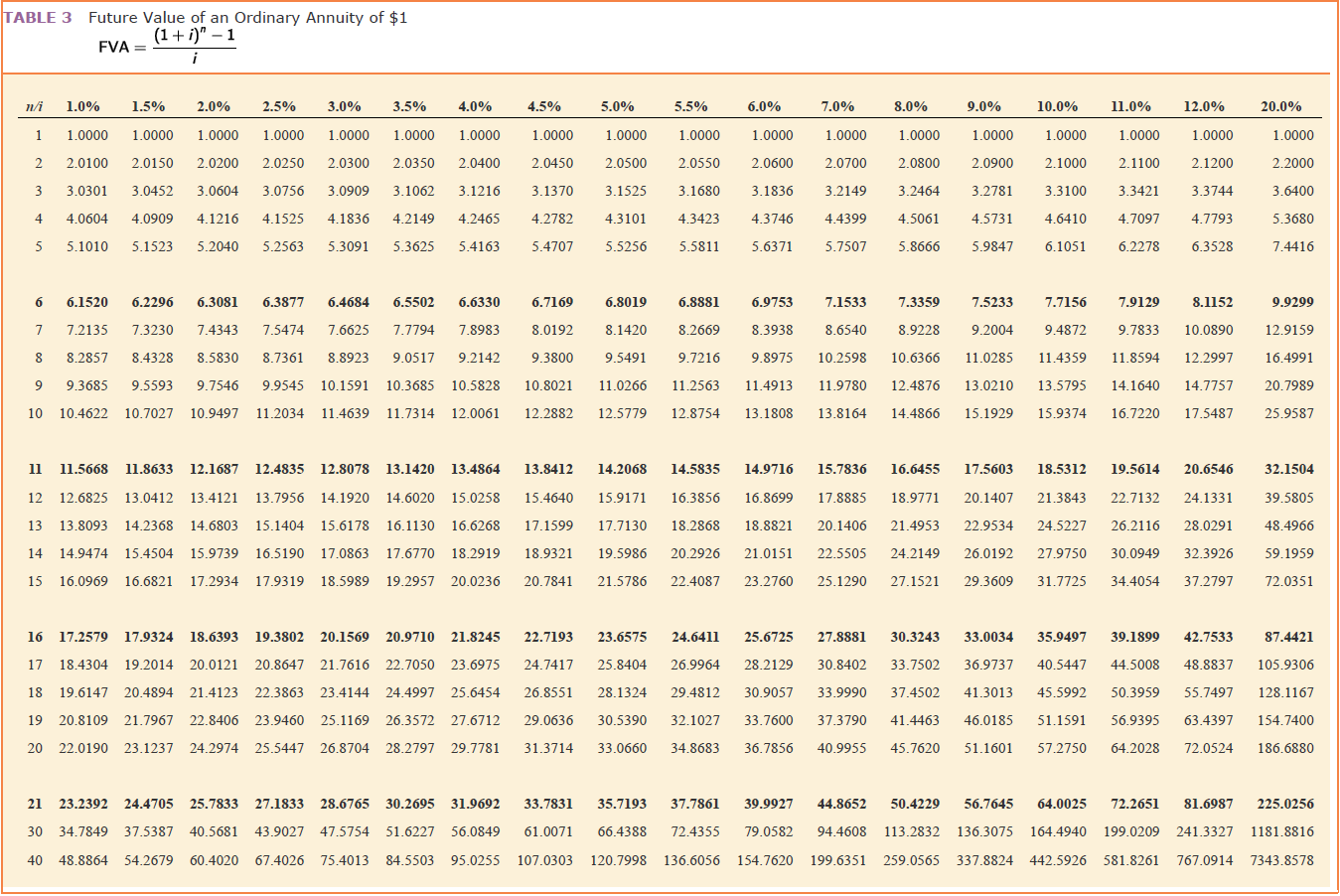

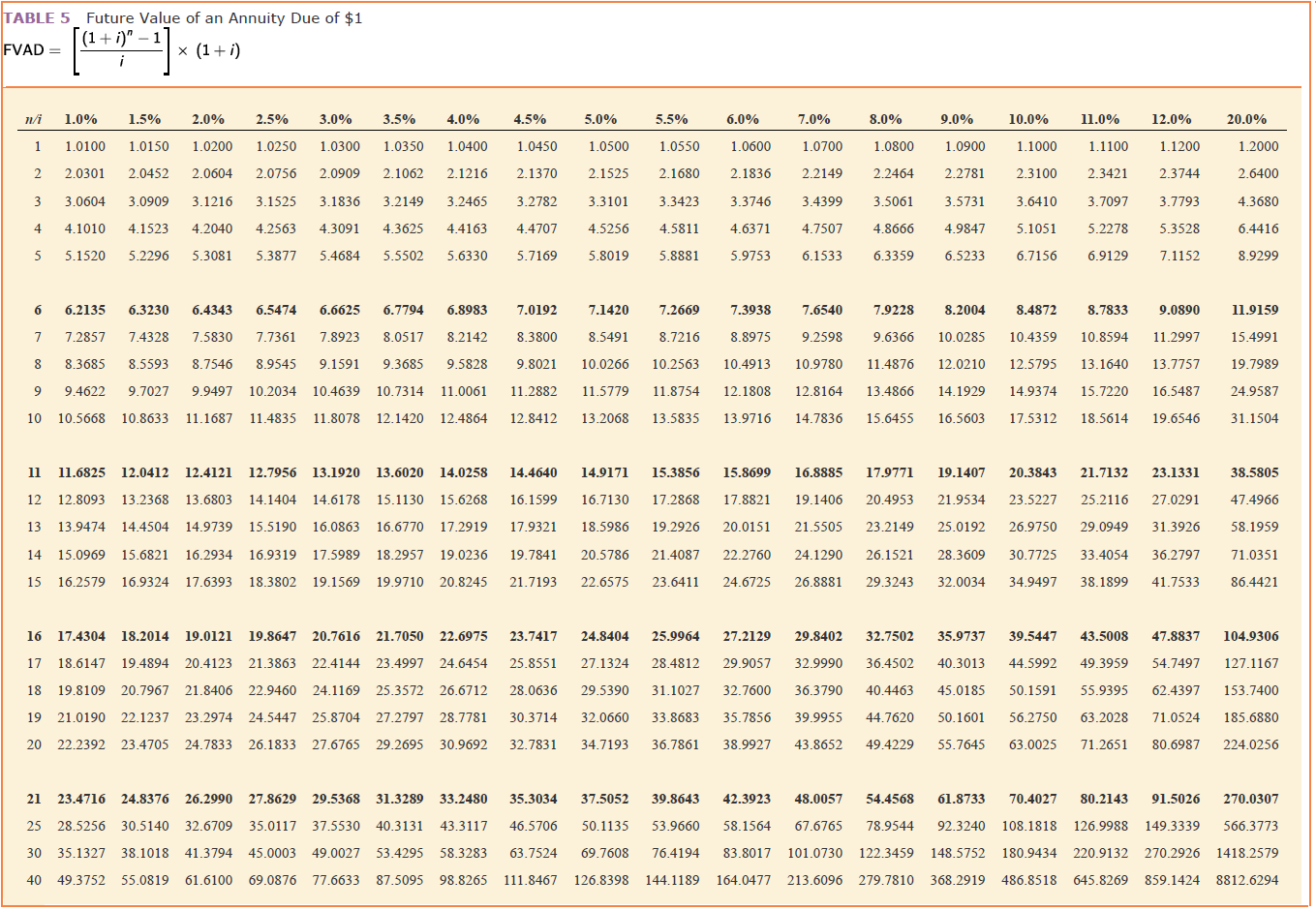

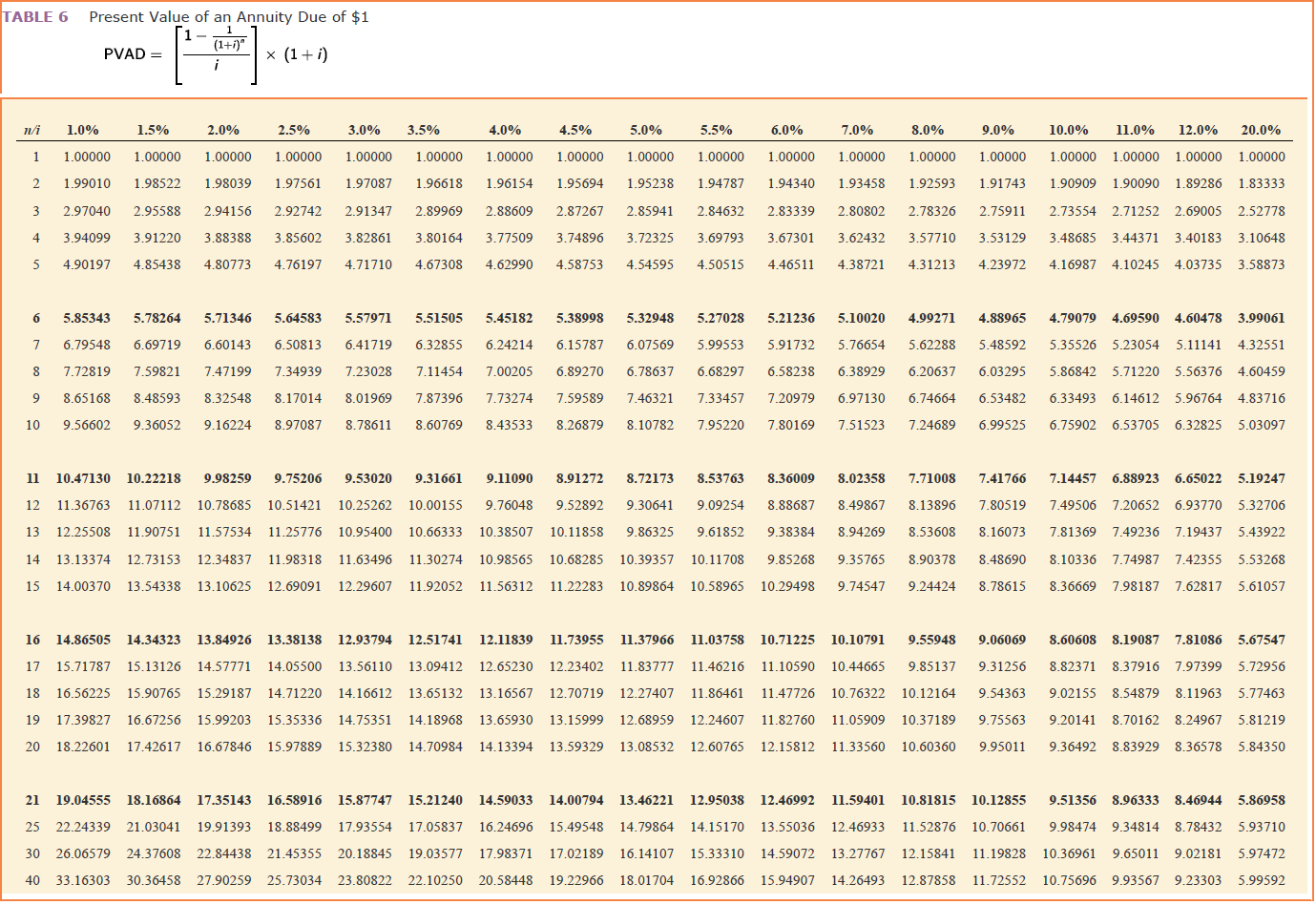

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

Required:

Supply the correct amount for each answer box on the schedule.

(Round your intermediate calculations and final answers to

the nearest whole dollar.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

Required:

Supply the correct amount for each answer box on the schedule.

(Round your intermediate calculations and final answers to

the nearest whole dollar.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

|

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2014. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.): |

| a. | Depreciation is computed from the first of the month of acquisition to the first of the month of disposition. |

| b. |

Land A and Building A were acquired from a predecessor corporation. Thompson paid $762,500 for the land and building together. At the time of acquisition, the land had a fair value of $68,000 and the building had a fair value of $782,000. |

| c. |

Land B was acquired on October 2, 2014, in exchange for 2,500 newly issued shares of Thompson’s common stock. At the date of acquisition, the stock had a par value of $5 per share and a fair value of $20 per share. During October 2014, Thompson paid $9,900 to demolish an existing building on this land so it could construct a new building. |

| d. |

Construction of Building B on the newly acquired land began on October 1, 2015. By September 30, 2016, Thompson had paid $160,000 of the estimated total construction costs of $250,000. Estimated completion and occupancy are July 2017. |

| e. |

Certain equipment was donated to the corporation by the city. An independent appraisal of the equipment when donated placed the fair value at $14,000 and the residual value at $1,500. |

| f. |

Machine A’s total cost of $110,000 includes installation charges of $500 and normal repairs and maintenance of $10,500. Residual value is estimated at $4,900. Machine A was sold on February 1, 2016. |

| g. |

On October 1, 2015, Machine B was acquired with a down payment of $3,500 and the remaining payments to be made in 10 annual installments of $3,500 each beginning October 1, 2016. The prevailing interest rate was 8%. |

| Required: |

|

Supply the correct amount for each answer box on the schedule. |

| THOMPSON CORPORATION | |||||||

| Fixed Asset and Depreciation Schedule | |||||||

| For Fiscal Years Ended September 30, 2015, and September 30, 2016 | |||||||

| Assets |

Acquisition Date |

Cost | Residual |

Depreciation Method |

Estimated Life in Years |

Depreciation

for Year Ended 9/30 |

|

| 2015 | 2016 | ||||||

| Land A | 10/1/14 | $762,500 | N/A | N/A | N/A | N/A | N/A |

| Building A | 10/1/14 | 782,000 | $53,500 | SL | $13,500 | ||

| Land B | 10/2/14 | 850,000 | N/A | N/A | N/A | N/A | N/A |

| Building B | Under construction | 160000 to date | — | SL | 30 | — | |

| Donated Equipment | 10/2/14 | 14,000 | 1,500 | 150% Declining balance | 10 | ||

| Machine A | 10/2/14 | 4,900 | Sum-of-the years’-digits | 10 | |||

| Machine B | 10/1/15 | — | SL | 15 | — | ||

In: Accounting

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

Required:

Supply the correct amount for each answer box on the

schedule. (Round your intermediate

calculations and final answers to the nearest whole

dollar.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

Cash Budget

The controller of Bridgeport Housewares Inc. instructs you to prepare a monthly cash budget for the next three months. You are presented with the following budget information:

| September | October | November | ||||

| Sales | $98,000 | $117,000 | $157,000 | |||

| Manufacturing costs | 41,000 | 50,000 | 57,000 | |||

| Selling and administrative expenses | 34,000 | 35,000 | 60,000 | |||

| Capital expenditures | _ | _ | 38,000 | |||

The company expects to sell about 10% of its merchandise for cash. Of sales on account, 70% are expected to be collected in the month following the sale and the remainder the following month (second month following sale). Depreciation, insurance, and property tax expense represent $6,000 of the estimated monthly manufacturing costs. The annual insurance premium is paid in January, and the annual property taxes are paid in December. Of the remainder of the manufacturing costs, 80% are expected to be paid in the month in which they are incurred and the balance in the following month.

Current assets as of September 1 include cash of $37,000, marketable securities of $53,000, and accounts receivable of $109,400 ($86,000 from July sales and $23,400 from August sales). Sales on account for July and August were $78,000 and $86,000, respectively. Current liabilities as of September 1 include $6,000 of accounts payable incurred in August for manufacturing costs. All selling and administrative expenses are paid in cash in the period they are incurred. An estimated income tax payment of $14,000 will be made in October. Bridgeport’s regular quarterly dividend of $6,000 is expected to be declared in October and paid in November. Management desires to maintain a minimum cash balance of $36,000.

Required:

1. Prepare a monthly cash budget and supporting schedules for September, October, and November. Input all amounts as positive values except overall cash decrease and deficiency which should be indicated with a minus sign. Assume 360 days per year for interest calculations.

| Bridgeport Housewares Inc. | |||

| Cash Budget | |||

| For the Three Months Ending November 30 | |||

| September | October | November | |

| Estimated cash receipts from: | |||

| Cash sales | $ | $ | $ |

| Collection of accounts receivable | |||

| Total cash receipts | $ | $ | $ |

| Less estimated cash payments for: | |||

| Manufacturing costs | $ | $ | $ |

| Selling and administrative expenses | |||

| Capital expenditures | |||

| Other purposes: | |||

| Income tax | |||

| Dividends | |||

| Total cash payments | $ | $ | $ |

| Cash increase or (decrease) | $ | $ | $ |

| Plus cash balance at beginning of month | |||

| Cash balance at end of month | $ | $ | $ |

| Less minimum cash balance | |||

| Excess or (deficiency) | $ | $ | $ |

Feedback

The primary source of estimated cash receipts is from cash sales and collections on account.

To estimate cash receipts from cash sales and collections on account, a schedule of collections from sales is prepared.

Learning Objective 5.

2. On the basis of the cash budget prepared in part (1), what recommendation should be made to the controller?

The budget indicates that the minimum cash balance be maintained in November. This situation can be corrected by and/or by the of the marketable securities, if they are held for such purposes. At the end of September and October, the cash balance will the minimum desired balance.

In: Accounting

Cash Budget

The controller of Bridgeport Housewares Inc. instructs you to prepare a monthly cash budget for the next three months. You are presented with the following budget information:

| September | October | November | ||||

| Sales | $250,000 | $300,000 | $315,000 | |||

| Manufacturing costs | 150,000 | 180,000 | 185,000 | |||

| Selling and administrative expenses | 42,000 | 48,000 | 51,000 | |||

| Capital expenditures | _ | _ | 200,000 | |||

The company expects to sell about 10% of its merchandise for cash. Of sales on account, 70% are expected to be collected in the month following the sale and the remainder the following month (second month following sale). Depreciation, insurance, and property tax expense represent $50,000 of the estimated monthly manufacturing costs. The annual insurance premium is paid in January, and the annual property taxes are paid in December. Of the remainder of the manufacturing costs, 80% are expected to be paid in the month in which they are incurred and the balance in the following month.

Current assets as of September 1 include cash of $40,000, marketable securities of $75,000, and accounts receivable of $300,000 ($60,000 from July sales and $240,000 from August sales). Sales on account for July and August were $200,000 and $240,000, respectively. Current liabilities as of September 1 include $40,000 of accounts payable incurred in August for manufacturing costs. All selling and administrative expenses are paid in cash in the period they are incurred. An estimated income tax payment of $55,000 will be made in October. Bridgeport’s regular quarterly dividend of $25,000 is expected to be declared in October and paid in November. Management desires to maintain a minimum cash balance of $50,000.

Required:

1. Prepare a monthly cash budget and supporting schedules for September, October, and November. Enter all amounts as positive values except for overall cash decrease and deficiency which should be indicated with a minus sign.

| Bridgeport Housewares Inc. | |||

| Cash Budget | |||

| For the Three Months Ending November 30 | |||

| September | October | November | |

| Estimated cash receipts from: | |||

| Cash sales | $ | $ | $ |

| Collection of accounts receivable | |||

| Total cash receipts | $ | $ | $ |

| Less estimated cash payments for: | |||

| Manufacturing costs | $ | $ | $ |

| Selling and administrative expenses | |||

| Capital expenditures | |||

| Other purposes: | |||

| Income tax | |||

| Dividends | |||

| Total cash payments | $ | $ | $ |

| Cash increase or (decrease) | $ | $ | $ |

| Plus cash balance at beginning of month | |||

| Cash balance at end of month | $ | $ | $ |

| Less minimum cash balance | |||

| Excess or (deficiency) | $ | $ | $ |

Feedback

The primary source of estimated cash receipts is from cash sales and collections on account.

To estimate cash receipts from cash sales and collections on account, a schedule of collections from sales is prepared.

Learning Objective 5.

2. On the basis of the cash budget prepared in part (1), what recommendation should be made to the controller?

The budget indicates that the minimum cash balance will not be maintained in November. This situation can be corrected by borrowing and/or by the sale of the marketable securities, if they are held for such purposes. At the end of September and October, the cash balance will exceed the minimum desire balance.

Can you break this down step by step

In: Accounting

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2016. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.):

Depreciation is computed from the first of the month of acquisition to the first of the month of disposition.

Land A and Building A were acquired from a predecessor corporation. Thompson paid $872,500 for the land and building together. At the time of acquisition, the land had a fair value of $76,800 and the building had a fair value of $883,200.

Land B was acquired on October 2, 2016, in exchange for 3,600 newly issued shares of Thompson’s common stock. At the date of acquisition, the stock had a par value of $5 per share and a fair value of $31 per share. During October 2016, Thompson paid $11,000 to demolish an existing building on this land so it could construct a new building.

Construction of Building B on the newly acquired land began on October 1, 2017. By September 30, 2018, Thompson had paid $270,000 of the estimated total construction costs of $360,000. Estimated completion and occupancy are July 2019.

Certain equipment was donated to the corporation by the city. An independent appraisal of the equipment when donated placed the fair value at $18,400 and the residual value at $2,600.

Machine A’s total cost of $109,000 includes installation charges of $610 and normal repairs and maintenance of $12,500. Residual value is estimated at $5,200. Machine A was sold on February 1, 2018.

On October 1, 2017, Machine B was acquired with a down payment of $4,600 and the remaining payments to be made in 10 annual installments of $4,600 each beginning October 1, 2018. The prevailing interest rate was 8%.

Required:

Supply the correct amount for each answer box on the schedule. (Round your final answers to nearest whole dollar.)

Thompson Corporation

Fixed Asset and depreciation schedule

For fiscal year ended september 30, 2017, and september 30, 2018

|

Assets |

Acquisition date |

cost |

residual |

Depreciation method |

Estimated life in years |

Depreciation 9.30.2017 |

Depreciation 9.30.2018 |

|

Land A |

10/1/16 |

? |

N/A |

N/A |

N/A |

N/A |

N/A |

|

Building A |

10/1/16 |

? |

72,700 |

SL |

? |

14,600 |

? |

|

Land B |

10/2/16 |

? |

N/A |

N/A |

N/A |

N/A |

N/A |

|

Building B |

Under construction |

270 000 to date |

___ |

SL |

30 |

___ |

? |

|

Donated Equipment |

10/2/16 |

? |

2600 |

150% declining balance |

10 |

? |

? |

|

Machine A |

10/2/16 |

? |

1500 |

Sum of the yearsdigits |

10 |

? |

? |

|

Machine B |

10/1/17 |

? |

__ |

SL |

15 |

___ |

? |

In: Accounting

Romeo Lindo, the management accountant at Woods Household Supplies, is in the process of planning the company’s cash needs for the last quarter of 2016. Extracts from the sales and purchases budgets are as follows:

Month 2016 Cash Sales Sales On Account Purchases On Account

August $71,000 $520,000 $420,000

September $55,500 $640,000 $400,000

October $38,400 $760,000 $520,000

November $36,500 $680,000 $440,000

December $56,750 $850,000 $540,000

i) An analysis of the records shows that trade receivables (accounts receivable) are settled according to the following credit pattern, in accordance with the credit terms 4/30, n90: 50% in the month of sale 40% in the first month following the sale 10% in the second month following the sale

ii) Accounts payable are settled as follows, in accordance with the credit terms 5/30, n60: 75% in the month in which the inventory is purchased 25% in the following month

iii) In the month of November, an old motor vehicle, with net book value of $95,000, will be sold for cash to an employee at a gain of $45,000. The employee will be allowed to pay a deposit equal to 50% of the amount in November and the balance will be settled in two equal amounts in December 2016 & January 2017

instrument purchased by Woods Household Supplies with a face value of $500,000 will mature on October 20, 2016. In order to meet the financial obligations of the business, management has decided to liquidate the investment upon maturity.

On that date quarterly interest computed at a rate of 6% per annum is also expected to be collected. Discussion Question _Budgets Page 2

vi) The manager of Woods Household Supplies has negotiated with a tenant for rental of storage space to him beginning October 2016. The rental is $864,000 per annum. The first month’s rent along with one month’s safety deposit will be collected from the tenant on October 1. Thereafter, the monthly rental in expected to be received at the beginning of each month.

vii) Fixed operating expenses which accrue evenly throughout the year, are estimated to be $2,016,000 per annum, and are settled monthly. Monthly depreciation expenses of non-current assets of $56,000 are included in these costs.

viii) Other operating expenses are expected to be $168,000 per quarter and are settled monthly.

ix) Wages and salaries are expected to be $2,916,000 per annum and will be paid monthly.

x) At the recently concluded negotiations between management and the union representing the workers it was agreed that Woods Household Supplies should make retroactive payments in the amount of $1,140,000 to employees. The payment is being settled in four equal tranches. The third payment becomes due and payable in October of 2016.

xi) The cash balance on September 30, 2016 is expected to be an overdraft of $175,000. Required:

(a) Prepare a schedule of budgeted cash collections for sales on account for each of the months October to December 2016

(b) Prepare a schedule of expected cash disbursements for purchases on account for the quarter to December 31, 2016.

(c) Prepare a cash budget, with a total column, for the quarter ending December 31, 2016, showing the receipts & payments for each month.

In: Accounting

Entries into T accounts and Trial Balance

Connie Young, an architect, opened an office on October 1, 2019. During the month, she completed the following transactions connected with her professional practice:

Required:

1. Record the above transactions (in chronological order) directly in the following T accounts, without journalizing. Cash; Accounts Receivable; Supplies; Prepaid Insurance; Automobiles; Equipment; Accounts Payable; Notes Payable; Connie Young, Capital; Professional Fees; Salary Expense; Blueprint Expense; Rent Expense; Automobile Expense; Miscellaneous Expense. To the left of each amount entered in the accounts, select the appropriate letter to identify the transaction.

2. Determine account balances of the T accounts. Accounts containing a single entry only (such as Prepaid Insurance) do not need a balance.

| Cash | |||

|---|---|---|---|

| c. | c. | ||

| Bal. | |||

| Accounts Receivable | |||

|---|---|---|---|

| Supplies | |||

|---|---|---|---|

| Prepaid Insurance | |||

|---|---|---|---|

| Automobiles | |||

|---|---|---|---|

| Equipment | |||

|---|---|---|---|

| Accounts Payable | |||

|---|---|---|---|

| Bal. | |||

| Notes Payable | |||

|---|---|---|---|

| Bal. | |||

| Connie Young, Capital | |||

|---|---|---|---|

| Professional Fees | |||

|---|---|---|---|

| Bal. | |||

| Salary Expense | |||

|---|---|---|---|

| Blueprint Expense | |||

|---|---|---|---|

| Rent Expense | |||

|---|---|---|---|

| Automobile Expense | |||

|---|---|---|---|

| Miscellaneous Expense | |||

|---|---|---|---|

Feedback

1. and 2. First, identify what account is used and then what type of account is used. Every account is either an asset, liability, capital, withdrawal, revenue, or expense account. Every transaction involves at least two accounts. Then determine whether the account increases or decreases. Each increase or decrease is recorded as a debit or credit in the T-accounts, following the rules of debit and credit. Net debits against credits to determine the balance and double-check to see if it is a normal balance for that account classification.

3. Prepare an unadjusted trial balance for Connie Young, Architect, as of October 31, 2019. If an amount box does not require an entry, leave it blank.

| Connie Young, Architect | ||

| Unadjusted Trial Balance | ||

| October 31, 2019 | ||

| Debit Balances |

Credit Balances |

|

Feedback

3. The trial balance lists the ending balance of each account in a corresponding Debit or Credit column. The trial balance column totals should be equal.

4. Determine the net income or net loss for

October.

$

Feedback

4. Recall that Revenue - Expenses = Net Income (Loss).

Feedback

Incorrect

In: Accounting

{kind=link}

{kind=link}

{kind=link}

{kind=link}