Question

In: Economics

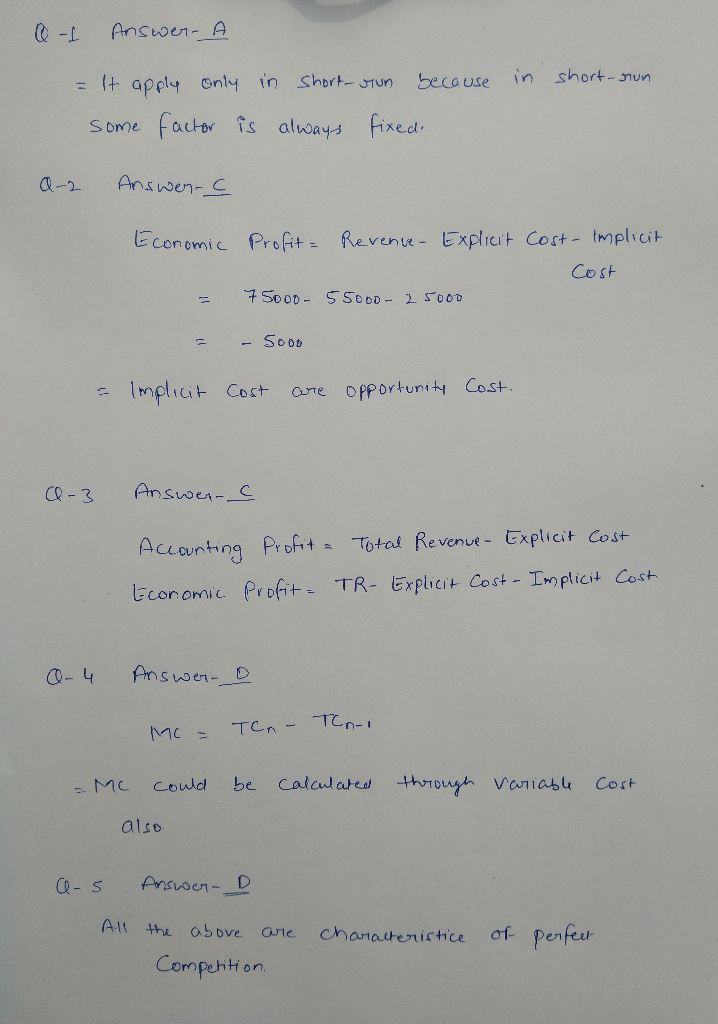

QUESTION 1 The law of diminishing marginal productivity pertains to_____: a. the short run. b. the...

QUESTION 1

-

The law of diminishing marginal productivity pertains to_____:

a. the short run.

b. the long run.

c. both the short run and the long run.

d. the short run for small firms, and the long run for large firms.

1 points

QUESTION 2

-

Assume that you own a sole proprietorship. Your first year earnings were $75,000, and your explicit costs were $55,000. If you could have worked at another establishment and earned $25,000, which of the following is true?

a. Your firm earned an economic profit of $20,000.

b. Your firm's total implicit costs were $80,000.

c. Your firm sustained an economic loss of $5,000.

d. Your firm's total costs are $100,000.

1 points

QUESTION 3

-

Which of the following is true regarding accounting profit?

a. It is typically smaller than economic profit.

b. It includes all explicit and implicit cost of production.

c. It includes depreciation.

d. All of the above.

1 points

QUESTION 4

-

Marginal cost is understood as the change in__________ when producing one more unit of output. In the short run, marginal cost can also be determined by the change in__________ when producing one more unit of output.

a. variable cost; fixed cost

b. total cost; fixed cost

c. fixed cost; variable cost

d. total cost; variable cost

1 points

QUESTION 5

-

Which of the following are characteristics of a perfectly competitive market?

a. Firms are price takers.

b. Firms produce identical or nearly identical products.

c. Firms can enter the market without any restrictions.

d. All of the above.

1 points

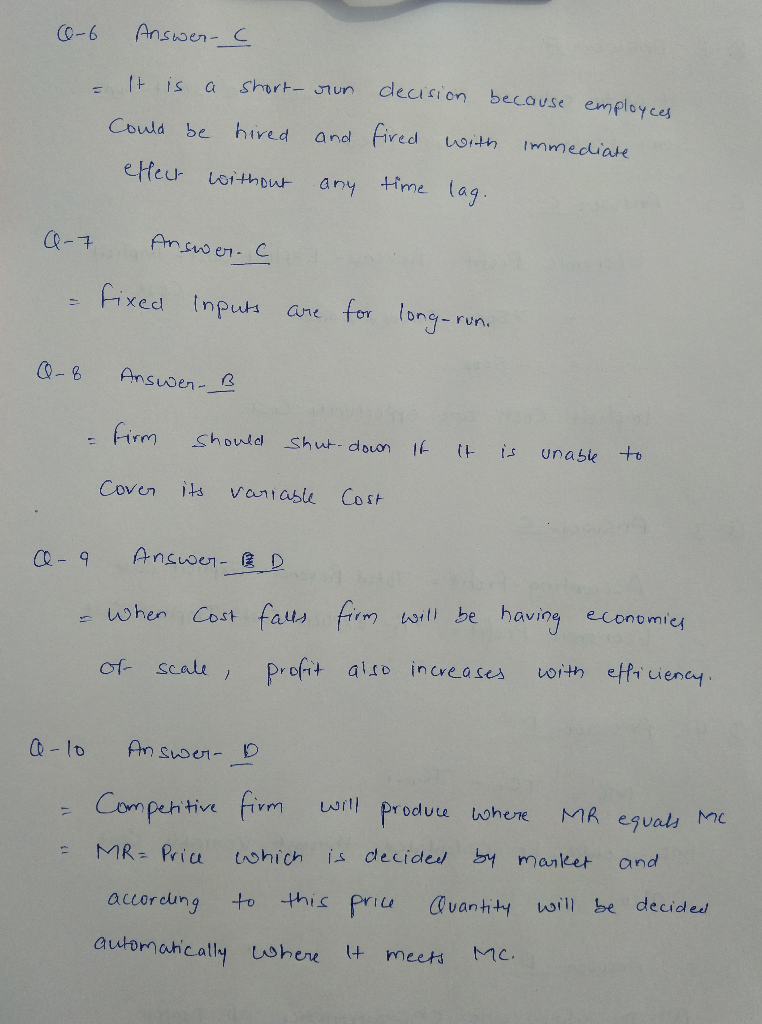

QUESTION 6

-

An organization with 50 employees will add 10 employees next month. This is_____:

a. a long run decision.

b. a long run and a short run decision.

c. a short run decision.

d. none of the above.

1 points

QUESTION 7

-

Fixed inputs are_____:

a. those inputs to production that have a fixed price.

b. those inputs to production that result in a fixed variable product.

c. those inputs to production that cannot be varied in the short run.

d. those inputs to production that have a fixed market.

1 points

QUESTION 8

-

When deciding whether to continue operations or shutdown, a perfectly competitive firm should_____:

a. continue operations if the price of the firm's product falls below the minimum average variable cost.

b. shut down if the price of the firm's product falls below the minimum average variable cost.

c. continue operations if the marginal cost of a new invention for the firm surpasses average variable cost.

d. shut down if it can cover all of its costs, but only at a diminishing marginal rate.

1 points

QUESTION 9

-

If the total output rises while the cost per unit fails, a firm is understood to be enjoying_____:

a. increased profits.

b. economies of scale.

c. maximum efficiency.

d. all of the above.

1 points

QUESTION 10

-

Firms that compete in perfectly competitive markets must decide_____:

a. the quantity to produce.

b. the price to charge.

c. the price to charge and the quantity to produce.

d. none of the above.

Solutions

#Please rate

positively...thank you

#Please rate

positively...thank you Rahul Sunny answered 8 months ago

Rahul Sunny answered 8 months agoRelated Solutions

What’s the law of diminishing marginal productivity? What are the costs in the short run? What...

What is the law of diminishing marginal productivity? How does the law of diminishing marginal productivity...

Q2. What is the law of diminishing marginal productivity? How does the law of diminishing marginal...

explain the law of diminishing marginal productivity and why the law tends to hold in the...

Microeconomics Marginal Productivity and the Law of Diminishing Marginal Returns You have recently been hired to...

Explain the principle of the cost of production, Diminishing Marginal Productivity , Diminishing Marginal Utility in...

Explain the law of diminishing marginal utility & the law of diminishing return.

a) explain what the law of diminishing(marginal) return means. Does it apply to the short or...

How do specialization economies and diminishing marginal returns affect the shape of a firm’s short-run marginal...

Question 1: Do young children follow the law of diminishing marginal utility? Question 2: Suppose a...

- The output of the function is a dictionary whose keys represent the bins and whose values...

- The shape of a graph of a binomial distribution depends on the value of both n...

- In 2012, cost per Medicare beneficiary did what?

- 3. A. What techniques can a firm use to optimize demand deposit holdings? B. How do...

- The half-life of mercury-197 is 64.1 hours. If a patient undergoing a kidney scan is given...

- Double bonds react with Br2 to form a dibromide. Isobutylene undergoes cationic polymerization under conditions where...

- 1. Which sex chromosomes are limited to only one sex? A. X and Z B. X...