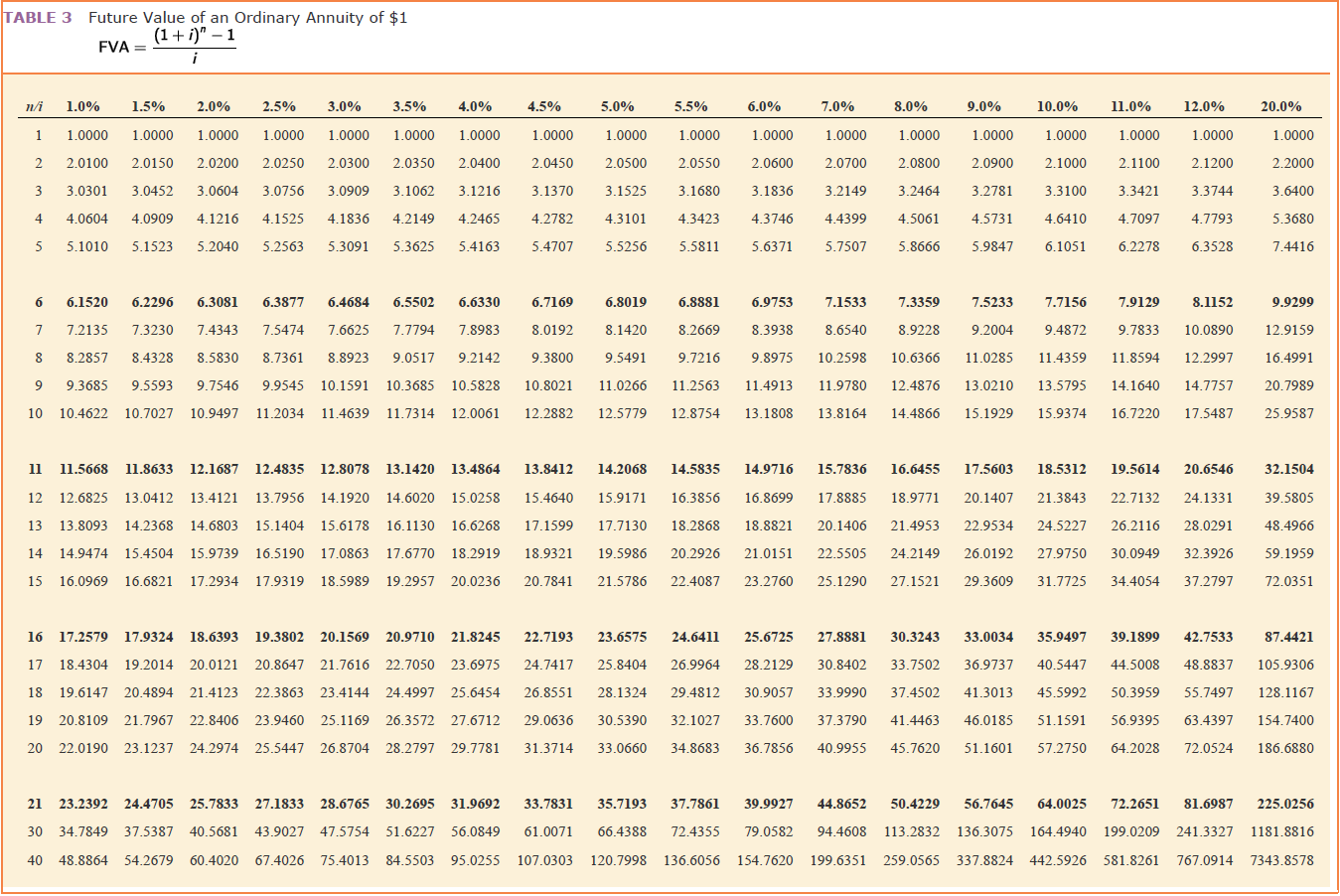

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

Required:

Supply the correct amount for each answer box on the schedule.

(Round your intermediate calculations and final answers to

the nearest whole dollar.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

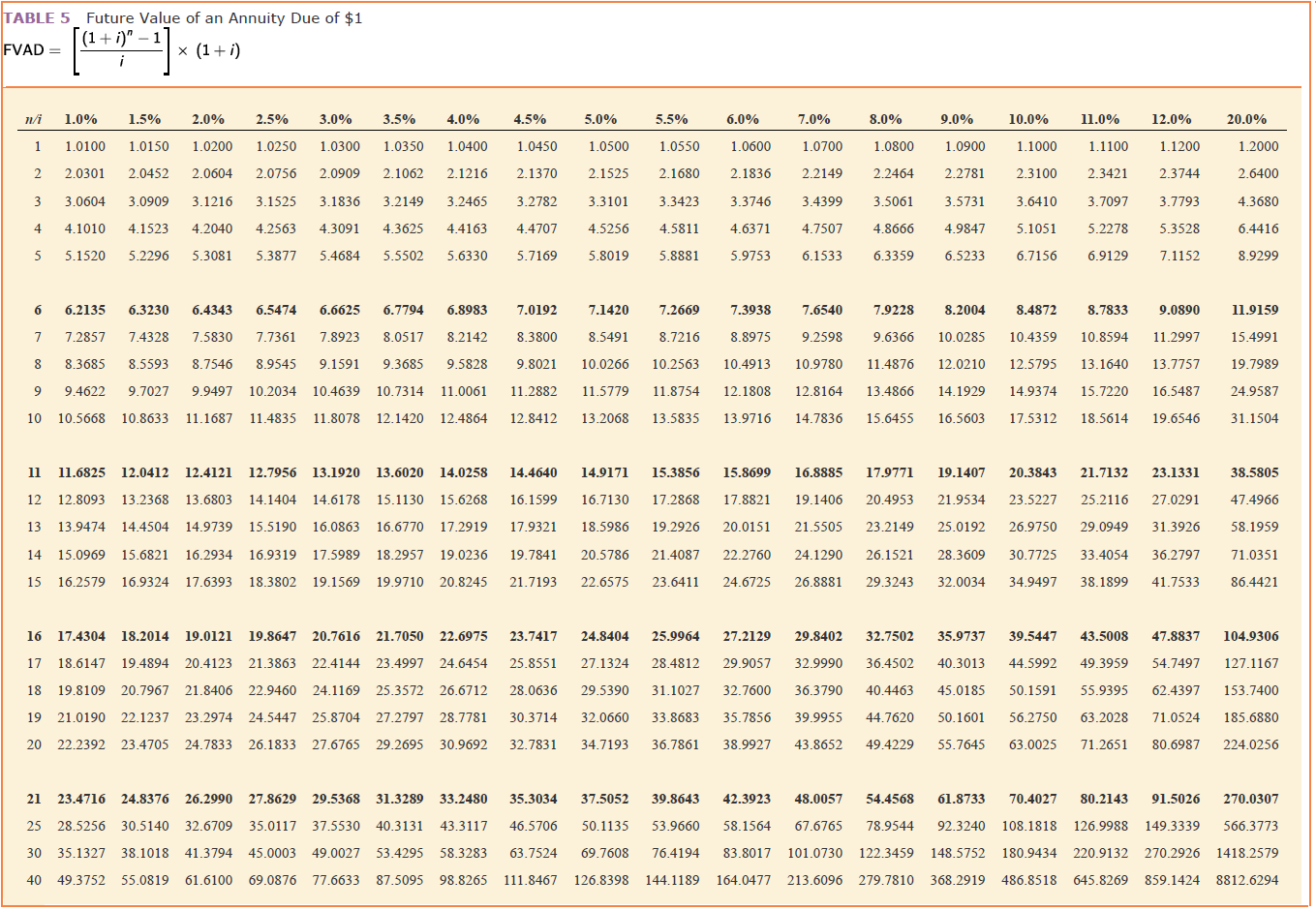

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

Required:

Supply the correct amount for each answer box on the schedule.

(Round your intermediate calculations and final answers to

the nearest whole dollar.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

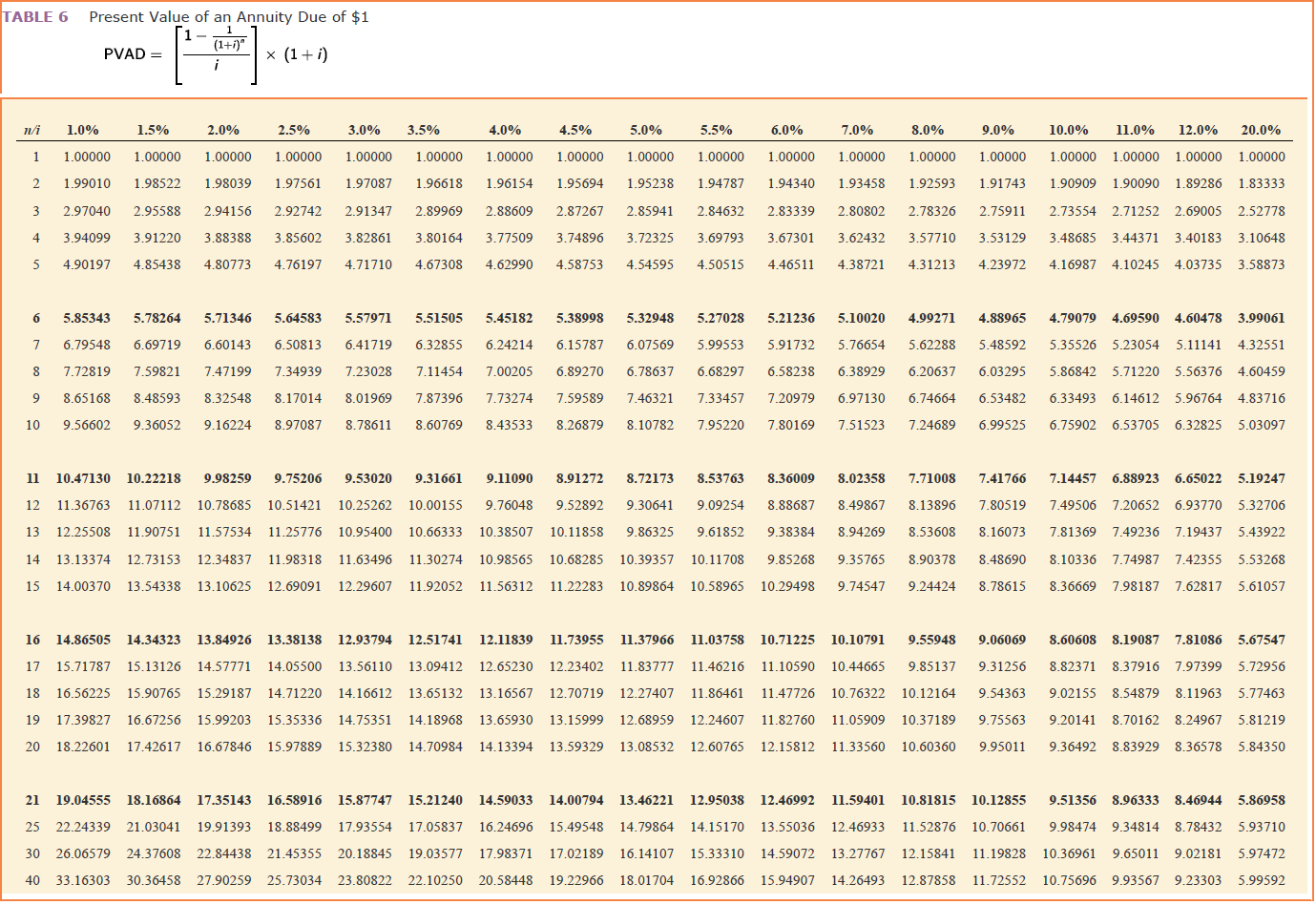

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.)

Required:

Supply the correct amount for each answer box on the

schedule. (Round your intermediate

calculations and final answers to the nearest whole

dollar.)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In: Accounting

Question text

The Chancellor of the California State University System has recently indicated that classes in the Fall of 2020 will continue to be virtual to be able to cope with the Corona Virus. Assume that all CSULB business students take a student satisfaction survey each semester. A researcher wants to compare compare two random groups of students from Fall 2019 to Fall 2020 in their satisfaction scores. The Chancellor has indicated that student satisfaction will improve with virtual classes. The groups are called FSS2019 for Student Satisfaction scores for Fall, 2020 and FSS202- for Student Satisfaction Scores for Fall, 2020. The study will calculate the difference using a confidence level of 95%. The population standard deviation is known.

The researcher wants to make sure even though they take random samples, they get a group from each of the local community colleges and plans to use Anova to analyze the data. What type of design could ensure this?

Select one:

a. Randomized Block Design

b. Completely Randomized Design

c. Matched Samples

d. Random but Related Sampling

In: Statistics and Probability

Scenario C: SonicStar Inc. requires its job applicants to take a test that measures their vocabulary and numerical skills. In addition to the written test, for specific jobs the company also requires its applicants to perform a sample of the job. Before implementing the tests, the management analyzes how well the test actually correlates and predicts job performance. When SonicStar Inc. needed to downsize, the company helped employees who were laid off to get placed in other organizations, and immediate supervisors talked to the employees about the reasons for their dismissal. When SonicStar Inc. needed to downsize, the dismissed employees' immediate supervisors discussed the need for downsizing with them. This is an example of a(n) ________.

|

situational interview |

||

|

termination interview |

||

|

behavioral description interview |

||

|

expatriation |

||

|

outplacement |

In: Other

Dealing a Rigged Game

The case study concerns Pete Miller, CEO of National Oilwell Varco (NOV) since 2001. Miller acquired over 200 companies, each with a strategic tie to the oil producing industry. The company now has a dominant share of the market for offshore drilling equipment, a segment of the industry that reported the most orders ever in 2013. NOV stands to capitalize on all segments of the future oil industry – the actual building of the drilling rigs, jack-ups, and ships that have to go offshore and do the drilling.

Management Update: In November 2013, Pete Miller announced he was stepping down as NOV’s CEO to serve as executive chairman of DistributionNOW

Case Question: Recall our definition of strategy as “a comprehensive plan for accomplishing an organization’s goals.” Explain why NOV’s approach to acquisitions qualifies as corporate-level strategy. Be specific by discussing the company’s moves, the nature and state of the industry that it’s in (drilling equipment and services), the nature and state of the industry to which it’s closely related (oil and gas drilling), and, most importantly, its goals. What are NOV’s goals?

In: Operations Management

In: Operations Management

Each change occurs during 2021 before any adjusting entries or

closing entries were prepared. Assume the tax rate for each company

is 25% in all years. Any tax effects should be adjusted through the

deferred tax liability account.

| Loss—litigation | 140,000 | |

| Liability—litigation | 140,000 | |

Late in 2021, a settlement was reached with state authorities to

pay a total of $284,000 in penalties.

Required:

For each situation:

1. Identify the type of change.

2. Prepare any journal entry necessary as a direct

result of the change, as well as any adjusting entry for 2021

related to the situation described.

In: Accounting

Chapman Company obtains 100 percent of Abernethy Company’s stock on January 1, 2020. As of that date, Abernethy has the following trial balance:

| Debit | Credit | ||||

| Accounts payable | $ | 56,700 | |||

| Accounts receivable | $ | 43,800 | |||

| Additional paid-in capital | 50,000 | ||||

| Buildings (net) (4-year remaining life) | 143,000 | ||||

| Cash and short-term investments | 80,250 | ||||

| Common stock | 250,000 | ||||

| Equipment (net) (5-year remaining life) | 295,000 | ||||

| Inventory | 110,500 | ||||

| Land | 112,000 | ||||

| Long-term liabilities (mature 12/31/23) | 171,000 | ||||

| Retained earnings, 1/1/20 | 268,750 | ||||

| Supplies | 11,900 | ||||

| Totals | $ | 796,450 | $ | 796,450 | |

During 2020, Abernethy reported net income of $122,500 while declaring and paying dividends of $15,000. During 2021, Abernethy reported net income of $159,250 while declaring and paying dividends of $49,000.

Assume that Chapman Company acquired Abernethy’s common stock for $698,050 in cash. As of January 1, 2020, Abernethy’s land had a fair value of $123,900, its buildings were valued at $219,400, and its equipment was appraised at $254,500. Chapman uses the equity method for this investment.

Prepare consolidation worksheet entries for December 31, 2020, and December 31, 2021.

In: Accounting

Chapman Company obtains 100 percent of Abernethy Company’s stock on January 1, 2020. As of that date, Abernethy has the following trial balance: Debit Credit Accounts payable $ 55,800 Accounts receivable $ 42,500 Additional paid-in capital 50,000 Buildings (net) (4-year remaining life) 209,000 Cash and short-term investments 67,250 Common stock 250,000 Equipment (net) (5-year remaining life) 357,500 Inventory 136,000 Land 114,000 Long-term liabilities (mature 12/31/23) 168,500 Retained earnings, 1/1/20 414,650 Supplies 12,700 Totals $ 938,950 $ 938,950 During 2020, Abernethy reported net income of $104,500 while declaring and paying dividends of $13,000. During 2021, Abernethy reported net income of $137,750 while declaring and paying dividends of $34,000. Assume that Chapman Company acquired Abernethy’s common stock for $849,550 in cash. As of January 1, 2020, Abernethy’s land had a fair value of $128,300, its buildings were valued at $274,600, and its equipment was appraised at $334,750. Chapman uses the equity method for this investment. Prepare consolidation worksheet entries for December 31, 2020, and December 31, 2021.

In: Accounting

{kind=link}

{kind=link}

{kind=link}

{kind=link}