Please construct a nondeterministic, deterministic, and minimum deterministic finite state machine for the following regular expressions. You have to show the construction process, not just the final result.

1) acb*a | bba*b+

2) d*adc | (a)b*bc*d

In: Computer Science

The following unadjusted trial balance is for Ace Construction Co. as of the end of its 2019 fiscal year. The June 30, 2018, credit balance of the owner’s capital account was $57,800, and the owner invested $25,000 cash in the company during the 2019 fiscal year.

| ACE CONSTRUCTION CO. Unadjusted Trial Balance June 30, 2019 |

||||||||

| No. | Account Title | Debit | Credit | |||||

| 101 | Cash | $ | 17,500 | |||||

| 126 | Supplies | 9,500 | ||||||

| 128 | Prepaid insurance | 5,500 | ||||||

| 167 | Equipment | 141,780 | ||||||

| 168 | Accumulated depreciation—Equipment | $ | 27,000 | |||||

| 201 | Accounts payable | 5,000 | ||||||

| 203 | Interest payable | 0 | ||||||

| 208 | Rent payable | 0 | ||||||

| 210 | Wages payable | 0 | ||||||

| 213 | Property taxes payable | 0 | ||||||

| 251 | Long-term notes payable | 22,000 | ||||||

| 301 | V. Ace, Capital | 82,800 | ||||||

| 302 | V. Ace, Withdrawals | 30,000 | ||||||

| 401 | Construction fees earned | 141,000 | ||||||

| 612 | Depreciation expense—Equipment | 0 | ||||||

| 623 | Wages expense | 46,000 | ||||||

| 633 | Interest expense | 2,420 | ||||||

| 637 | Insurance expense | 0 | ||||||

| 640 | Rent expense | 14,000 | ||||||

| 652 | Supplies expense | 0 | ||||||

| 683 | Property taxes expense | 4,100 | ||||||

| 684 | Repairs expense | 2,700 | ||||||

| 690 | Utilities expense | 4,300 | ||||||

| Totals | $ | 277,800 | $ | 277,800 | ||||

Adjustments:

Required:

1. Prepare a 10-column work sheet for fiscal year 2019,

starting with the unadjusted trial balance and including

adjustments based on the additional facts. The June 30, 2018,

credit balance of the owner’s capital account was $57,800, and the

owner invested $25,000 cash in the company during the 2019 fiscal

year.

2a. Prepare the adjusting entries. (all dated June

30, 2019).

2b. Prepare the closing entries. (all dated June

30, 2019):

3a. Prepare the income statement for the year

ended June 30, 2019.

3b. Prepare the statement of owner's equity for

the year ended June 30, 2019.

3c. Prepare the classified balance sheet at June

30, 2019.

In: Accounting

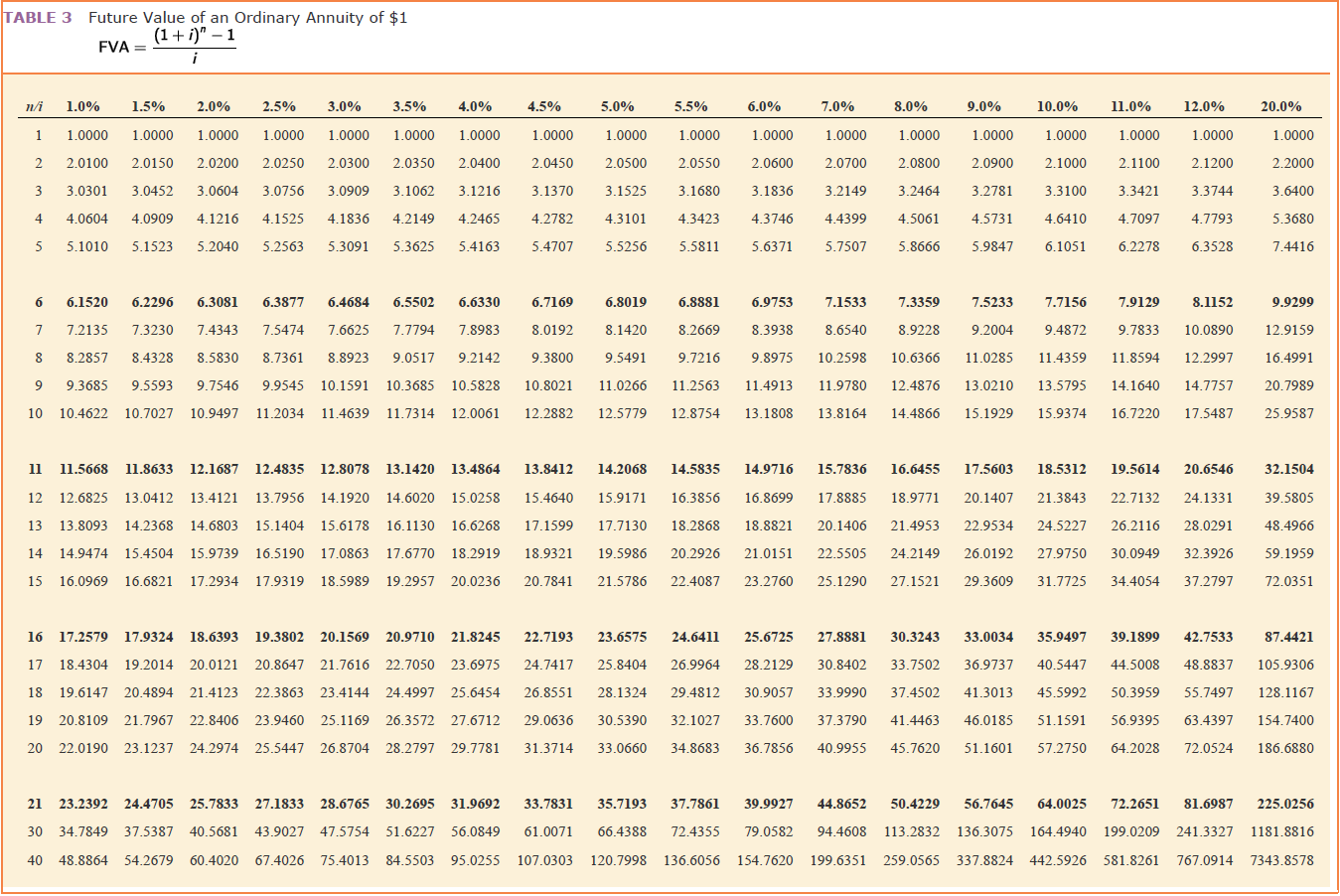

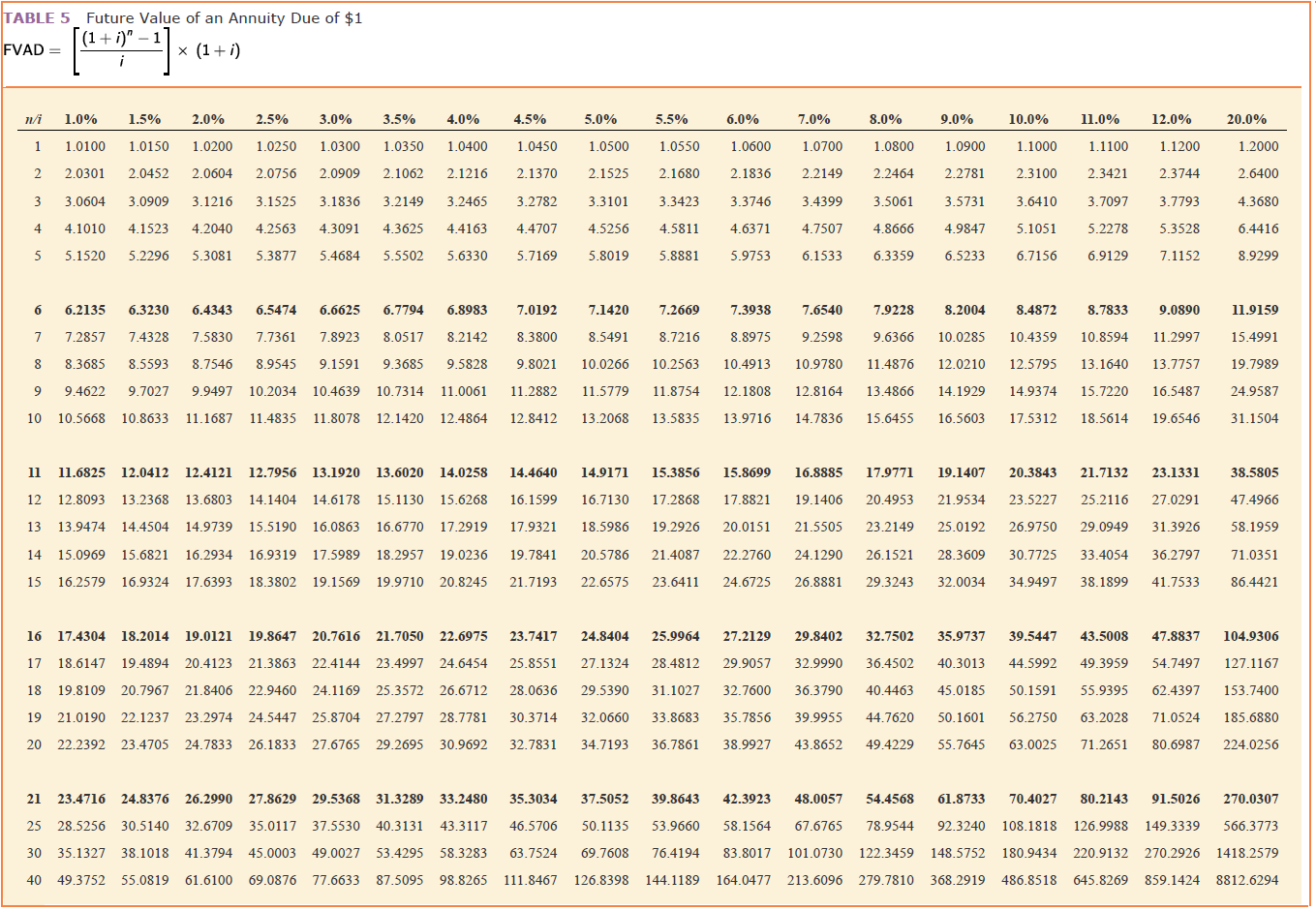

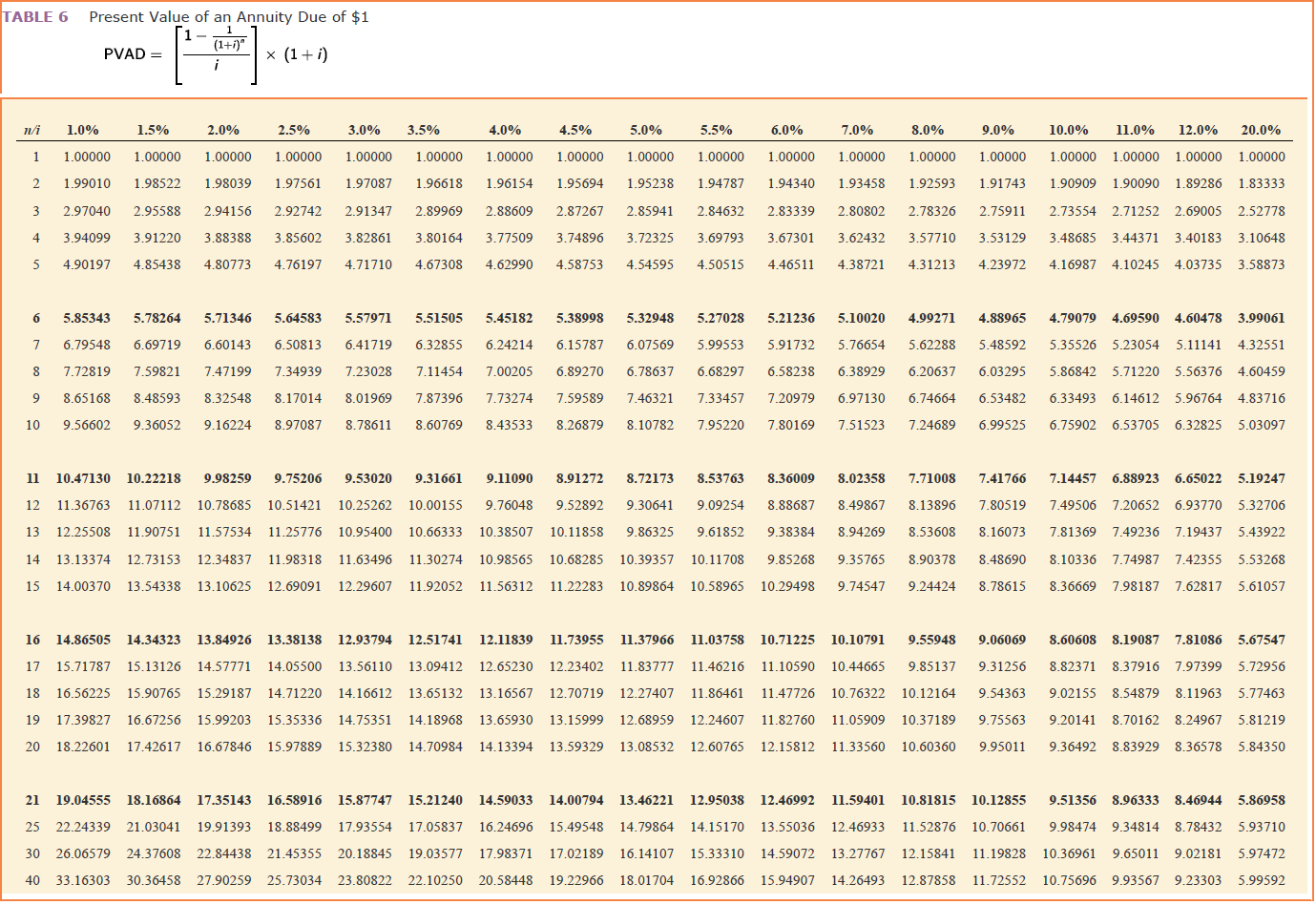

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

Required:

Supply the correct amount for each answer box on the schedule.

(Round your intermediate calculations and final answers to

the nearest whole dollar.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

Required:

Supply the correct amount for each answer box on the schedule.

(Round your intermediate calculations and final answers to

the nearest whole dollar.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

|

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2014. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.): |

| a. | Depreciation is computed from the first of the month of acquisition to the first of the month of disposition. |

| b. |

Land A and Building A were acquired from a predecessor corporation. Thompson paid $762,500 for the land and building together. At the time of acquisition, the land had a fair value of $68,000 and the building had a fair value of $782,000. |

| c. |

Land B was acquired on October 2, 2014, in exchange for 2,500 newly issued shares of Thompson’s common stock. At the date of acquisition, the stock had a par value of $5 per share and a fair value of $20 per share. During October 2014, Thompson paid $9,900 to demolish an existing building on this land so it could construct a new building. |

| d. |

Construction of Building B on the newly acquired land began on October 1, 2015. By September 30, 2016, Thompson had paid $160,000 of the estimated total construction costs of $250,000. Estimated completion and occupancy are July 2017. |

| e. |

Certain equipment was donated to the corporation by the city. An independent appraisal of the equipment when donated placed the fair value at $14,000 and the residual value at $1,500. |

| f. |

Machine A’s total cost of $110,000 includes installation charges of $500 and normal repairs and maintenance of $10,500. Residual value is estimated at $4,900. Machine A was sold on February 1, 2016. |

| g. |

On October 1, 2015, Machine B was acquired with a down payment of $3,500 and the remaining payments to be made in 10 annual installments of $3,500 each beginning October 1, 2016. The prevailing interest rate was 8%. |

| Required: |

|

Supply the correct amount for each answer box on the schedule. |

| THOMPSON CORPORATION | |||||||

| Fixed Asset and Depreciation Schedule | |||||||

| For Fiscal Years Ended September 30, 2015, and September 30, 2016 | |||||||

| Assets |

Acquisition Date |

Cost | Residual |

Depreciation Method |

Estimated Life in Years |

Depreciation

for Year Ended 9/30 |

|

| 2015 | 2016 | ||||||

| Land A | 10/1/14 | $762,500 | N/A | N/A | N/A | N/A | N/A |

| Building A | 10/1/14 | 782,000 | $53,500 | SL | $13,500 | ||

| Land B | 10/2/14 | 850,000 | N/A | N/A | N/A | N/A | N/A |

| Building B | Under construction | 160000 to date | — | SL | 30 | — | |

| Donated Equipment | 10/2/14 | 14,000 | 1,500 | 150% Declining balance | 10 | ||

| Machine A | 10/2/14 | 4,900 | Sum-of-the years’-digits | 10 | |||

| Machine B | 10/1/15 | — | SL | 15 | — | ||

In: Accounting

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

Required:

Supply the correct amount for each answer box on the

schedule. (Round your intermediate

calculations and final answers to the nearest whole

dollar.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

The following unadjusted trial balance is for Ace Construction Co. as of the end of its 2019 fiscal year. The June 30, 2018, credit balance of the owner’s capital account was $57,700, and the owner invested $26,000 cash in the company during the 2019 fiscal year.

| ACE CONSTRUCTION CO. Unadjusted Trial Balance June 30, 2019 |

||||||||

| No. | Account Title | Debit | Credit | |||||

| 101 | Cash | $ | 16,000 | |||||

| 126 | Supplies | 9,000 | ||||||

| 128 | Prepaid insurance | 7,000 | ||||||

| 167 | Equipment | 135,920 | ||||||

| 168 | Accumulated depreciation—Equipment | $ | 25,000 | |||||

| 201 | Accounts payable | 6,000 | ||||||

| 203 | Interest payable | 0 | ||||||

| 208 | Rent payable | 0 | ||||||

| 210 | Wages payable | 0 | ||||||

| 213 | Property taxes payable | 0 | ||||||

| 251 | Long-term notes payable | 28,000 | ||||||

| 301 | V. Ace, Capital | 83,700 | ||||||

| 302 | V. Ace, Withdrawals | 33,000 | ||||||

| 401 | Construction fees earned | 136,000 | ||||||

| 612 | Depreciation expense—Equipment | 0 | ||||||

| 623 | Wages expense | 50,000 | ||||||

| 633 | Interest expense | 3,080 | ||||||

| 637 | Insurance expense | 0 | ||||||

| 640 | Rent expense | 13,000 | ||||||

| 652 | Supplies expense | 0 | ||||||

| 683 | Property taxes expense | 4,100 | ||||||

| 684 | Repairs expense | 2,800 | ||||||

| 690 | Utilities expense | 4,800 | ||||||

| Totals | $ | 278,700 | $ | 278,700 | ||||

Adjustments:

Required:

1. Prepare a 10-column work sheet for fiscal year 2019,

starting with the unadjusted trial balance and including

adjustments based on the additional facts. The June 30, 2018,

credit balance of the owner’s capital account was $57,700, and the

owner invested $26,000 cash in the company during the 2019 fiscal

year.

2a. Prepare the adjusting entries. (all dated June

30, 2019).

2b. Prepare the closing entries. (all dated June

30, 2019):

3a. Prepare the income statement for the year

ended June 30, 2019.

3b. Prepare the statement of owner's equity for

the year ended June 30, 2019.

3c. Prepare the classified balance sheet at June

30, 2019.

In: Accounting

| Create Journal entries for the following: | Account Balances | |||||

| June 30, 2016 | June 30, 2017 | |||||

| Debits | ||||||

| Cash | $ 361,700 | $ 880,550 | ||||

| Accounts Receivable | 100,000 | 125,000 | ||||

| Marketable Securities (at cost) | 11,700 | 13,000 | ||||

| Allowance for Change in Value | 1,500 | 1,800 | ||||

| Construction in Process | 168,750 | 405,000 | ||||

| Prepaid Expenses | 45,000 | 10,000 | ||||

| Investments (long-term) | - | 13,500 | ||||

| Leased Equipment | - | 20,000 | ||||

| Building | 30,000 | - | ||||

| Deferred tax asset | 5,375 | 2,200 | ||||

| Land | 10,500 | 10,500 | ||||

| Discount on Bonds Payable | - | 1,305 | ||||

| Totals | 734,525 | 1,482,855 | ||||

| Credits | ||||||

| Allowance for doubtful accounts | $ 6,000 | $ 4,500 | ||||

| Accounts Payable | 87,500 | 210,000 | ||||

| Deferred tax liability | 1,000 | 3,300 | ||||

| Income Taxes Payable | 3,500 | 9,000 | ||||

| Note Payable (long-term) | 3,500 | - | ||||

| Accumulated Depreciation on Building | 2,500 | - | ||||

| Accumulated Depreciation on Leased Asset | - | 3,000 | ||||

| Lease obligation | - | 18,000 | ||||

| Interest payable on lease obligation | - | 1,800 | ||||

| Interest payable (Bonds) | - | 1,800 | ||||

| Bonds payable | - | 45,000 | ||||

| Billings on contruction in process | 150,000 | 325,000 | ||||

| Pension liability | 150,000 | 400,000 | ||||

| Convertible preferred stock, $100 par | 9,000 | - | ||||

| Common Stock, $10 par | 14,000 | 24,500 | ||||

| Additional Paid-in Capital | 8,700 | 13,700 | ||||

| Unrealized Increase in Value of Marketable Securities | 1,500 | 1,800 | ||||

| Retained Earnings | 297,325 | 421,455 | ||||

| Totals | 734,525 | 1,482,855 | ||||

| Additional information: | ||||||

| a. Dividends declared and paid totaled $650. | ||||||

| 10,500 | ||||||

| b. 300 shares of common stock (at par) were issued for cash. | 3000 | 5000 | 8000 | |||

| c. On July 1, 2016, convertible preferred stock that had originally been issued at par value were | ||||||

| converted into 500 shares of common stock. The book value method was used to account for the | ||||||

| conversion. | ||||||

| d. The long-term note payable was paid by issuing 250 shares of common stock at the beginning of the | ||||||

| fiscal year. | ||||||

| e. Short-term marketable securities were purchased at a cost of $1,300. The portfolio was increased by | ||||||

| $300 to a $14,800 fair value at year-end by adjusting the related allowance account. | ||||||

| f. During the year, a 30% interest in Ricochet Co. was purchased as an investment for $9,500. Ricochet | ||||||

| reported $20,000 in net income for the year and paid dividends of $2,000 to Smart. | ||||||

| g. $5,000 of accounts receivable were written off as uncollectible during the year. | ||||||

| h. Smart’s inventory consists of Construction-in-Process in excess of the Billings on | ||||||

| Construction-in-Process account balance. | ||||||

| i. A building was destroyed by fire during the year and insurance proceeds of $26,000 were collected. | ||||||

| j. The 12% bonds payable were issued on February 28, 2017, at 97. They mature on February 28, 2027. | ||||||

| The company uses the straight-line method to amortize bond premiums and discounts. | ||||||

| k. Smart recorded pension expense of $350,000 for the year. | ||||||

| l. A lease agreement was signed on July 1st, 2016 for the use of equipment worth $20,000. The | ||||||

| company determined that the transaction should be recorded as a capital lease. | ||||||

In: Accounting

The following unadjusted trial balance is for Ace Construction Co. as of the end of its 2019 fiscal year. The June 30, 2018, credit balance of the owner’s capital account was $51,200, and the owner invested $22,000 cash in the company during the 2019 fiscal year.

| ACE CONSTRUCTION CO. Unadjusted Trial Balance June 30, 2019 |

||||||||

| No. | Account Title | Debit | Credit | |||||

| 101 | Cash | $ | 16,500 | |||||

| 126 | Supplies | 10,000 | ||||||

| 128 | Prepaid insurance | 5,000 | ||||||

| 167 | Equipment | 146,510 | ||||||

| 168 | Accumulated depreciation—Equipment | $ | 26,500 | |||||

| 201 | Accounts payable | 5,400 | ||||||

| 203 | Interest payable | 0 | ||||||

| 208 | Rent payable | 0 | ||||||

| 210 | Wages payable | 0 | ||||||

| 213 | Property taxes payable | 0 | ||||||

| 251 | Long-term notes payable | 29,000 | ||||||

| 301 | V. Ace, Capital | 73,200 | ||||||

| 302 | V. Ace, Withdrawals | 29,000 | ||||||

| 401 | Construction fees earned | 148,000 | ||||||

| 612 | Depreciation expense—Equipment | 0 | ||||||

| 623 | Wages expense | 48,000 | ||||||

| 633 | Interest expense | 3,190 | ||||||

| 637 | Insurance expense | 0 | ||||||

| 640 | Rent expense | 14,000 | ||||||

| 652 | Supplies expense | 0 | ||||||

| 683 | Property taxes expense | 4,500 | ||||||

| 684 | Repairs expense | 2,100 | ||||||

| 690 | Utilities expense | 3,300 | ||||||

| Totals | $ | 282,100 | $ | 282,100 | ||||

Adjustments:

Required:

1. Prepare a 10-column work sheet for fiscal year 2019,

starting with the unadjusted trial balance and including

adjustments based on the additional facts. The June 30, 2018,

credit balance of the owner’s capital account was $51,200, and the

owner invested $22,000 cash in the company during the 2019 fiscal

year.

2a. Prepare the adjusting entries. (all dated June

30, 2019).

2b. Prepare the closing entries. (all dated June

30, 2019):

3a. Prepare the income statement for the year

ended June 30, 2019.

3b. Prepare the statement of owner's equity for

the year ended June 30, 2019.

3c. Prepare the classified balance sheet at June

30, 2019.

In: Accounting

{kind=link}

{kind=link}

{kind=link}

{kind=link}