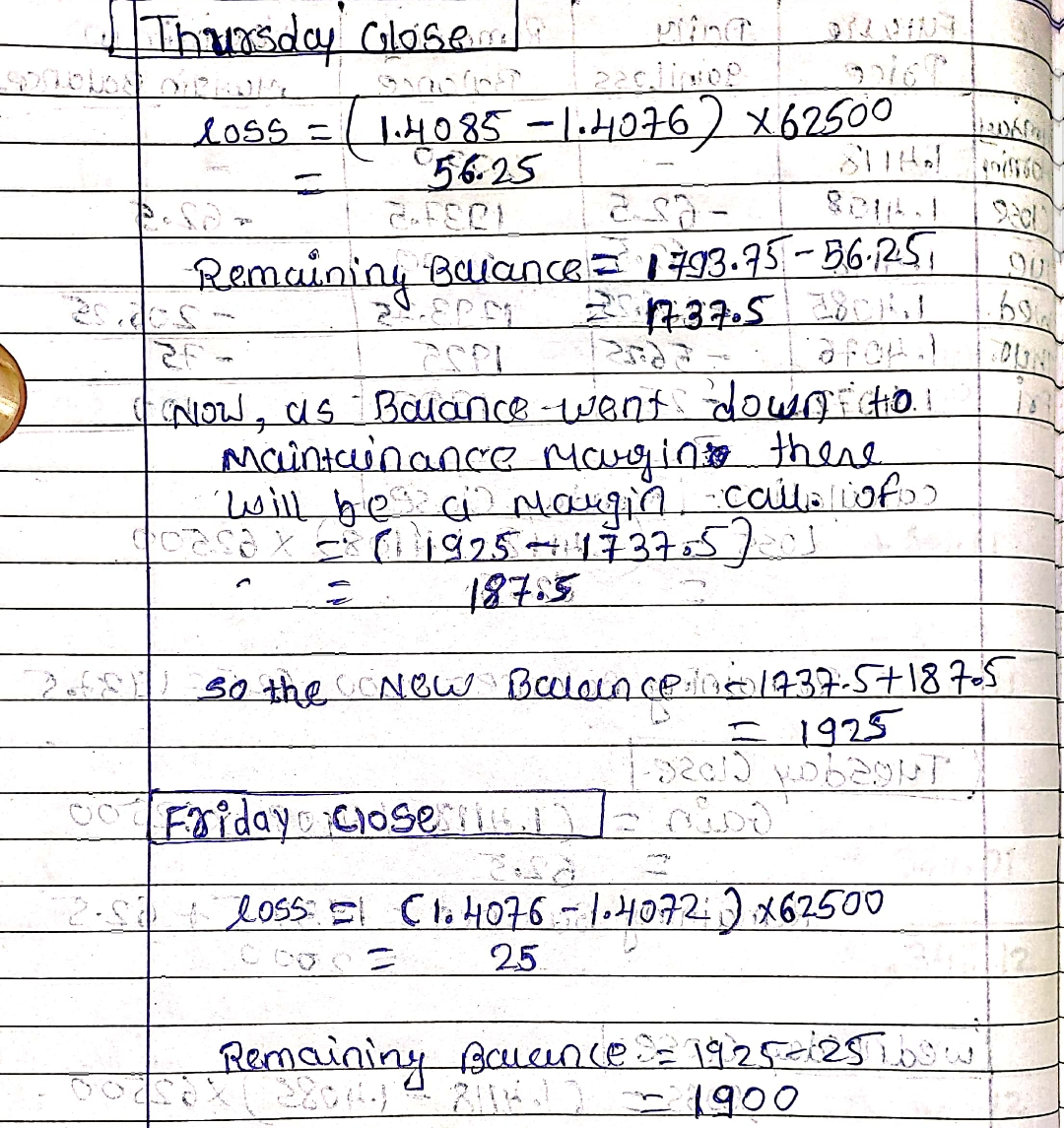

On Monday morning, your buy one CME British Pound futures contract (i.e., you buy BP) containing BP 62,500 at a price of $1.4118. Suppose the broker requires an initial margin of $1,925 and a maintenance margin of $1,750. The settlement prices for Monday through Friday are $1.4108, $1.4118, $1.4085, $1.4076, and $1.4072, respectively. Assume that you begin with an initial balance of $2,000 (not $1,925). Fill out the following tables. Make sure you show your calculation. (To get exact answers, show 4 digits after the decimal point. If your calculation can’t show 4 digits after the decimal point, use excel spread sheet for the calculation) (9 points)

|

|

Monday Morning |

Monday Close |

Tuesday Close |

Wednesday Close |

Thursday Close |

Friday Close |

|

Future price |

$1.4118 |

$1.4108 |

$1.4118 |

$1.4085 |

$1.4076 |

$1.4072 |

|

Daily gain/Loss |

||||||

|

Remaining Balance |

||||||

|

Variation Margin |

||||||

|

Balance |

Solutions

jeff jeffy answered 7 months ago

jeff jeffy answered 7 months agoRelated Solutions

On Monday morning you sell one June T-bond futures contract at 97:27, that is, for $97,843.75....

On Monday morning you sell one June T-bond futures contract at $98,622.75. The contract's face value...

1) You are US company, 500,000 BP (British Pound) payable to UK in one year. Answer...

Today's settlement price on a Chicago Mercantile Exchange (CME) € futures contract is $1.7537/€. Your initial...

Yesterday, you entered into a futures contract to buy €62,500 at $1.50 per €. Your initial...

A corn futures contract is 5,000 bushels. If you buy a contract of corn at 356...

You have a short position in one corn futures contract. Each futures contract calls for the...

Suppose you sold a pound futures contract three days ago at$1.33/£. Over the next three...

You enter into a futures contract to buy white maize for R1 845 per tonne. The...

1. Suppose you buy a call option on a $100,000 Treasury bond futures contract with an...

- Students performed a procedure similar to Part III of this experiment (Analyzing a Vitamin Supplement for...

- The output of the function is a dictionary whose keys represent the bins and whose values...

- The shape of a graph of a binomial distribution depends on the value of both n...

- In 2012, cost per Medicare beneficiary did what?

- 3. A. What techniques can a firm use to optimize demand deposit holdings? B. How do...

- The half-life of mercury-197 is 64.1 hours. If a patient undergoing a kidney scan is given...

- Double bonds react with Br2 to form a dibromide. Isobutylene undergoes cationic polymerization under conditions where...